Vi er ikke langt fra det pengeløse samfund, skriver Nordea i en analyse af de digitale valutaer, som centralbankerne eksperimenterer med. De gammeldags pengetransaktioner er faldet til 20 pct. af alle pengetransaktioner. Kina er foran med en digital yuan, men også ECB og den svenske Riksbank arbejder med konkrete planer. Nordea venter, at den nye kinesiske valuta vil blive lanceret i forbindelse med vinter-OL næste år, og flere andre centralbanker kommer derefter med deres, i første række den svenske centralbank. Det kan i første omgang føre til højere renter, men på sigt giver det centralbankerne nye muligheder i pengepolitikken, også med negative renter. En af de vigtigste konsekvenser er, at digitale valutaer vil udhule dollarens internationale rolle. Det vil i første omgang ske ved, at mange fjernøstlige lande vil bruge den digitale yuan i samhandelen med Kina.

Central bank digital currencies: China is (almost) the first mover – buy CNY?

The PBoC, the ECB, the Riksbank and the Fed are all looking into digital currencies. We look at the status and the potential repercussions. Could we enter a period of speculation in the CNY ahead of the launch of the digital renminbi?

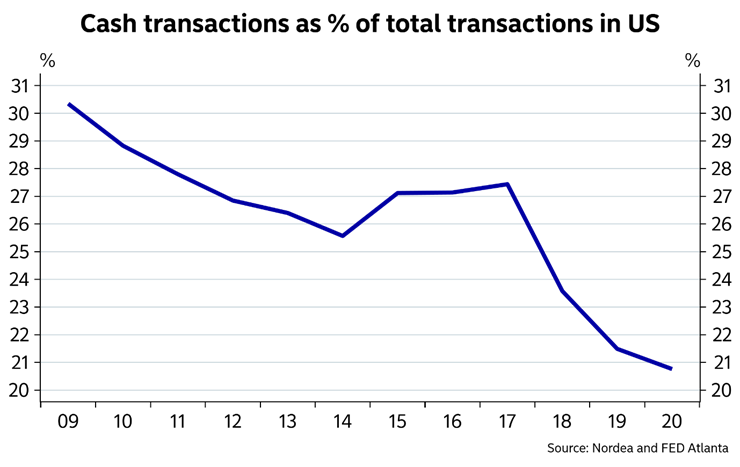

CBDC (central bank digital currencies) is one of the most exciting and important topics at the moment. Through the last decade the transition from physical fiat money to digital payments has formed our society more than ever. With the evolution (or even revolution) in digital payments services, a possible cashless society doesn’t seem that far away in several countries.

New services as MobilePay in Denmark, Swish in Sweden, Venmo in the US etc. have given the end-users a new and more flexible solution when transferring money privately. Furthermore, increasing focus on money laundering, terror financing and KYC combined with the before-mentioned flexibility has lowered the cash share as a payment instrument.

These are obvious reasons for a central bank to investigate a digital currency setup, but likely not the only drivers. Could it be that a digital currency allows for a more direct type of QE as a policy instrument?

Chart 1. Cash is playing a less and less important role in society

Our main takeaways

We expect China to launch the digital renminbi at the Winter Olympics in 2022 and wouldn’t rule out that markets speculate in a positive repricing of the renminbi ahead of the launch.

We expect all major central banks to launch digital currencies over time, which opens the door for actual “people’s QE” compared to the current “asset QE”.

We wouldn’t rule out that a launch of a digital currency would make it easier for central banks to go even deeper into negative territory on the policy rate, but this is clearly not a story for the next few years. We ultimately rather expect digital currencies to lead to higher interest rates.

