Digitaliseringen og den unge generation vender op og ned på betalingssystemerne. En ny form for “Køb nu, betal senere” – i forkortet form BNPL – stormer frem og tager markedsandele fra creditcards og alle traditionelle betalingsformer. Udviklen går hurtigere i Europa end i USA, især i de skandinaviske lande, men også i Tyskland, der har været bundkonservativ, hvad betalinger angår. Den hurtige udvikling skyldes, at det er den unge generation, Millennials og Gen Z, der bruger de nye metoder med digitale betalinger og mobile pay. De udgør kun en lille del af samtlige betalinger, men de vokser eksplosivt, og Morgan Stanley venter, at det vil udhule bankernes indtjening fra creditcards. Det er tegn på endnu en stor disruption fra fintech-selskaberne. Det særlige ved BNPL er, at kunderne ikke betaler renter på den udskudte betaling som ved brugen af creditcards.

Buy Now, Pay Later:

Banking on Global

Financial Innovation

The new credit payment is the latest Fintech disruptor. Can established legacy banks adapt to keep up with the increased e-commerce demand and the red-hot tech services?

The latest Fintech sounds simple enough: Buy a product, take it home, set up payments after. However, the changes this innovation may bring to the financial sector are anything but. In fact, “buy now, pay later” (BNPL) platforms—adopted, so far, mainly by app-loving Millennials and Gen Z—are changing how people shop and spurring financial institutions to keep up.

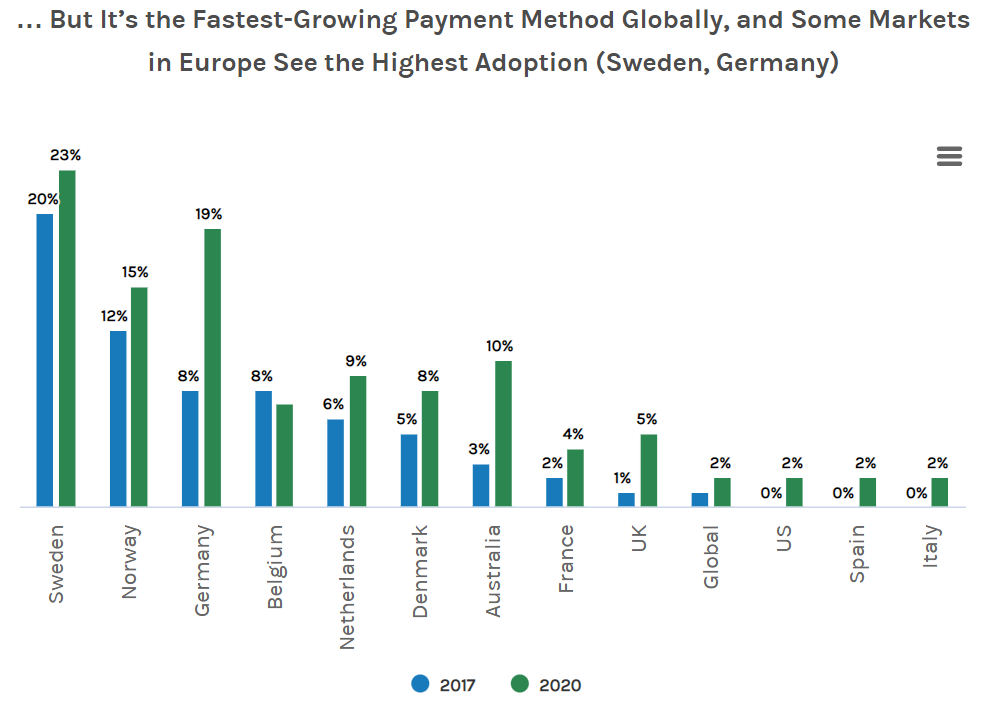

BNPL is one of the fastest-growing e-commerce segments in Europe and Australia, and it is expanding across the U.S.

