Uddrag fra Authers:

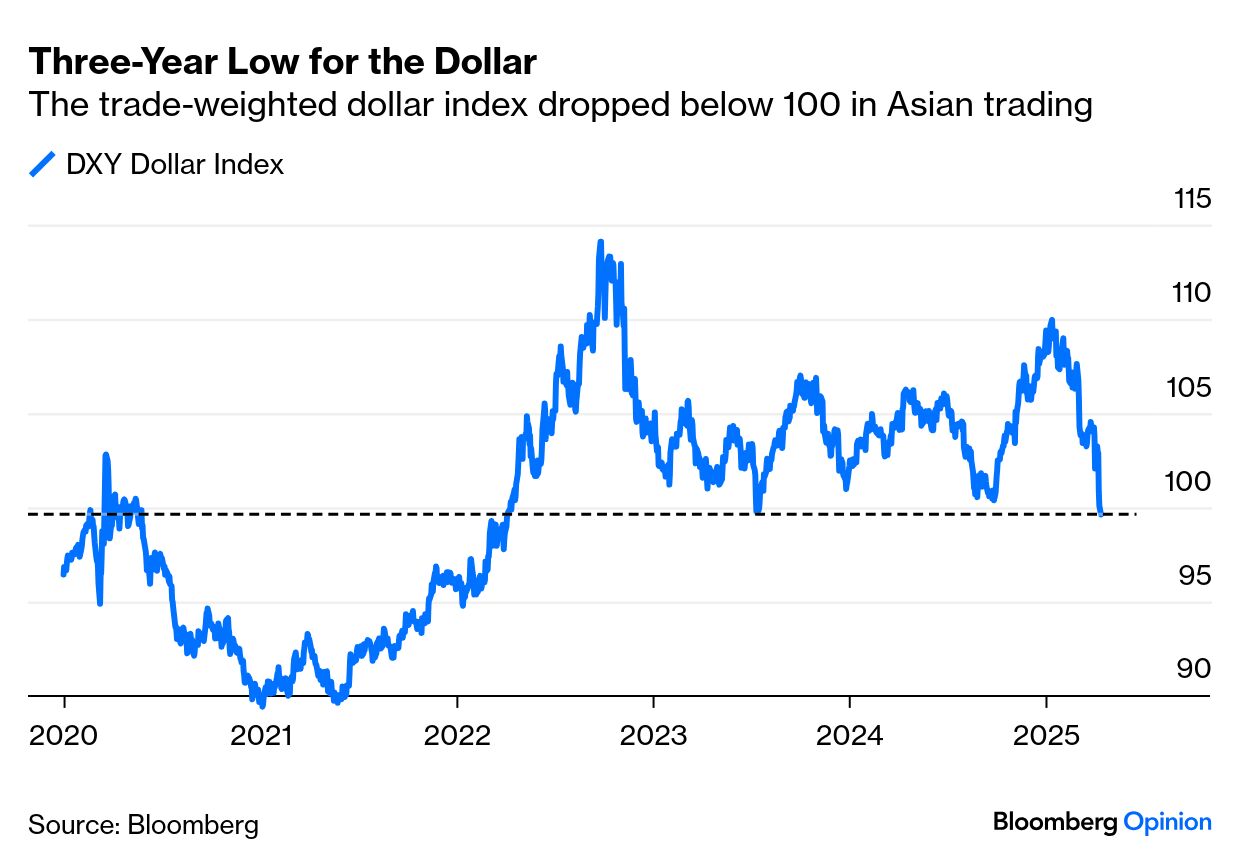

Why is the dollar falling, even though Treasury yields are rising?

Usually, the bond differential is a crucial currency driver. Money flows where it can get the higher yield. Except recently. In early Asia trading, the DXY dollar index dropped to a three-year low:

