Fra Mauldin Economics:

I am going to argue that there are five major weak links.

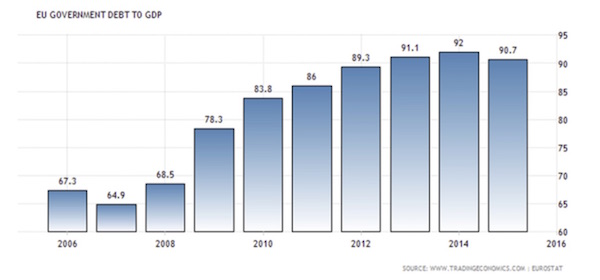

The first weak link is Europe and its debt. On average, across the continent, the debt-to-GDP ratio is about 90%. It is up to 135% and will soon be a 140% in Italy. Either Europe mutualizes all its debt and Germany says, “Ja, vee vill take it,” or the debt problem will continue to worsen. If they mutualize, they can put the debt on the balance sheet of the ECB, and then all the countries of the Eurozone will pinky swear to balance their budgets in the future, giving up their national sovereignty to Brussels.

A European treaty is actually what my teenage girls called a pinky swear. They mean it when they sign those treaties, but the problem is actually adhering to the treaty.

Today you heard Anatole Kaletsky tell us that Europe’s big problem is unfunded liabilities, and they will have to cut their pensions. Can anybody tell me how loud French pensioners will scream when their pensions are cut? Or what French farmers will get up to when their subsidies are cut?

I am suggesting to you that there might be some political problems brewing in Europe. (We will deal with the implications of Brexit and European cohesion at the end of the letter.) So Europe is a weak link – but maybe not the weakest. Remember the Weakest Link TV program? The lady would run through the questions, and then with that sharp British accent, she would say to a contestant, “You are the weakest link,” and the player had to walk off in shame. The weakest link could be Europe, but it could also be China.

Xi Jinping is the most powerful Chinese leader since Deng Xiaoping and will likely be compared by historians to Mao Zedong and Sun Yat-sen in his importance. He has taken China by the neck and is wringing it. He has at least five more years left in his term – and note my use of the words at least. This is a man who has decided, “I am going to take China into the next century. I have a vision, and we are going to do it.”

To succeed, Xi has to rid the Chinese system of endemic corruption and cronyism and build a consumer society. The problem is that you don’t create a consumer society from the top down; you have to do it from the bottom up. I could give you tons of research on that. It’s a basic economic axiom.

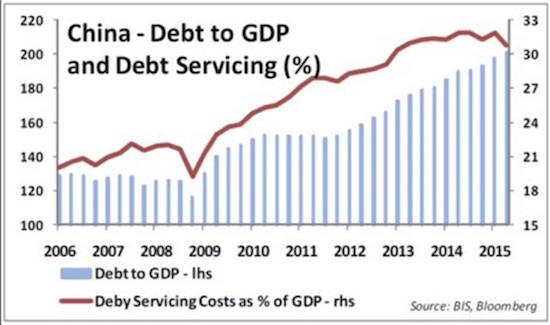

So, China has problems. Their debt has just ballooned. Depending on whom you want to listen to, 40% to 80% of the last $6 trillion the Chinese borrowed went to pay interest on the debt they already had. In less polite circles we would call that a Ponzi scheme.

Now, they do have a lot of money. Yes. Can they print more? Yes. Do they want to have a New Silk Road? Do they want to be the world’s reserve currency? Do they want to be the most powerful country in the world? Of course they do. You get into private conversations with Chinese who are hard-core Chinese, and you can see their dreams. Their vision is not unlike the spirit of “Manifest Destiny” that moved the United States westward in the 1800s. We saw ourselves building an empire. The Chinese see themselves rebuilding their own ancient empire.

You don’t do that on the back of a weak currency – but then we come to the problem of a strong Chinese currency. Oh, by the way, their debt service is up to 30% of GDP, but that’s a detail that is mostly overlooked. (Please note more than a hint of sarcasm.)

