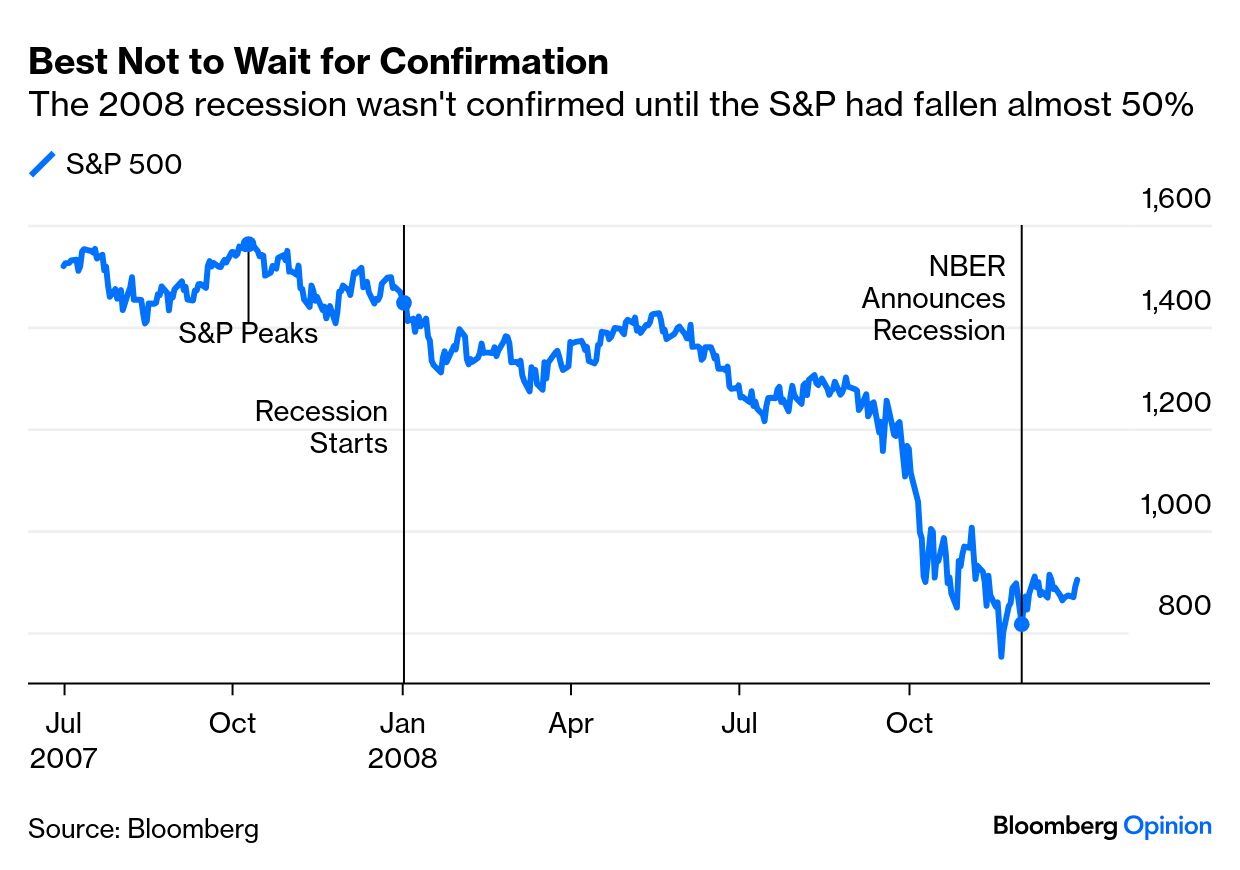

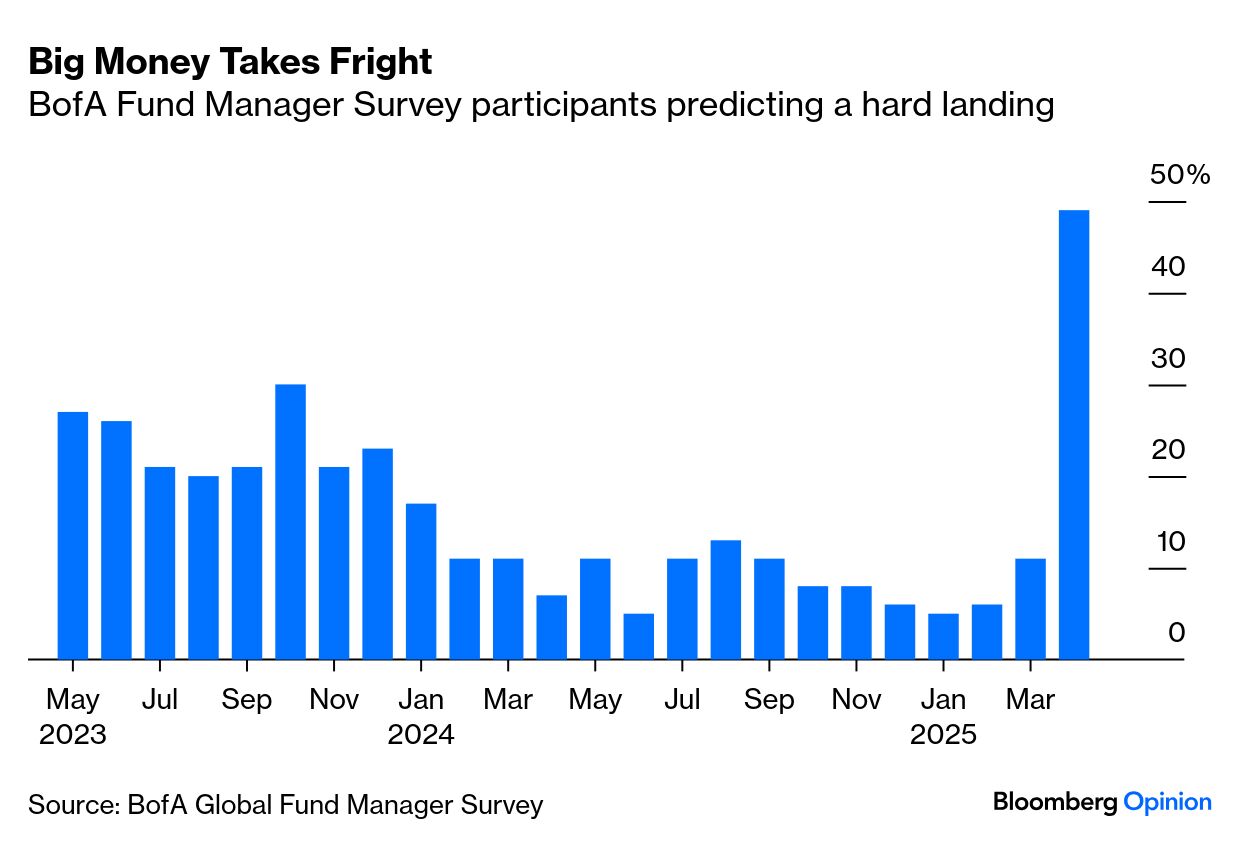

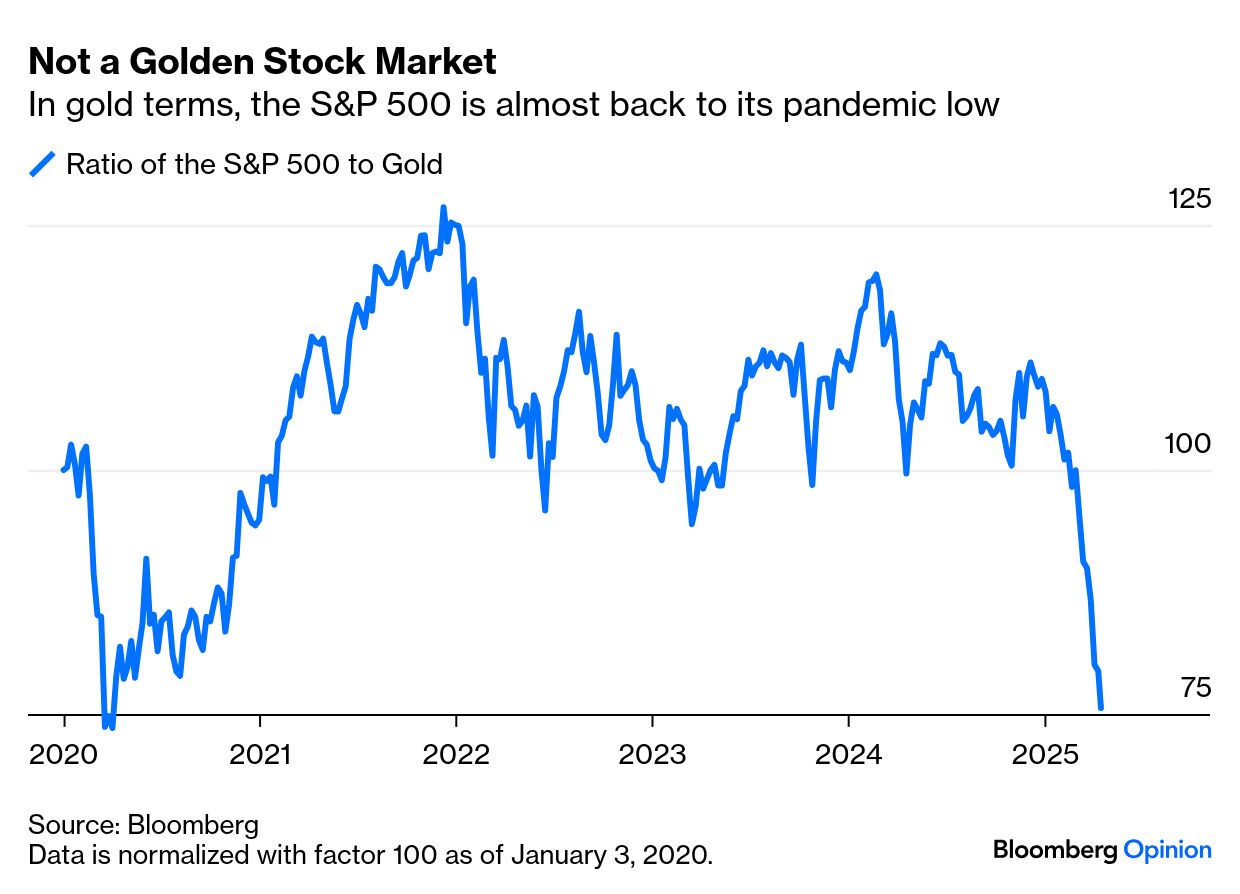

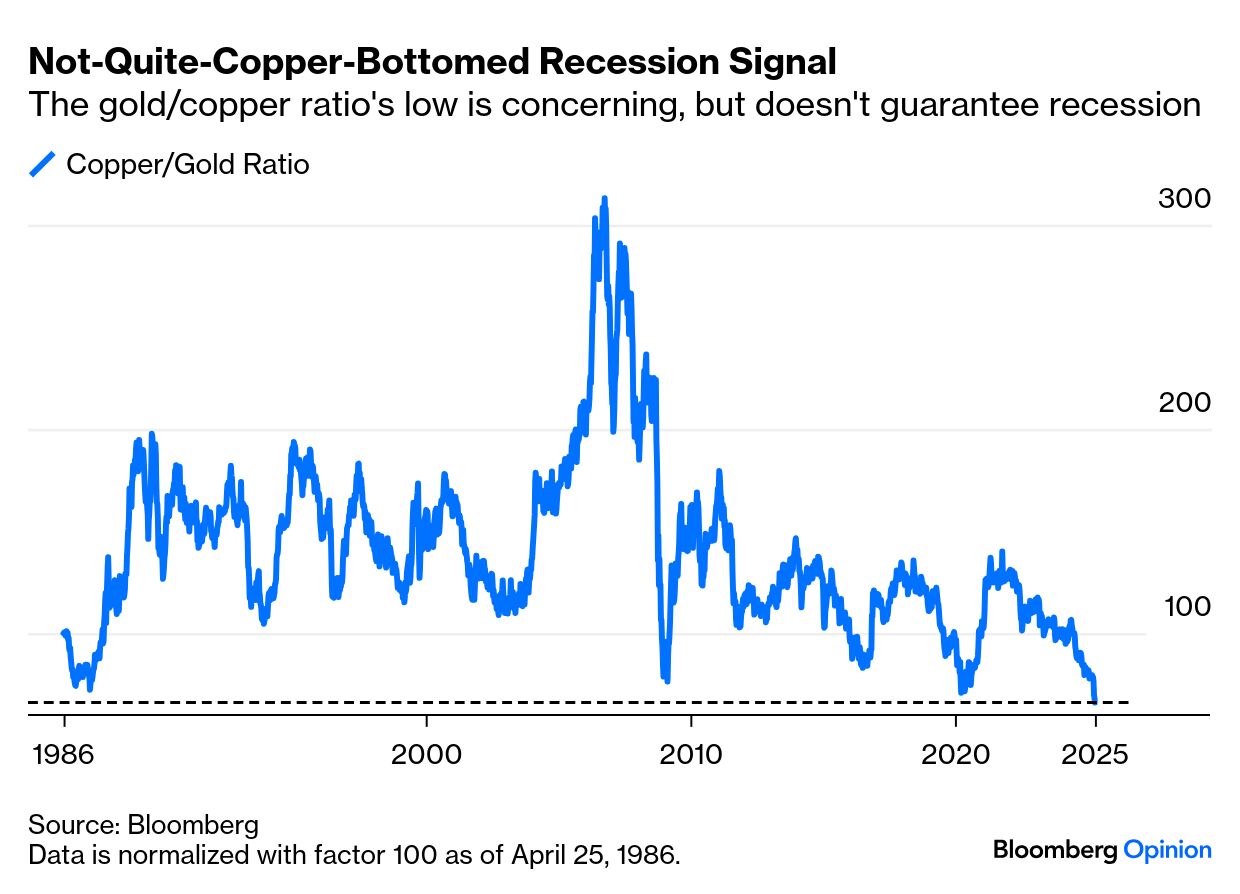

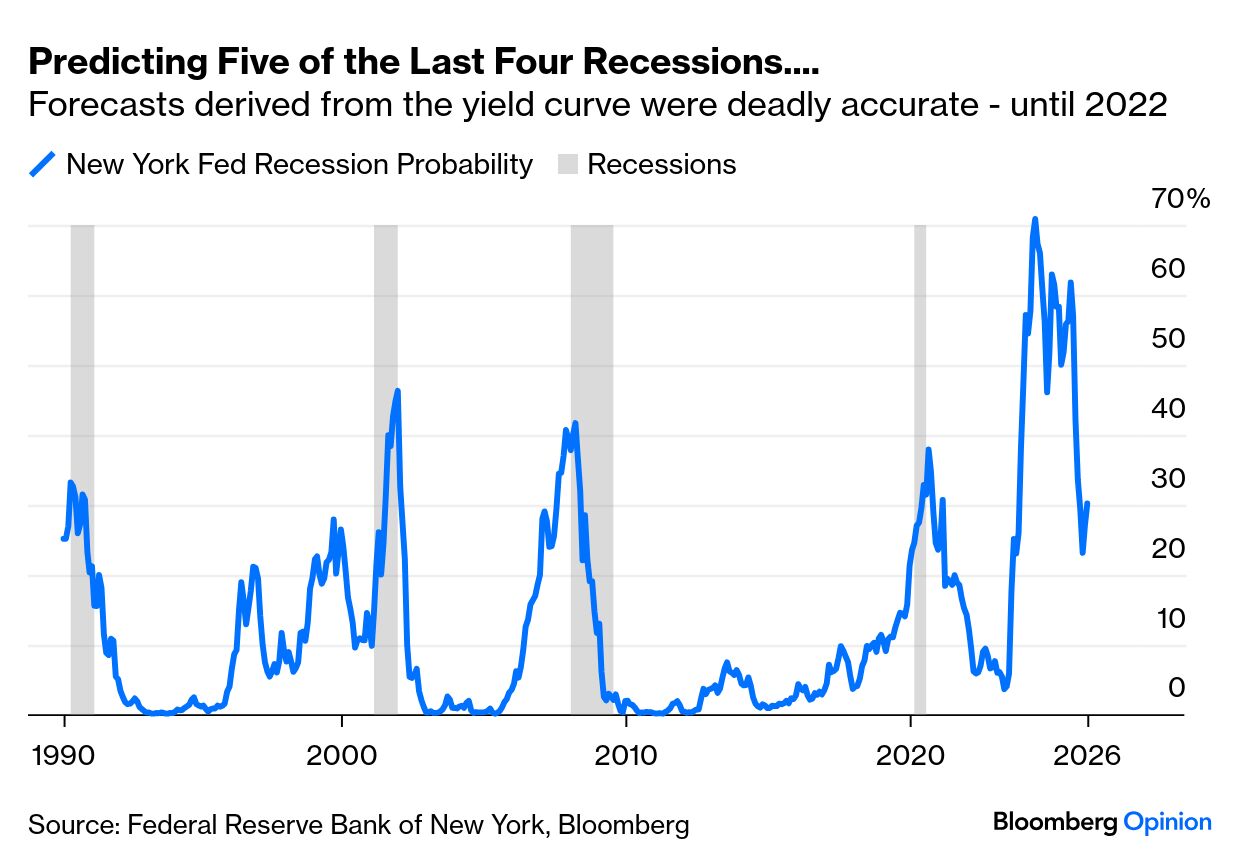

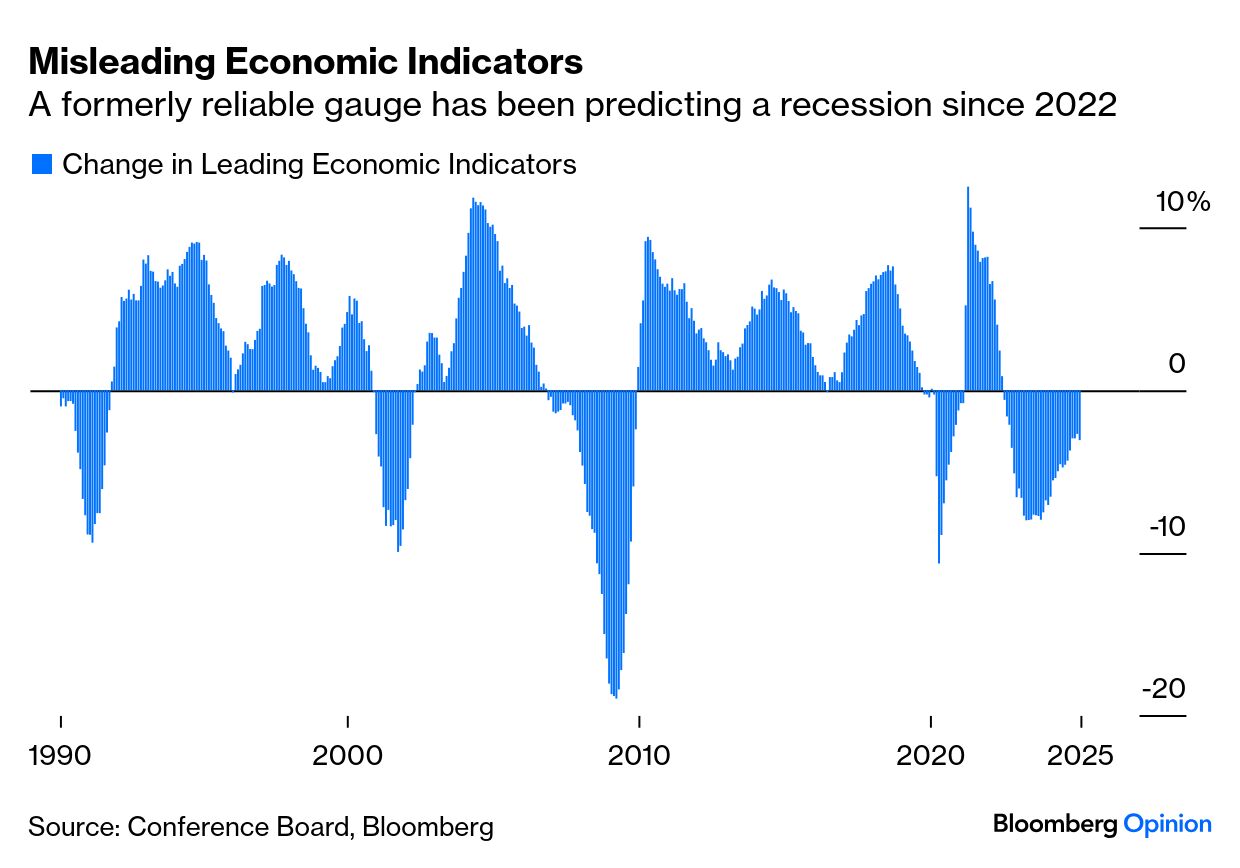

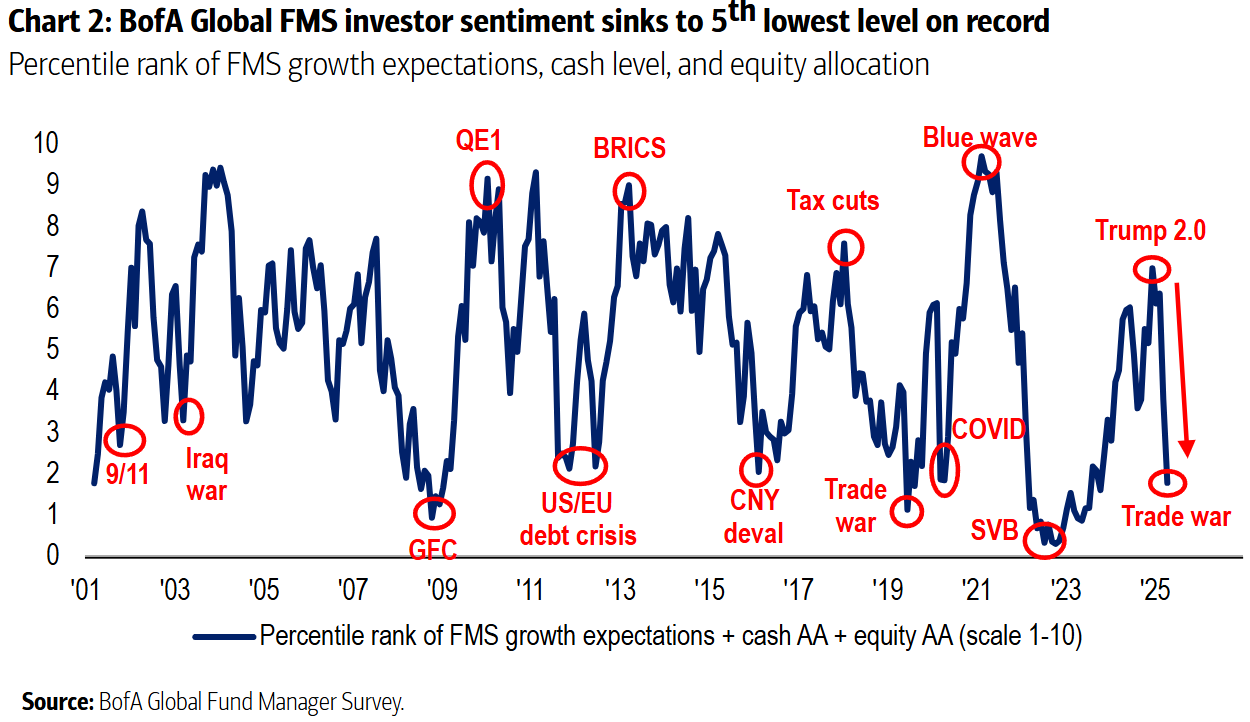

| When you think a recession is coming, it generally pays to sell first and ask questions later. Waiting for confirmation that the economy is declining is just too costly. For a spectacular demonstration, look to the events of 2008, when the National Bureau of Economic Research announced that a recession had started in January of that year — but didn’t