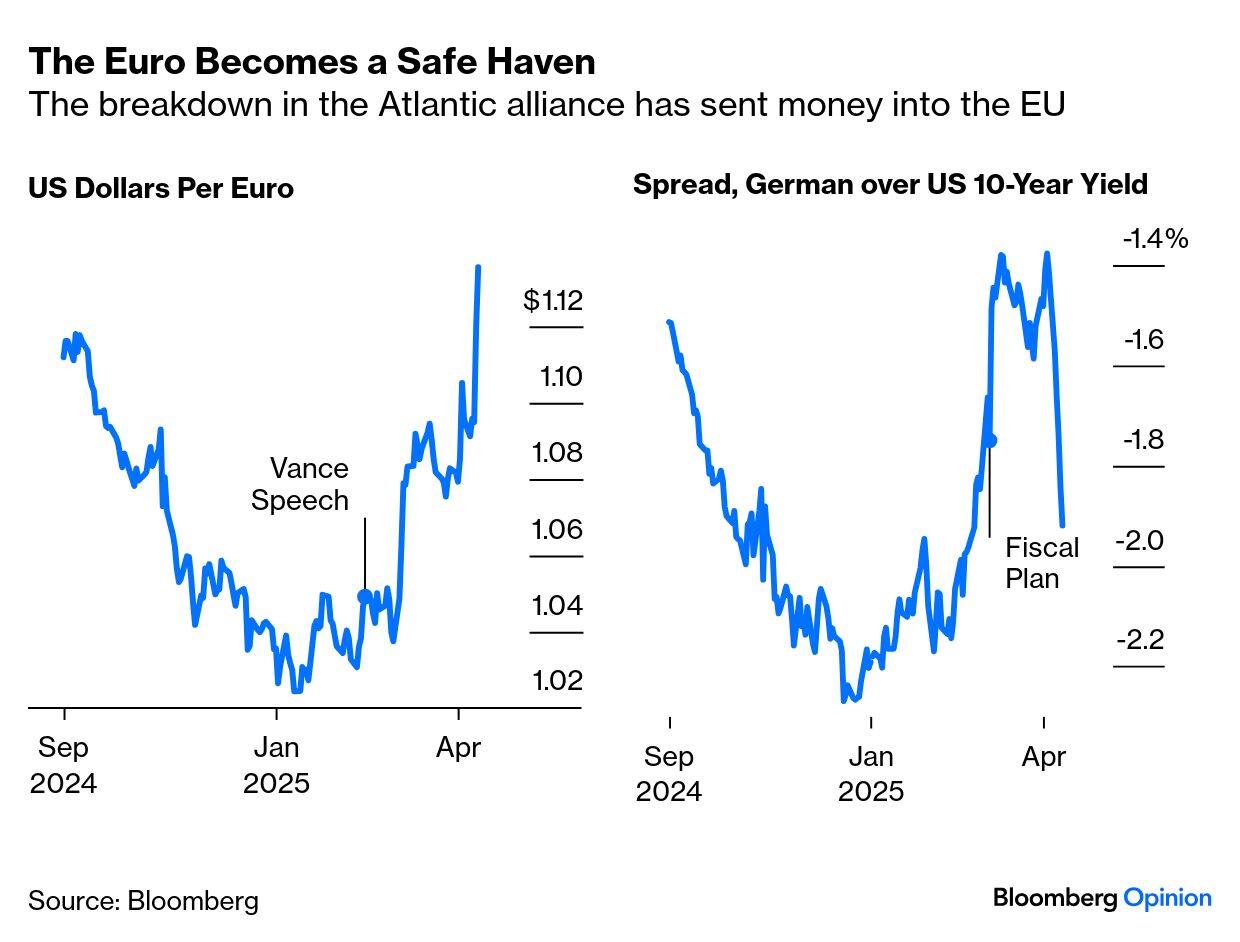

After US Vice President JD Vance launched his attack on Europe two months ago, Day, prompting a desperate European attempts to beef up their defense, the spread of German over US yields ballooned but then came straight back down. Meanwhile, the euro has surged upward. If you’re reading this on the terminal, try opening this chart in GP so that you can look at it on two scales overlaid, which will make the divergence even clearer:

