Nordea betragter supply chain som den største risiko ved corona-krisen. Hvis den knækker, får det alvorlige konsekvenser. De første indikationer kommer i løbet af marts, når Vestens virksomheder vil mærke fabrikslukningerne i Kina, nemlig med containertransporterne.

Uddrag fra Nordea:

The market remains on virus-watch, though so far there is very scarce evidence that the virus outbreak is denting activity much in the developed world. However, the main effect is still ahead of us! Chinese activity dropped off a cliff in February, and this does carry a negative read-through to manufacturing activity in the months to come in the EU and US. Instead of “amazeballs”, the virus is delivering a great big bucket of bummerballs. At least for those not long US Treasuries.

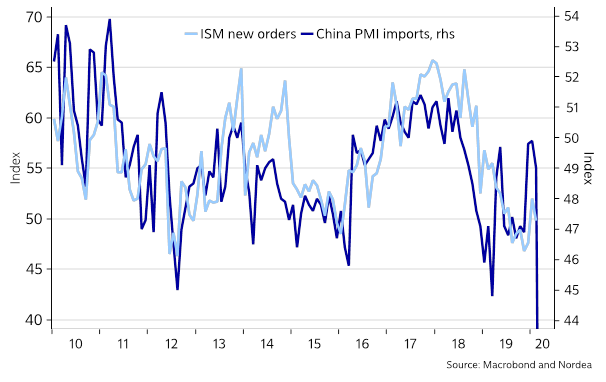

Chart 1: China-triggered shortages may show up in EU/US factory closures in March

For instance, as noted in an article in the HBR: “if Chinese plants stopped manufacturing prior to the beginning of the Chinese holiday on January 25, the last of their shipments will be arriving [in EU/US] the last week of February”. As companies “still usually carry only 15 to 30 days’ worth of inventory”, this might mean there will be a spike in “the temporary closures of assembly and manufacturing facilities in mid-March”. How many firms in EU or US are reliant on input goods from China? If they amount to 5% of value added then industrial production could be about to drop 5% between February and April(!).

One of the most important issues facing authorities currently is arguably to try to keep the credit cycle alive and kicking. Supply shortages and/or demand shortfalls must not trigger extensive defaults, as such could dent the credit cycle and perhaps prompt a truly adverse economic scenario (forget buybacks or M&A activity in this scenario…).

The current landside in oil prices, which will likely continue next week now that the Saudis have declared a full-blown price-race to the bottom, is another risk for the US credit cycle. The move by the Saudis could be interpreted as an attack on US shale producers, and we know by now that US Capex is generally positively correlated to the oil price. Credit risks are rapidly on the rise, and so is the credit cycle risks.

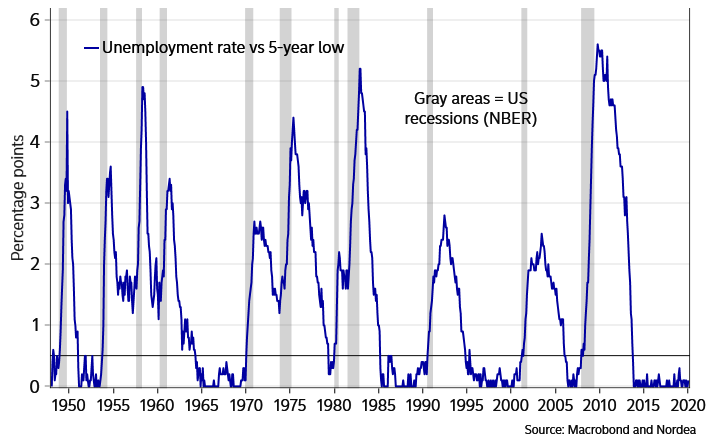

Chart 3: Demand/supply shortfalls must not boost US unemployment…

In the manufacturing sector, firms have arguably engaged in plenty of labour hoarding over the past year or so – hoping that the sector will recover robustly in 2020. Now that recovery may be postponed six-nine months, possibly causing companies to try to protect profit margins via layoffs. In the US, whenever the unemployment rate has increased by more than 0.3-0.4 percentage points, the economy has always ended up in a full-blown recession. For instance, to limit layoffs, the Swedish government is changing the rules for short-term work (in a similar way to what was done 2009-2011.)

In our main and more negative scenario, we foresee supply chain problems, quarantines (imposed or voluntary), and precautionary savings, which all weigh on both manufacturing and services sentiment in coming months.