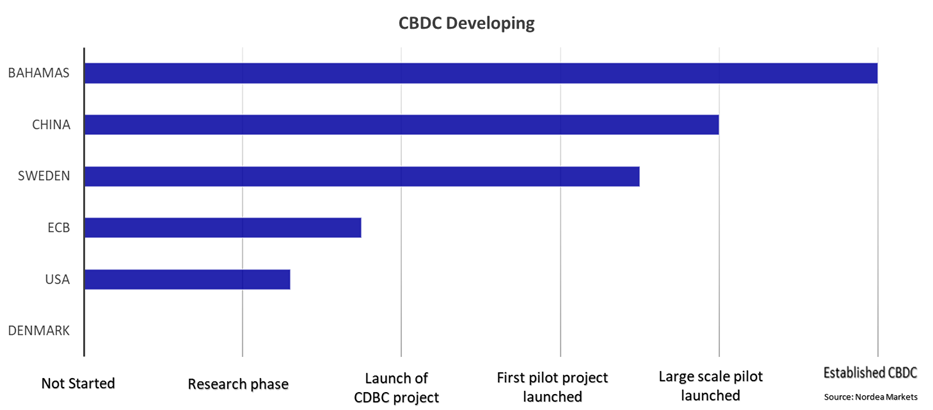

China is leading the race, but Sweden is the forerunner of Western economies in the CBDC development

A CBDC is a currency issued by the central bank as a digital version of their physical currency. This currency will be placed in a digital wallet either on a phone or in a “node”. Each and every person (and potentially company) is likely to get such a digital wallet directly in the central bank over time.

The difference between a CBDC and the money placed in your bank account today is that in the case your bank goes into bankruptcy, your money (minus an insured sum) will be lost. A CBDC on the other hand is secured by the central bank, meaning it cannot be lost but only lose value due to inflation; 1 digital dollar will always be equal to 1 dollar.

The big question is whether these wallets will carry interest rates or not. In principle the wallet should carry an interest rate alongside the deposit rate of the central bank, which in the case of the ECB, the Riksbank and the Danish central bank would be a negative carry.

Will central bankers opt to free digital wallets from a negative interest rate? In such case they would clearly need to limit the size of the wallets. Fabio Penetta from the ECB has already multiple times mentioned a potential limit at EUR 3.000 for the Euro wallet to prevent this potential problem.

Chart 2. A development time-line of DBDCs from various central banks

The current first mover in the CDBC developing process is the Peoples Bank of China (PBOC) with their Digital Currency Electronic Payment (DCEP). They are currently testing their CBDC in a large-scale pilot project and hope for a full implementation by the Winter Olympics 2022.

Most countries are not near as far in the development of digital currencies, in addition multiple emerging and frontier markets don’t have the required know-how and money to develop the infrastructure even though some of these countries would be the potential biggest gainers by having a CBDC because their commercial banking infrastructure is very unstable. This leaves a decent space for a Chinese attempt to “reservenize” the Renmbinbi via opening the CNY DCEP to other countries or via selling the infrastructure to other countries.

If China gives other countries direct access to their DCEP, then the buying pressure in the DCEP would give the PBOC an incentive to issue more DCEP “nodes”. This could lead to a new dollarization or more correctly a “yuanization”, and clearly be a risk for the USD reserve status over time should the Chinese digital currency project succeed.

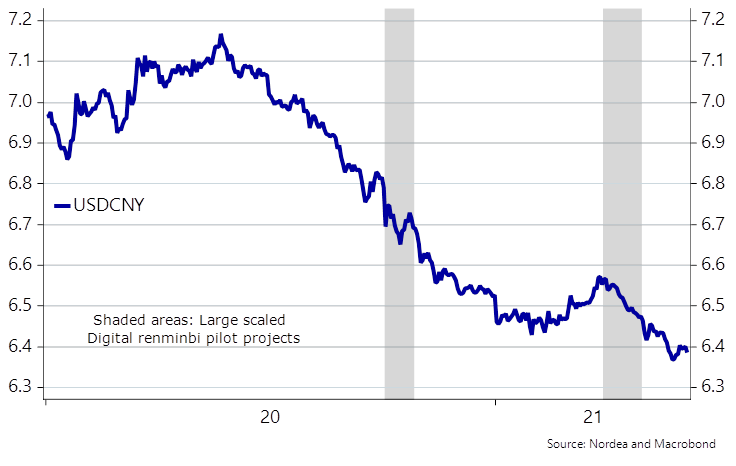

We have noted how the USD/CNY has clearly traded lower during the pilot test periods of the digital renminbi. Maybe an early signal of what to expect when we get closer to an actual launch?