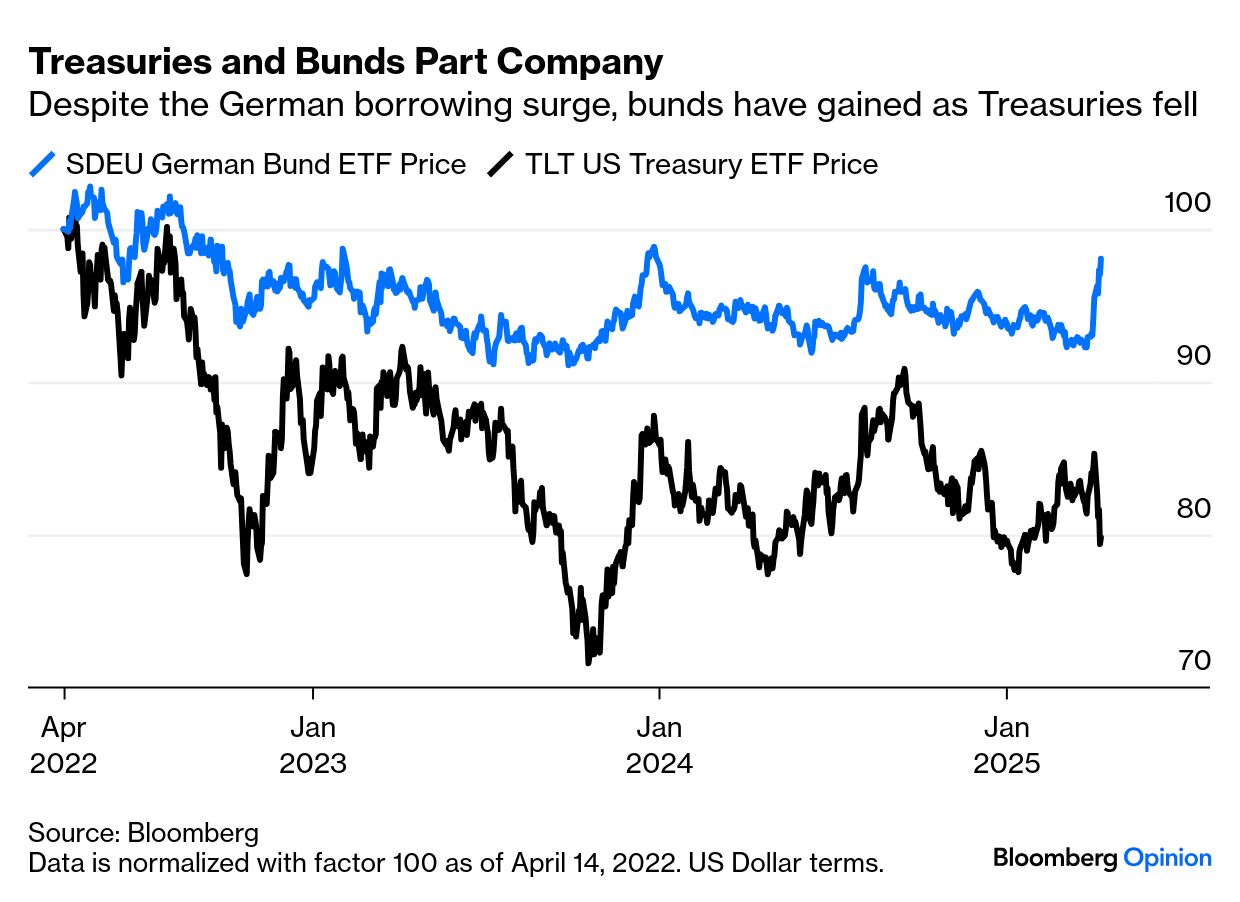

A further weirdness post-Vance: Germany is now going to borrow far more, which should make its bonds less attractive. The US is taking a chainsaw to the federal budget in a brutal attempt to cut the deficit and borrow less. But the prices of bunds and Treasuries, as measured via exchange-traded funds tracking them, show that Germany has gained while the US has dropped. This is stunning:

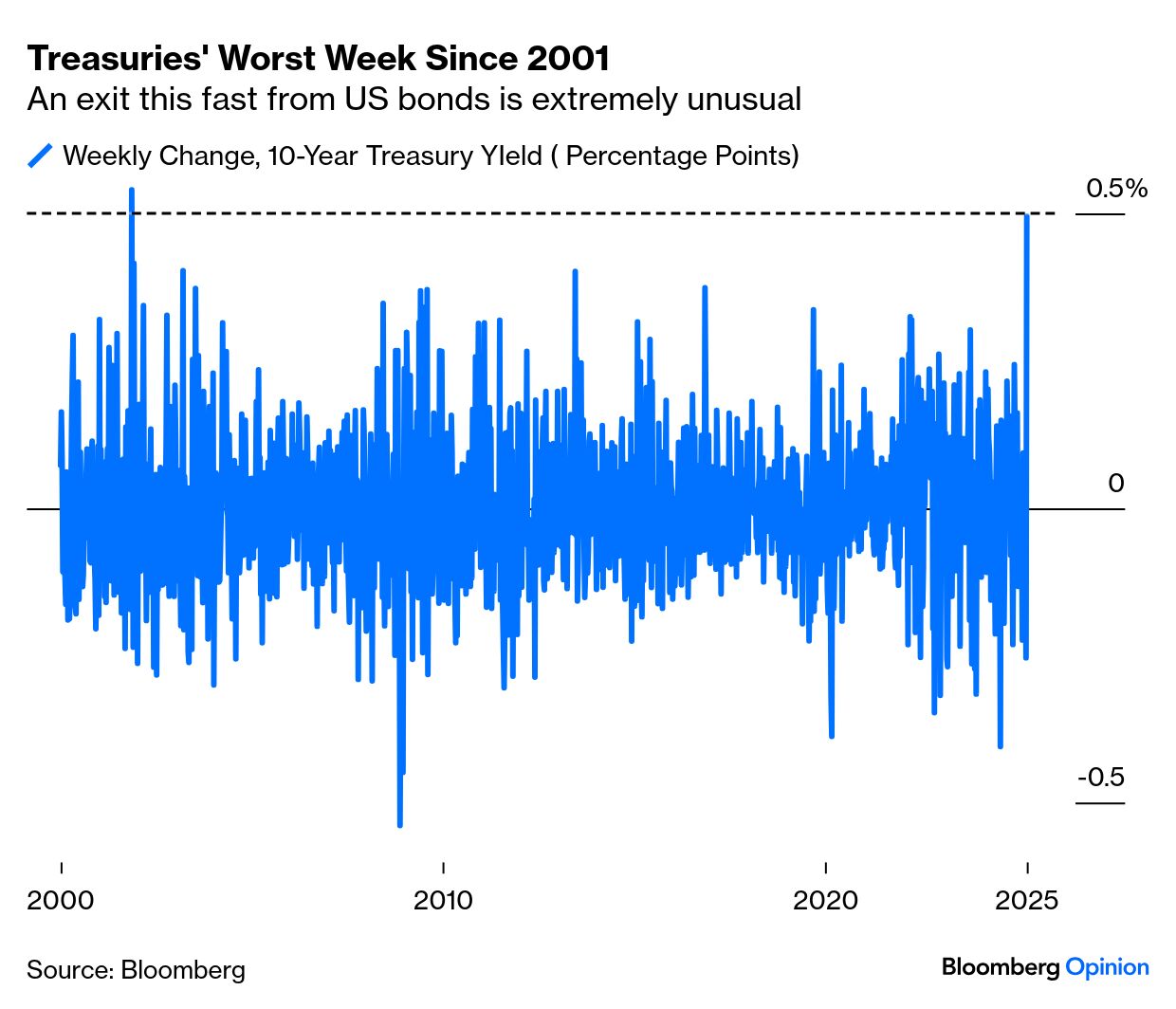

It’s true that US yields still aren’t all that high. At Friday’s close, the 10-year yielded just under 4.5%; it hit 4.8% in January, and briefly topped 5% in 2023. But the speed demands attention — it gained 50 basis points last week. The last time that happened was in November 2001:

Another problem: The week’s price action tends to confirm that bond yields are in a rising trend that started five years ago. Such things matter in the bond market, which tends to follow long cycles:

Put all these together, and the only explanation is a loss of confidence in the US as a destination for funds. Last week’s combination of rising yields and a falling currency is reminiscent of any number of emerging markets crises, and of the one for gilts and sterling that followed Prime Minister Liz Truss’s unfunded UK tax cuts in 2022. It’s amazing that such a fate can befall the US. Truss capitulated and sterling rebounded; that’s generally the pattern that emerging crises follow. Amazingly, that is now the template for the US.

Why is the US making concessions to China, when it appears that Beijing has far more to lose?

Trade is more important to China than to America, and its economy is in a more dubious place at present. But game theory (and common sense) show that what matters most when dealing with an aggressive bully is pain threshold. If you can soak up more pain than they can, you’ll prevail, even if it hurts.

Trump owes his election in large part to popular anger over inflation that peaked at less than 10%. In China, the Communist Party killed millions during the Cultural Revolution; set tanks on peaceful protesters in Tiananmen Square; and only three years ago imposed Covid lockdowns far more draconian than anyone else, which by then were clearly excessive. China’s leadership evidently has a far higher threshold for the pain it will inflict on the population before conceding.