announce this until December: From the start of the recession to the NBER’s acknowledgement, the S&P 500 almost halved. It was better to take a judgment first. That’s why there’s particular interest in the latest survey of global fund managers by Bank of America Corp., the first since the “Liberation Day” tariffs announcement, which showed a dramatic increase in fears of an economic hard landing: If big fund managers take fright, then their actions can guarantee a market selloff as they move their money to safety. And they’re not the only ones growing much more nervous. Odds of a recession this year have ballooned on the Polymarket betting site, and now stand at more than 50%: Traditional indicators of market negativity show a similar trend. The total assets of State Street Global Advisors’ GLD exchange-traded fund, the biggest fund for retail investors to buy gold, topped $100 billion for the first time Wednesday, as a rising price and growing interest from small investors combined: (Parenthetically, the gold rally provides vital context for the stock market. The ratio of the S&P 500 to the gold price, which effectively prices the index in gold rather than dollars, has tanked this year and is almost back to its pandemic-era low. If you choose to view the post-Covid rally as one big side effect of cheap money, this would tend to support you.) Combining gold with copper provides another alarming recession signal. The former rises when people are worried, while a gain in the latter shows that economic activity is expanding. So when copper drops to its lowest in gold terms in at least 38 years, that’s concerning (although it’s worth noting that the previous low in 1987 didn’t prefigure a recession): There’s another problem with making a confident recession prediction. Formerly reliable market indicators have been foretelling one for so long without success that it’s getting harder to take them seriously. The New