The latest test ran from 10 to 23 April including 500,000 persons, which is 10 times more than the first test in October 2020. However, we are still far away from a “real” world scenario so it will perhaps be a small-scale launch by the Winter Olympics.

Chart 3. USD/CNY tends to drop when the PBoC tests the new digital renminbi. A coincidence?

Sweden is currently a clear frontrunner in the CBDC development in the Western countries. In contrast to China, they are using a blockchain-based technology as their digital krona is based on the DLT technology. It is Accenture which has been hired for the job at a contract running from 2019 until 2026, if all options for extensions are exercised.

In April this year they published the results and conclusions of the first pilot project. One of the current focus areas that needs to be tested is if the DLT technology can handle retail payments (China said it could not). Another important topic is the way that the e-krona will be stored, where they mention three different options, each with advantages and disadvantages.

The user stores a private key and CBDC locally for example on their phone, in an app or on a card:

Most cash look-a-like, if you lose your storage (eg phone), your money will be lost precisely as when you lose your cash in a wallet.

The user stores a private key locally but the CBDC is stored in the network in a “node”:

With the money stored in a node, you will not lose your money in the case of losing your key.

The user stores a private key and the CBDC in the network in a node

Nearly identical to our current bank accounts and associated payment services, only difference is that it will be a liability against the central bank instead of your commercial bank.

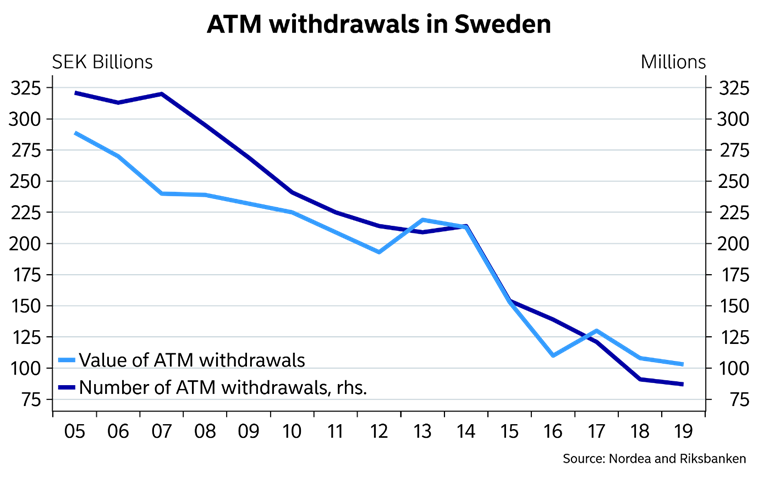

Chart 4. Sweden is also turning cashless rapidly

The ECB and the Fed are not as far as China and Sweden in their digital Euro and Dollar projects. In the same interview where the ECB’s Fabio Penetta mentioned a possible limit at EUR 3,000 of the wallet, he also mentioned 2026 as the earliest launching date.

The research about a digital dollar is run by the digital dollar project, which is a non-profit partnership between Accenture and the Digital Dollar Foundation, and a partnership between Boston Fed and MIT. These projects are supposed to run as complements and therefore both contribute with insightful research to the CBDC environment. Even though the digital dollar project is about to launch five pilot projects, the US is still far behind China and Sweden. However, after a message from Powell an escalation of the digital dollar could be on the cards.

What are the repercussions for central banks, interest rates and FX developments?

As we mentioned in the beginning, central banks are likely inclined to look into digital currencies for several reasons. First, it is easy to monitor transactions. Second, they may help protect simple savers from negative interest rates. Third, it fits hand in glove to the de-cashing trend of the most recent decades.

We also find that a digital currency may increase the size of the tool-box of the monetary policy. Currently, central banks buy assets (mostly bonds) from financial counterparts in return for fresh digital reserves (an asset swap), but these reserves are parked in the commercial banking system and hence rely on the usual transmission mechanism before reaching the real economy. If a digital currency is in place, then the central bank may just as well decide to transform the asset swap QE into a form of People’s QE.

