Saxo Bank har den store kanon fremme i en analyse af økonomiens og markedets udvikling og kommer med vurderinger, der går imod den generelle opfattelse. På markederne er der en betydelig optimisme med lutter fremgang, men Saxo Bank skyder optimismen i sænk. Januar er aldrig en god måned for at måle en trend, og valget af Joe Biden giver ikke nødvendigvis en visionær økonomisk fremgang. En række indikatorer viser faresignaler, og markedet er for præget af spekulationer i f.eks. Bitcoin og Tesla. Inflationen er på vej opad, ikke mindst på grund af store prisstigninger i f.eks. transportsektoren. Saxo Bank venter en inflation på 3,25 pct. i juli, og det vil trække renten med op. Markedet begynder at vise træthed. Det er på tide, at nogle investorer overver at tage gevinsten hjem nu.

Once is chance, twice is coincidence, three is a pattern

Summary: We are always taking a risk when we send out a cautionary note at a time when things have rarely been better, at least for the broader equity indices. But recent volatility events in some of the most speculative assets and technical developments across a number of assets, as well as our concern that inflationary risks are underappreciated has us urging a reigning in of risk exposure here.

It’s always a huge risk to warn clients that it is time to take some risk exposure off the table when things are going as well as they have for months on end, but that’s exactly what I am set to do here.

Why now?

- Technical – Our leading risk on indicators: TSLA, Bitcoin, AUDJPY and Agriculture have all lost momentum

- The Welcome Party for President Biden is over, now reality sets in

- Rates starting to bite. We remain inflation hawks and expect US CPI to rise to 3.25% by July

- History. January is very often misleading in establishing the trend for the year

Technical

The TSLA chart is ugly from a momentum perspective, i.e., the velocity of the rally move is collapsing. The daily MACD indicator is crossing lower.

Source: Saxo Group

Source: Saxo Group

Bitcoin – We believe TSLA and Bitcoin traders are often the same group of people and as such they reinforce each other. This is where the speculative gains have been greatest since the pandemic low in Q2-2020.

AUDJPY has been my go-to risk proxy in FX for over 30 years! Why? Australia is a small open economy, has a massive exposure to Asia and commodities and JPY is a current account surplus nation that recycles its savings abroad. Note that the MACD already crossed lower some days ago, and the daily trading range (ATR) suggests complacency, given the chart hasn’t participated in the up-leg in many other risk assets recently.

We at SaxoStrats are commodity bulls but over last few sessions, agriculture and especially grains, the early leaders in this space, have collapsed.

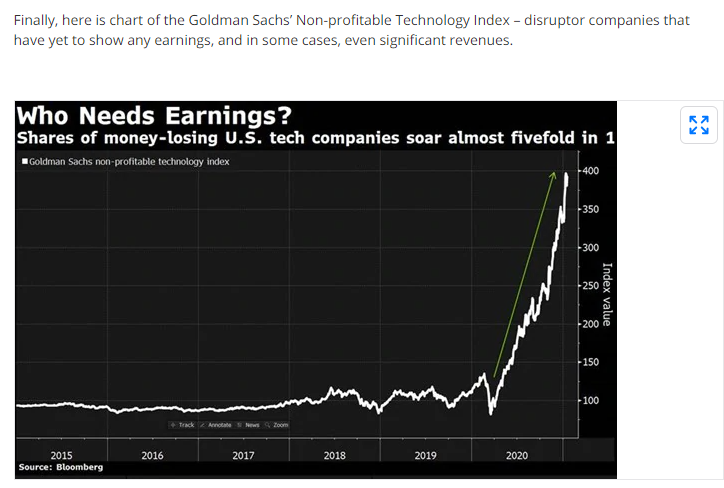

Finally, here is chart of the Goldman Sachs’ Non-profitable Technology Index – disruptor companies that have yet to show any earnings, and in some cases, even significant revenues.

The Welcome Party for President Biden

The market has celebrated the changing of guard at the White House as it expects nearly $1.9 trillion worth of new stimulus, although most likely the final amount will come in south of $1 trillion. What the market tends to forget is that in US politics talk is cheap, action extremely difficult – especially with the slimmest of majorities in Congress for the Democrats.

Unlike most commentators, I don’t believe President Biden offers a robust vision for dealing with the critical issues at hand in the US, from inequality to its structural deficits. His back-to-normal agenda is both flawed and entirely lacks vision. Sure he is nice and talks a good game on the need for national unity, but the US doesn’t need a nice President, it needs a visionary President and the oldest President ever conditioned by a lifetime of his past five decade in politics, is not likely to be that person.

Interest rates matter

All of the markets today are counting on one thing and one thing only: low interest rates. But we firmly believe rates at the longer end of the yield curve will rise, even as central banks keep short rates pegged near or below zero. The US 10-year treasury benchmark could easily rise above 150 bps. Why?

The equity market is one large bond with a huge duration of 20! – For those unfamiliar with the implications of duration, this means that a 100 basis point, or 1% move in the yield will cost at least 20 points (percent). That is a yield-sensitive market and the US 10-year benchmark already has risen from lows last August near 50 bps by 60 bps to the current level of 1.10%

The need for social stability has replaced the need for financial stability as the key macro policy response. This means that from here, stimulus will be aimed at the pockets of consumers and small businesses rather than large corporations. It means massive spending increases for the common good in terms of welfare, education and health, but also for infrastructure and the Green Transformation.

This then translates into Supply Side Bottlenecks where the physical world is too small for the digital economy and online economy to continue to scale at the same pace as previously.

You can have the best online platform in the world, but you still need to: produce your goods (China), where factories now wants an additional 15-25% to deliver the order you put in 2020. Then when you get the goods you need to ship them from a Chinese port. Good luck.

Container rates are up 400% to 600% depending on port of delivery, and when you then finally get the goods delivered in your distribution center, the cost for the final mile of delivery has risen by some 50% in places on capacity constraints!

In other words, business-to-business inflation is rampant. Consumer demand will continue as stimulus will be aimed at driving that demand. Inflation is here.

The chart below suggests the market is increasingly concerned about the arrival of higher inflation, as the Breakeven Rate – the difference between the yield on a basic 10-year US Treasury versus the yield on an inflation-linked treasury – is well over 2%.

Finally, it is sad to admit that I have more than 30 years on my back of watching and trading the financial markets. My old mentor in trading used to force me to go on leave for January as he believed that the first move with “fresh money put to work” tends to be wrong.

And that may be never more so than this ýear, as the market tries to price in a post-pandemic boom with no downside risks. But boom or no, there is only one focus this year: inflation and how long yields react. A glacier like move up in rates on rising inflation will be welcomed by market, but a discontinuous jump in both will not.

The inflation in the US began in the late 1960’s on Vietnam War spending and the decline of the credibility of the US dollar’s gold backing, and actually eased slight after Nixon de-pegged the USD from gold in 1971 (averaging well above 3%) before then rising sharply and then exploding on the Arab oil embargo in late 1973 and exploding again in the late 70’s, much of rise happening even before the Iranian oil workers’ strike and Iranian Revolution exploded the price of oil once again. Inflation simply cannot be called in advance.

I am feeling so much deja vue from my childhood in the 1970s: big government, big deficits, gold standard abandoned, opening up of China (versus current attempt at closing), youth revolution, and not least bad fashion, hairstyles and colors. All of which I see repeated.

SaxoStrats and I have no reason to think we can time anything or predict the future, but we want to encourage especially long-only investors and those most steeped in the momentum trades of the last 9-10 months to consider taking some profit here on signs that market fatigue is starting to show: once is chance, twice is coincidence, three is a pattern.