York Fed recession probability indicator is based on the bond yield curve. Over time, an inverted curve, in which long bonds yield less than shorter-term instruments, has been a surefire sign of trouble ahead. But it’s never been more confident of an oncoming recession than it was in 2022, and so far it hasn’t come to pass: Another virtually foolproof signal comes from the Conference Board’s Leading Economic Indicators, which smooshes together various measures of the economy and market. Just like the yield curve, it successfully predicted the last four recessions, but also a fifth that still hasn’t happened: One problem with getting out of the market when everyone is scared of a recession is that this is often a great contrarian time to buy. The American Association of Individual Investors has for decades asked its members a weekly question: Are you bullish or bearish? The recent peak in the majority of bears over bulls makes this the fourth-biggest incidence of bearishness since 1987. Here it is in context: All were either good or great times to buy, with the significant exception of the angst over subprime bankruptcies in January 2008, when a few months later investors discovered they hadn’t seen nothing yet. Similarly, BofA has a measure of sentiment based on how much cash fund managers are holding, their hopes for growth, and the amount they’ve allocated to equities. With the exception of the response to the 9/11 terrorist attacks in 2001, all the previous times when sentiment dropped this low proved decent times to buy: A further problem: The recession fears this time around have been driven entirely by a new policy (US tariffs) that might yet be revoked. The chances are that it will create an epic buying opportunity at some point in the future. But that time to buy will come much later if there is a recession. While the uncertainty over tariffs persists, it will be hard to put together a market rally. |