“We do expect BNPL to grow faster than traditional credit cards in Europe,” says Giulia Aurora Miotto, a Morgan Stanley European Equity Analyst. “And we think this adds up to the trend of Fintechs slowly ‘skimming the cream’ off different banks’ businesses in Europe.”

That means potential disruption for legacy financial services companies, which must compete to offer similar services to existing customers, while adapting to (and adopting) this type of retail-financing Fintech to grow their customer base.

BNPL services are positioned to continue taking market share in the consumer spending space given their compelling offers for consumers. Miotto says, “Over the long term, we stress the importance for banks in Europe to potentially roll out a similar offering and develop apps that are able to engage customers.”

Not to be defeated in the tech space, some incumbents have formed notable partnerships and acquisitions with BNPL providers, while offering installment plans and other similar offerings to consumers.

Why Is ‘Buy Now, Pay Later’ Popular?

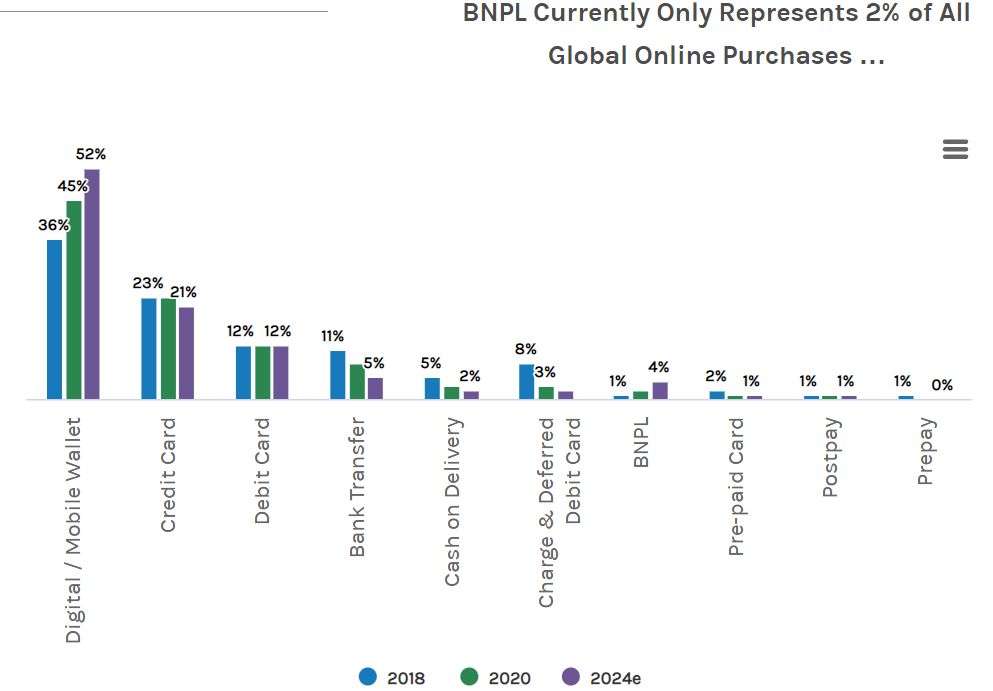

BNPL currently represents only a portion of overall global online purchases—2% in the U.S., 7% in Europe, 10% in Australia—but it’s growing. And our analysts say that the potential growth from the generational shift to this innovation cannot be underestimated.

