Pengeforsyningen i USA er steget lige så voldsomt som under Den anden Verdenskrig, skriver Merrill i en analyse, og det vækker bekymring om de langsigtede konsekvenser, især for inflationen. De voldsomme stimuli og centralbankens massive opkøb af statsobligationer har været nødvendige, men det har også skabt en enorm opsparing, som kan føre til et voldsomt forbrug med efterfølgende inflation som efter krigen. Det kan ifølge Merrill tvinge centralbanken til at træde tilbage fra den aktive pengepolitik og politisk-økonomisk støtte og kræve uafhængighed over for finanspolitikken, som det skete med en aftale i 1951. Det tog flere år at bekæmpe inflationen efter krigen, og det kan blive vilkårene i de kommende år, vurderer Merrill. Det kan blive nødvendigt for centralbanken, Fed, at synliggøre sin uafhængighed med en ny aftale.

Deficits, the Money Supply and Inflation

The ongoing creation of money and fiscal deficits to cushion the U.S. economy from the

effect of shutdowns and other pandemic effects are an order of magnitude greater than

any policy response since World War II (WWII). While helpful for the time being, the current

surge in government debt and money printing has raised concerns about the longer-term

consequences of this massive government spending binge.

During WWII, deficits of roughly 25% of gross domestic product (GDP) were necessary to

transform a peacetime economy into a war production machine that eventually prevailed.

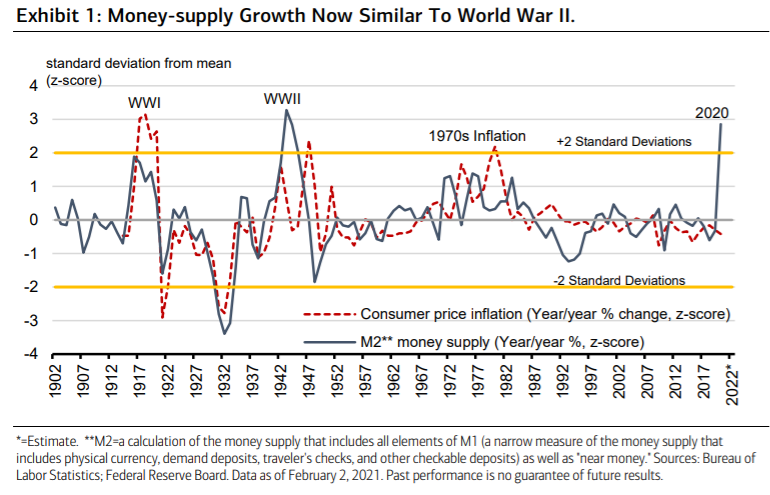

Prior to 2020, the episodes of the most extreme money growth in the 20th century were

during WWI, WWII and the great inflation of the 1970s. During the period of massive

deficits and money creation in WWII, money-supply growth (blue line) exceeded three

standard deviations above its 120-year average, as shown in Exhibit 1. The other two

highly inflationary episodes, WWI and the 1970s, saw money growth between one and two

standard deviations above normal. The WWII spike in money-supply growth has been

almost matched over the past year when money growth was just shy of three standard

deviations above its average of the past 120 years.

Thus, the faster, bigger response of inflation to the surge in money-supply growth during

WWI compared to the lagged, more proportionate response in WWII (Exhibit 1), probably

owes something to the much lower velocity of money in the 1940s, when lingering caution

from the Depression and massive saving during the war slowed the circulation of money.

Still, it’s hard to escape the conclusion that inflation is going to rise above trend over the

next few years, in our view. In addition to the massive money-supply growth, the forced

saving during the pandemic is likely to be unleashed, speeding up the velocity of money

just as the forced saving during WWII spurred the consumption boom that fueled the U.S.

economy in the 1950s. It took a few years for the high inflation of the late 1940s and

early 1950s to subside after the war.

As shown in Exhibit 1, the Fed had to rein in the money supply after the war before

inflation returned to trend. To do that, the Fed had to assert its independence from the

Treasury and fiscal deficits by reaching the Treasury-Federal Reserve Accord in March

1951. Currently, the Fed is bound to monetize government debt as in the 1942–1951

period. A key to avoiding inflationary instability in the future will likely be a similar

agreement to that in 1951, separating monetary and fiscal policy by restoring the Fed’s

independence.