It also has a much more prevalent myth of mistreatment by the rest of the world, reinforced by Vance’s extraordinarily offensive soundbite that the US was buying products made by Chinese peasants. Xi Jinping has far greater control over his media than Trump.

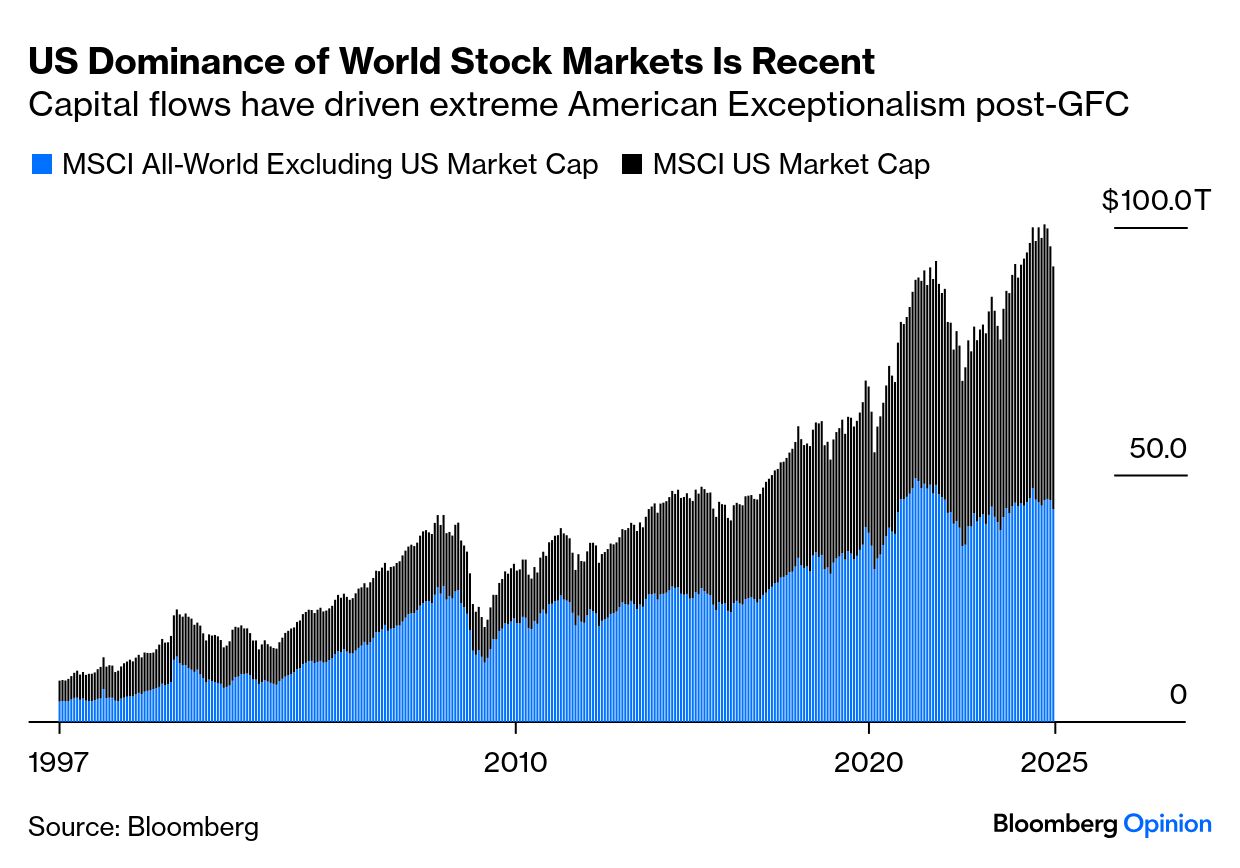

Additionally, the US position is weaker than it appears. Much of its Treasury debt is in foreign (particularly Chinese) hands. The stock market is worth more than all the others put together, even though its economy is only about a quarter of global GDP. This is a recent development, and means that the US has much more to lose from capital flows — which can adjust far more quickly than trade flows:

