Resume af teksten:

Japans inflationsrate faldt til 1,8% i februar, hjulpet af statslige energi-subsidier, men underliggende prispresset forbliver stædigt, især inden for tjenester. Utilities-priser, herunder elektricitet og gas, faldt med 6,6% i februar. Med de stigende omkostninger i serviceindustrien forventes inflationen at forblive under 2%, hvilket kan støtte Bank of Japans forsigtige renteforhøjelser. Industriproduktionen steg med 2,2% i januar, bl.a. drevet af en robust genopretning i bilsektoren, og detailhandlen øgedes med 4,1%. Den stærke detailhandel indikerer, at privatforbrug kan føre til økonomisk vækst i første kvartal. Forventningen er at se accelererende BNP-vækst, hvilket yderligere understøttes af lavere inflation og en positiv udvikling på aktiemarkedet.

Fra ING:

Japanese government measures helped to ease inflation, while industrial production and retail sales improved. The Bank of Japan is expected to maintain is normalization process, but proceed cautiously with rate hikes

Tokyo core inflation excluding fresh food

Core inflation continued to cool, falling below the BoJ’s target

Japan’s core inflation excluding fresh food eased to 1.8% year-on-year in February (vs 2.0% in January, 1.7% market consensus). Government energy subsidy measures drove inflation lower quite meaningfully. Utility prices, such as electricity and gas, fell further by 6.6% in February compared to -2.2% in January. Cereal prices (mostly rice) grew notably less, from 11.3% in January to 7.5%. The high base for rice prices will continue to weigh on inflation throughout this year. Energy subsidies will end soon, so we expect temporary volatility in monthly changes. Yet, other government welfare programs, such as free tuition, are likely to lower inflation in the latter part of the year.

Although core inflation eased, we believe underlying price pressure remained sticky, as most of the price decline was driven by goods rather than services. In a monthly seasonally-adjusted comparison, inflation fell 0.1% month-on-month, with goods prices down 0.6% and services up 0.2%.

Energy and food prices dropped while underlying inflation remain sticky

Source: CEIC

The BoJ will need additional evidence to hike rates

Going forward, inflation is expected to stay below 2%. Yet, service prices, primarily driven by rising labour costs and strong demand, are likely to remain firm. This is expected to support the Bank of Japan’s policy normalisation of modest rate hikes. We believe it’s important to monitor April inflation data since that’s when many businesses set new prices based on their costs — at the beginning of the fiscal year. As we mentioned in an earlier publication , the recent BoJ board nominees who lean towards dovish policies will require stricter criteria to be met for rate hikes. Therefore, the BoJ is expected to act in June, once the results of the spring wage negotiations and the April CPI figures have been confirmed.

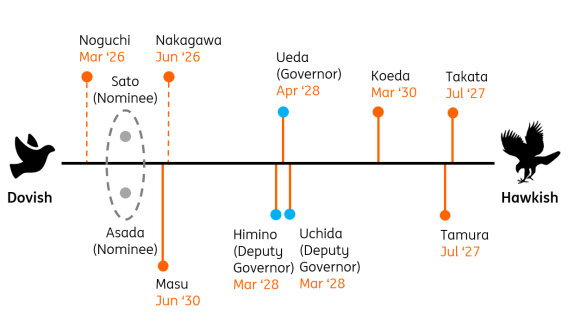

The dove-hawk balance may not change meaningfully with two new dovish-tilting nominees

Source: Bank of Japan, ING estimates

Industrial production

Auto sector recovery helped drive monthly data improvement

Industrial production and retail sales rebounded in January, suggesting GDP growth will accelerate in the first quarter. IP rebounded 2.2% MoM in January (vs -0.1% in December, 5.5% market consensus) and retail sales also were up 4.1% (vs -2.0% in December, 1.5% market consensus). Details of both data were quite encouraging, as gains were widely spread. But also, the improvement in auto sector activity was quite impressive. Motor vehicle output rose for the second month, by 9.1% in January, following a 1.4% gain in December. Shipments rebounded to 8.8% after dropping in the previous two months. Motor vehicle retail sales surged 12.5%.

Stronger-than-expected retail sales data indicate that private consumption will lead growth, supported by strong wage growth. We believe lower inflation, helped by subsidies, will partly enhance consumers’ purchasing power. Also, the recent rally in the local equity market should contribute positively to consumption. Today’s data support our view that GDP is expected to accelerate in 1Q26, driven by solid exports and consumption.

Retail sales rebounded firmly in January

Source: CEIC

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.