Fra Bloomberg: At the height of the financial crisis, the unprecedented decline in swap rates below Treasury yields was seen as an anomaly. The phenomenon is now widespread.

Swap rates are what companies, investors and traders pay to exchange fixed interest payments for floating ones. That rate falling below Treasury yields – the spread between the two being negative – is illogical in the eyes of most market observers, because it theoretically signals that traders view the credit of banks as superior to that of the U.S. government.

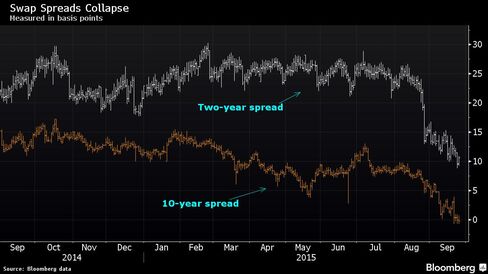

Back in 2009, it was only negative in the 30-year maturity, a temporary offshoot of deleveraging and market swings following the credit crisis. These days, swap spreads are near or below zero across maturities.

The shift is a result of a confluence of events, says Aaron Kohli, an interest-rate strategist in New York at BMO Capital Markets. It’s a ripple effect of regulations spawned by the credit crunch, combined with large-scale selling of Treasuries and surging corporate issuance.

“All of these effects have been pushing swap spreads the same way — lower,” Kohli said. “If this doesn’t go away after quarter-end, it could be the fact that a lot of the structural changes that have taken place in the marketplace are now manifesting. And this might then be one of the most visceral examples.”

In 2009, Gerald W. Buetow, co-author with Frank J. Fabozzi of a go-to textbook for pricing swaps, called the negative 30-year spread a “perverted” twist on historical patterns. The spread averaged about 60 basis points in the decade through December 2007, the month the recession began.

Swap rates serve as benchmarks for a variety of debt purchased with borrowed funds, including mortgage-backed and auto-loan securities. Narrower swap spreads can push borrowing costs lower even if Treasury yields hold steady.

Forgotten Tradition

Swap rates have traditionally exceeded Treasury yields because swaps pricing is based on the London interbank offered rate, which involves credit risk.

This week, swap spreads in seven-, 10- and 30-year maturities have traded below zero. The 10-year spread dipped below zero this week for the first time in three years and reached negative 2.44 basis points Friday, its lowest since September 2010. The two-year spread touched 7.56 basis points Friday, the narrowest in almost two years.

If the flip to negative spreads persists, it would signal that its roots are in regulators’ efforts to head off another financial crisis, according to Kohli.

Regulatory Ripple

Regulatory moves such as higher capital requirements have led banks to curtail market-making, crimping liquidity and driving repurchase agreement rates above bank funding benchmarks. Repo rates factor into Treasuries pricing because they’re considered the cost of financing positions in government debt.

Global market forces are also at work. Some strategists are pegging the narrowing of the two-year swap spread in recent weeks to selling of Treasuries by China as that nation’s central bank moves to stabilize its currency following the surprise yuan devaluation in August.

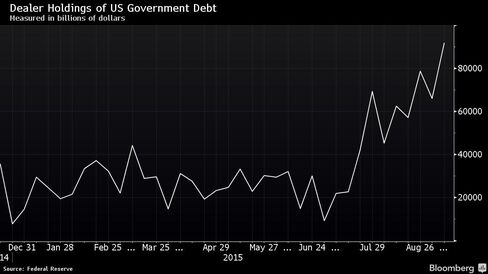

As speculation has swirled that China is selling shorter-maturity Treasuries while other investors dumped the securities before this month’s Federal Reserve meeting, dealer holdings of U.S. government debt climbed. That drives repo rates higher because dealers need more cash to finance those positions.

“There is a rebalancing of holdings by central banks and there is still a massive supply of Treasuries that has no end in sight,” said Ralph Axel, an analyst in New York at Bank of America Corp. “We see recent signs that China is selling and overall all central banks, including the Fed, are no longer the big supporters of Treasuries as they had been in recent years. This is narrowing spreads as it cheapens Treasuries.”

There’s a third component to the negative spreads: Companies are piling into the debt market to lock in low borrowing costs. They frequently swap the issuance from fixed to floating payments, which causes swap spreads to tighten.

Wrong-footed bets have also exacerbated the slide in spreads.

“Most people on the hedge-fund side had been long swaps spreads,” said David Keeble, New York-based head of fixed-income strategy at Credit Agricole SA. “But the rising repo rates and heavy corporate issuance really convinced a lot of people to capitulate and kill off the long-swap spread trades.”