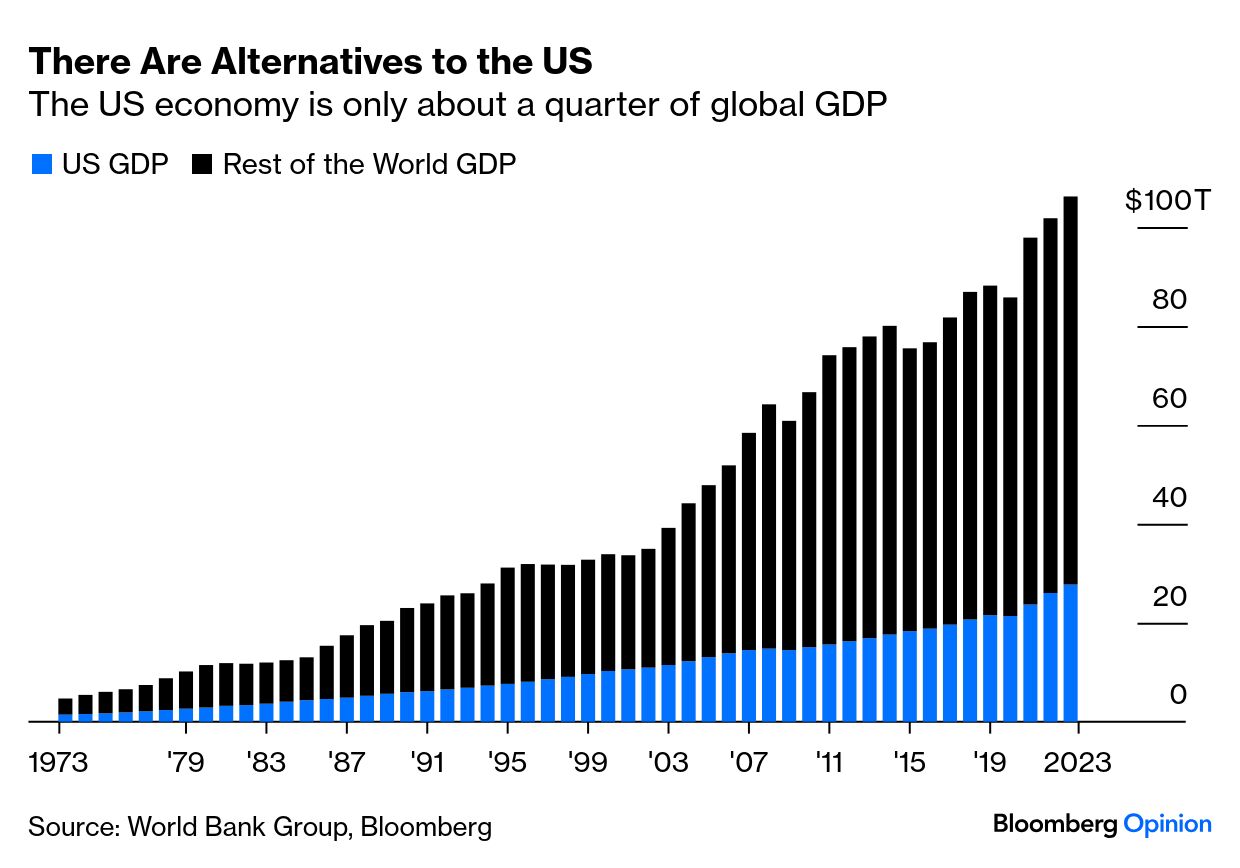

Also, steady global economic growth increases potential trade with other countries. Yes, a trade war with the US would hurt, but there are alternatives:

The US has more to lose than anyone else, because it starts with more. That’s why it shouldn’t be surprising that China is retaliating while calling the US policy a “joke.”

What’s up with these China tariffs? Are they on, off, delayed? How is anyone supposed to make sense of this?

OK, this question doesn’t fit the Passover format, but it’s on everyone’s lips. Thursday brought confirmation of a 145% US tariff on all Chinese imports from the US. Friday came the announcement that laptops and phones (the most significant of those imports) were to be excluded. And then on Sunday morning talk shows, Commerce Secretary Howard Lutnick said that reprieve was only temporary, and the president said he would look at “the whole electronics supply chain.”

