Merrill tror, at den amerikanske bank har et pokeransigt på i denne tid. Fed vil fastholde den lave rente, men den ønsker også at få en stigende inflation. Merrill tror, at inflationen vil blive på 2 pct. i fler måneder næste år, og at den bevæger sig op over 2,5 pct.

The Fed’s Poker Face

During the post-Great Financial Crisis (GFC) expansion, Fed officials often talked

about not waiting to see the “whites of inflation’s eyes” before raising interest rates,

citing their belief that monetary policy acted with long and variable lags and seeking

to avoid runaway inflation.

This appears to have been self-defeating as inflation ran persistently below the Fed’s 2.0% target for most of the expansion, and inflation expectations trended lower in acknowledgement of the forward-looking hawkish tilt.

The new Averaging Inflation Targeting (AIT) framework’s goal is to correct this mistake by acknowledging the important role inflation expectations play, whereby it “seeks to achieve inflation that averages 2% over time”.

For investors, this means that the Fed will now not only wait to see the “whites of inflation’s eyes,” it will likely put on its best poker face and stay the course, keeping policy rates pinned near zero.

This is a positive backdrop for equity investors, as higher inflation will boost nominal gross domestic product (GDP) growth with flowthrough to corporate revenues and profits.

Investors should maintain a tactical reflationary bias as well, in our view, in anticipation of the Fed letting inflation run hot.

Below we provide some commentary around the outlook for inflation in 2021 and the potential for the Fed to hit its target.

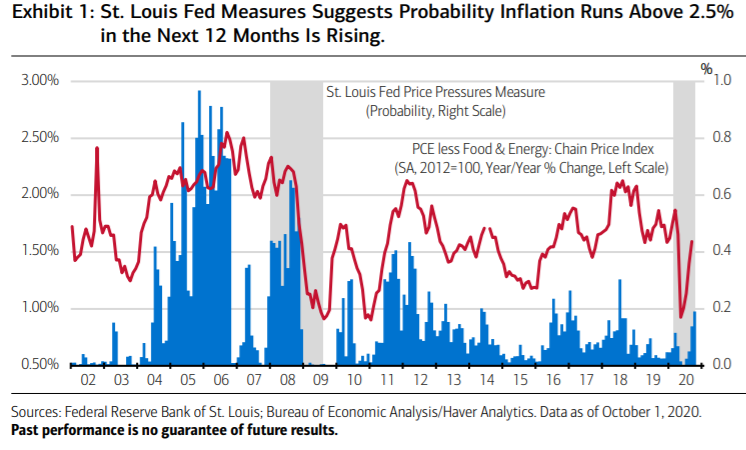

Considering the low base effects from the two-month recession earlier this year, inflation should run above 2.0% for at least a few months in the first half of next year, and the probability of inflation running above 2.5% has risen from near zero to 19%, according to the St. Louis Fed’s Inflation Pressure gauge (Exhibit

1).

There is cyclical upside in a number of the more volatile components of inflation like

hotel rates if the pandemic allows for it. The effect of the housing boom on inflation will be difficult to gauge as home prices are going up and the owners’ equivalent rent in PCE should also rise, but actual tenant-occupied rents are falling in some major cities and will act as a drag.

Beyond the cyclical pickup in inflation, the medium-term path will be determined by expectations, and the Fed’s actions will prove most important.