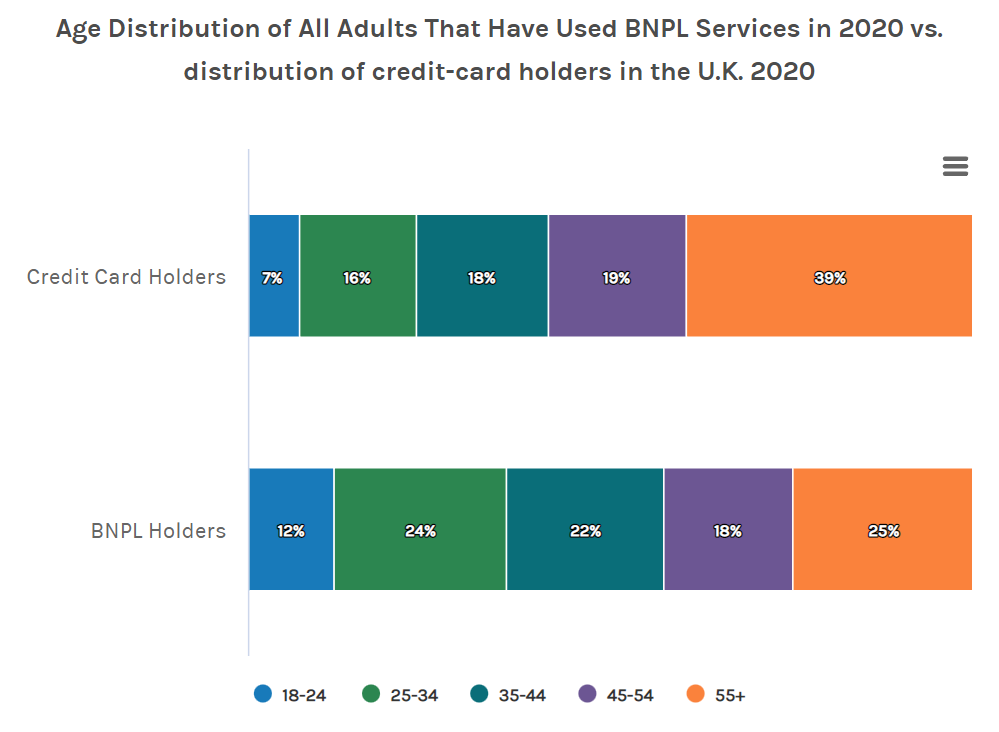

In a previous report, “How a ‘Youth Boom’ Could Shake Up Spending Trends,” Morgan Stanley noted that 73 million Millennials and 78 million Gen Z in the U.S. could be the “pillars of GDP growth,” even amid the ongoing pandemic. This points to significant implications for retailers in several categories, including the food and beverage industries, electronics and travel—and Fintech.

Many young, digitally minded shoppers have long-used peer-to-peer payments, and the overall share of retail spending by Millennials and Gen Z is expected to be as high as that of Gen X and older cohorts by 2030 across the UK, Australia and the U.S.

Here’s why BNPL brands and marketing resonate with Millennials and Gen Z:

- Simplicity and cost (they don’t charge interest, and late fees apply only if customers miss payments)

- Engaging apps that provide multiple features like wish lists, targeted offers and budgeting tools

- Products are merchant subsidized, and providers take on the credit risk

High Growth, Big Disruption?

Fintechs have raised more than $80 billion globally and $19 billion in Europe alone year to date, outpacing total fund inflows into the sector compared to the same period last year; and BNPL has raised $2.95 billion year to date in Europe, according to Pitchbook/Morgan Stanley Research.

Already there are big changes in the retail segment, where gross merchandise volume growth (i.e., the retailers’ sales to which BNPL companies charge a margin) reached 90% year-over-year in the last 12 months for the BNPL platforms Morgan Stanley tracks globally. The results are driving high valuations, even though a number of providers are losing money as they pursue growth.

Morgan Stanley views BNPL as an alternative payment method (APM). For analysts, that means that BNPL and the complexity of the payment landscape might accelerate with more APMs entering the marketplace.

In the short term, says Morgan Stanley Equity Analyst Andrei Stadnik, who leads Australian Non-Bank Financials Research, “We see limited impact to banks’ earnings, mostly related to a slower growth in credit cards. Over the long term, however, we see a bigger risk, and we stress the importance for banks of developing apps that are able to engage customers.”

While our analysts expect high growth, they warn against overlooking the regulatory risk that has already been seen globally. Still, they believe investors should focus on the new opportunity and potential longer-term impact on incumbents as mass adoption could boost several sectors.