Instead of buying 120bn worth of US Treasury bonds a month, the next step may simply be that each and every person’s digital wallet is revalued by 120bn divided by the population size every month. This would also fit hand in glove with the new woke style of many central banks.

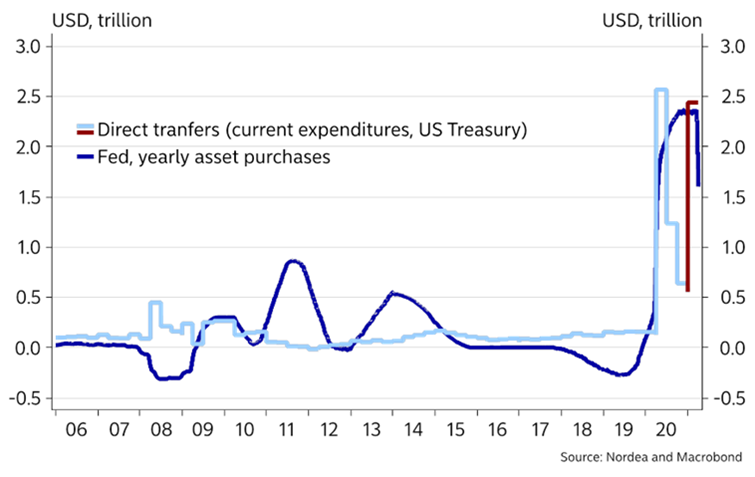

This is by the way almost what is already happening in practice, since the Fed is buying the bonds which are issued to pay each American adult 300$s via direct transfers a week currently. We wouldn’t rule out that such an infrastructure hypothetically opens the door for negative interest to an even larger extent, but a People’s QE programme would on the other hand prove much more efficient than asset QE in terms of creating inflation. We hence rather bet on higher, than lower interest rates as a result of a potential series of launches of digital central bank currencies.

Chart 5. We are already close to People’s QE in practice. A CBDC would make it even more likely

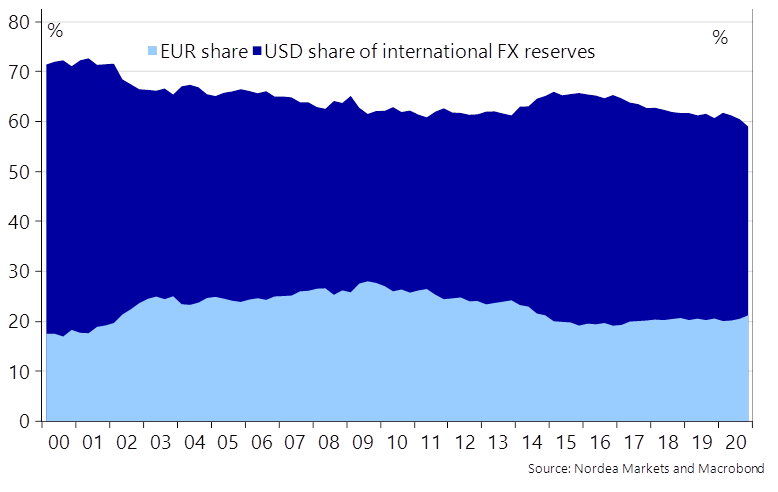

A potential early adoption of the digital renminbi by frontier and emerging markets may also open the door for a de-dollarization and a yuanization (Global: Bitcoin, the Chinese and the dollar) of the global economy.

As China’s GDP and role in world trade continue to grow, it seems natural to expect that countries, especially its neighbouring countries, will to a larger and larger extent start to use China’s currency as both invoicing and financing currency. And if demand for China’s currency increases, the appetite for dollars will decrease, which – keeping everything else equal – will lead to a continued de-dollarization in global FX reserves. A process that is currently already slowly in the making.

For all that, the dollar is likely to remain the world’s most important reserve currency for many years, perhaps even decades … But the Chinese first-mover advantage on the CBDC agenda may prove to be an important milestone for FX markets and we certainly wouldn’t rule out a continued clear strengthening of the CNY ahead of the launch of the digital renminbi in 2022.