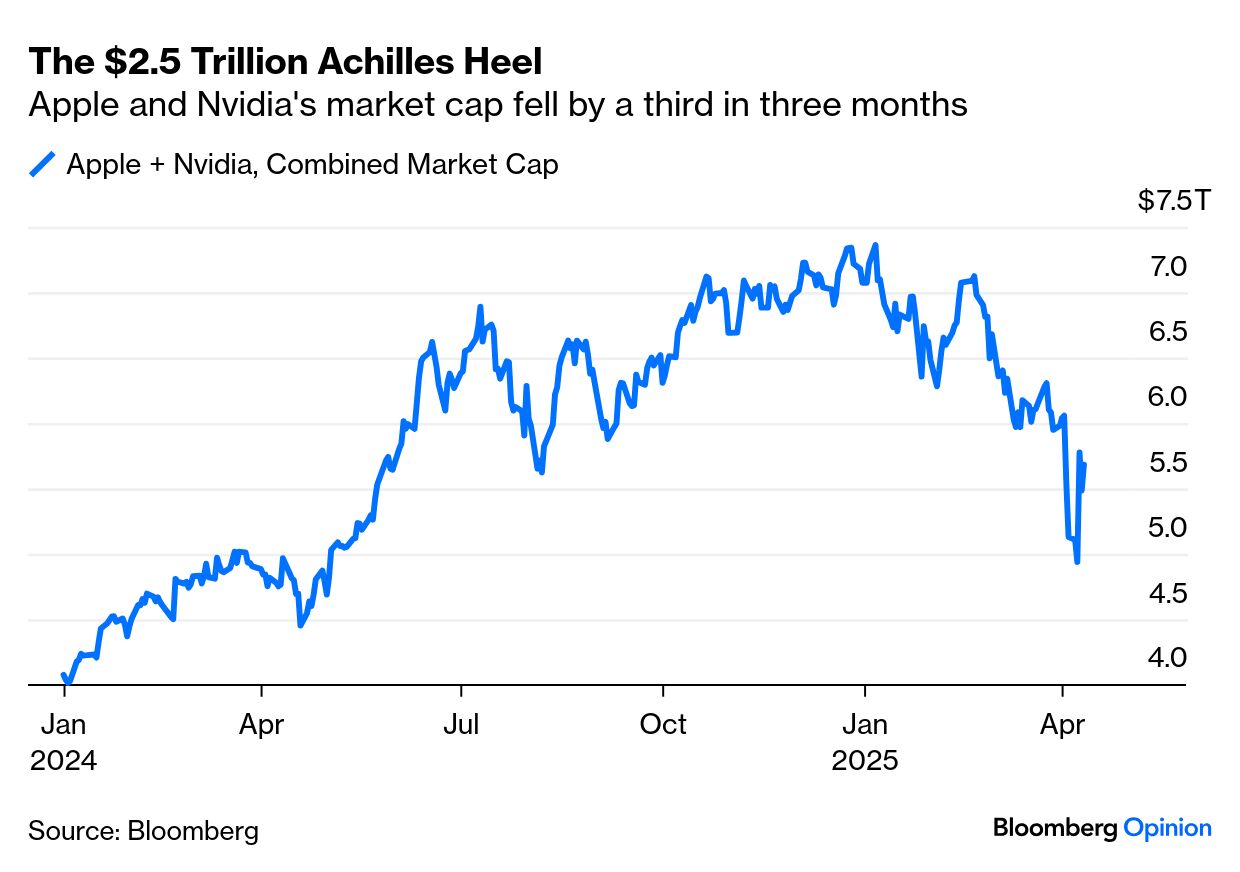

The most important message is that the administration grasps that there are limits on how much pain it can inflict on the business models of Apple Inc. and Nvidia Corp., which each were recently worth more than $3 trillion. In the last three months, their joint value dropped by a third, or more than $2.5 trillion:

It’s been popular of late to argue that the administration can happily let the stock market fall, as many Americans aren’t exposed to it. But the people who fund Trump tend to be rich, and they’re grievously hurt by this. If last week’s step back acknowledged that he couldn’t stare down the bond market, the weekend moves on electronics also suggest a Trump Put at which point he’ll intervene to help out stocks.

The bottom line for markets: The US is in a weak place and making concessions. That’s good news compared to the last couple of weeks, so an equity rally at Monday’s open seems likely. That said, the sheer ad hoc nature of policymaking over a sector as important as iPhones and laptops shows ever more conclusively that the children are in charge. This is amateur hour, and terrifying. Ultimately, nobody can give a confident answer to the fourth question. Risks and volatility are likely to continue.