Weak link number three is Japan. I have been talking about Japan for years. The line I coined six years ago is one that everybody tosses around now: “Japan is a bug in search of a windshield.” Japan is doing exactly what I said it would do in my book End Game five years ago and in Code Red over two years ago. It will get honorable mention in the next book.

Japan is monetizing its debt and putting it into the central bank. They are going to continue doing this at an astounding rate. I shorted the yen when it was at 100. I should have shorted it when it was at 90, because I was already writing about it then, but at the time I didn’t have the money or the testosterone. I was a lot happier when it was at 125 than now when it is back down to 102. One of the things I try to avoid when I place money with money managers is a “true believer.” A true believer’s certainties can take you over the cliff. But I must confess to being a true believer about the ultimate weakness of the yen. I still think 200 is a real possibility. For what it’s worth, I still have my money exactly where my mouth is. Only now, the cash value is back to where I started almost 2½ years ago. Oh well… We true believers are a hardy bunch. By the way, have I introduced you to some of my gold bug friends? And then there’s the survivalists. Just saying…

The Japanese have placed 30% of their total government debt on the balance sheet of their central bank. It is going to 70–80% – count on it, says the true believer. That is a lot of yen to put into the system, and that is what I think drives the ultimate valuation of the yen.

Emerging markets are the fourth weak link. How do they dig out? They borrowed $10 trillion in dollars that they have to pay back from income earned in their local currencies. Dollar valuation can create serious problems for their debt. And it happens at the worst possible time, during a crisis or global recession when the US dollar is the cleanest dirty shirt in the closet. The value of the dollar will rise at precisely the time when the profits and tax revenues of the emerging-market corporations and countries will fall.

Then there is a final weak link – and that is us, the US.

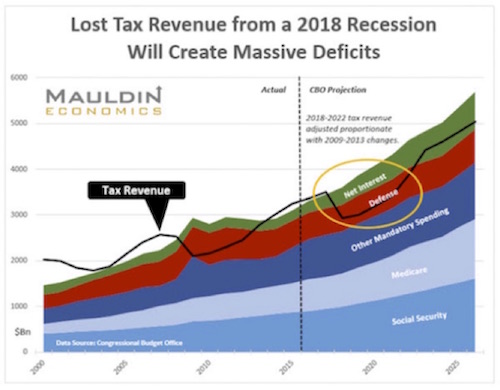

We are the most global, powerful, incredible, fabulous country in the history of the world. But here is our problem. When we next fall into recession, the deficit explodes to $1.3 trillion, even if we lose only the revenue we lost last time. If we have to add in the extra cost of safety nets, it’s $1.5 trillion minimum, plus the almost three quarters of a trillion dollars of “off-balance-sheet” debt. US total debt will be rising at over $2 trillion per year in short order.

All in, we are adding $2 trillion plus a year to an already huge total national debt. In five years we could be at $30 trillion debt. We are into 2020 and we are now facing $30 trillion in debt and people are going, “Whoa, what the hell are we doing?” You think there is angst today in the Tea Party?

Lacy Hunt is right: debt constrains growth. It constrains nominal GDP; and if we don’t get nominal GDP, we won’t get wage growth; we won’t get the labor participation rate up; we’ll get more of the gig economy; we’ll get a recession where we are back to 8–9–10% unemployment. People are going to be upset. Juan Williams may be right that Clinton is a shoo-in. That may be the best thing that ever happened to Republicans, because she will have to figure out what the heck to do, and she has no clue. Because it doesn’t make any difference which of these links breaks. We are all connected. The whole chain breaks.

When it breaks, the result is a global recession every bit as serious as the last one; it’s just different in its causes and effects. But there is a common denominator in each of the weak links mentioned above: Debt. And I do mean debt with a capital D. You can’t just wish debt away or declare a jubilee, because there are banks and pension companies and you and me on the other side of that debt. Somebody owns that debt, and that somebody is you and I in our pensions, in the insurance we buy, in the bond funds in our portfolios, in our foundations, our banks, and corporations. Those bonds silently permeate every part of our lives. Kill them and it all goes pear-shaped.