Uddrag fra Zerohedge/Goldman

Update (1300ET): Hours after Goldman’s Jan Hatzius confirmed the bank’s new expectation that The Fed will not hike rates in March (next week), let alone consider a 50bps rise; Barclays’ Marc Giannoni and the Economics Research team is out with a report forecasting no hike at the upcoming FOMC meeting, justified by risk management considerations as financial stability concerns move to the forefront.

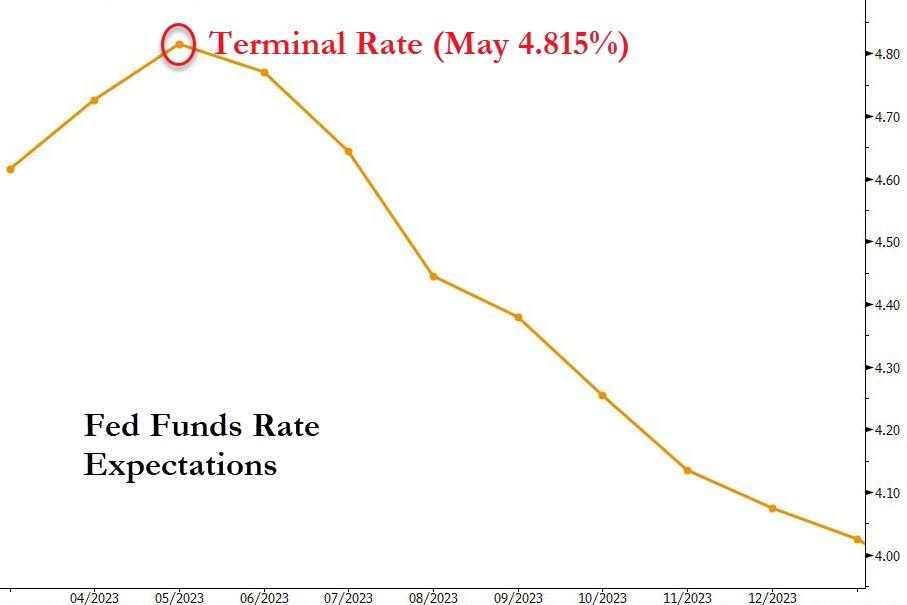

The market is now pricing in a coin-toss (0 or 25bps) for March, but expects the full 25bps in May…

Their flip-flop – from forecasting a 50bps hike just last week – to a pause is driven by the financial market turbulence over the weekend, and signs of a sudden intensification of risk aversion (outweighing their interpretation of incoming data, including from the US labor market, in combination with Chair Powell’s willingness to consider a return to aggressive hikes).

Additionally, Barclays lowers its terminal rate expectation to 5.1%…

We emphasize “pause” because we believe that the turmoil is likely to be contained in the coming weeks, especially following the backstops implemented over the weekend. We continue to believe that the Fed will see additional hikes as the baseline scenario, which it would carefully condition on an assumption that markets settle and that credit continues to flow from regional banks. Although recent distress will temper the appetite for additional aggressive hikes, we think that March’s dot plot will show the median dot peaking at 5.1% in 2023.

Which is still above the market’s 4.815% terminal rate expectation currently…

Even with financial stability considerations overshadowing data, Barclays does warn that a number of key prints will be released over the course of this week that will inform the evolution of rates at the coming meetings, including tomorrow’s CPI print for February and Wednesday’s estimates of retail sales.

* * *

Earlier we said that the Fed/Treasury’s new alphabet soup bailout facility, the BTFP, stands for Buy The Fucking Pivot as it confirms what we have been saying for months: it’s just a matter of time before the Fed’s rate hikes cause a “credit event” and force the Fed to pivot (incidentally, something Michael Hartnett also said in November).

Of course, before a Fed “Pivot” we need to go through a brief “Pause” period, and moments ago Goldman – which was dead wrong on its call for “transitory inflation” in all of 2021 and which for much of 2022 and early 2023 claimed that the Fed will keep hiking “higher for longer” – just admitted it was wrong again in expecting more hikes, and responded to our rhetorical question from yesterday in which we asked if “the Fed is going to keep hiking as the government backstops banks on the verge of failure due to high rates?”…

… by saying that the Fed is done.

Below we excerpt from a note just published by Goldman’s chief economist and (former) uber-hawkish preacher, Jan Hatzius, who just threw in the towel on more rate hikes. Expect the rest of Wall Street to follow in the next few hours.

The Treasury, Federal Reserve, and Federal Deposit Insurance Corporation (FDIC) made two major policy announcements intended to stabilize the banking system in response to recent bank failures and the risk of continued deposit outflows. We expect these measures to provide substantial liquidity to banks facing deposit outflows and to improve confidence among depositors. In light of recent stress in the banking system, we no longer expect the FOMC to deliver a rate hike at its March 22 meeting with considerable uncertainty about the path beyond March

First, Hatzius looks at the liability side of the bank bailout and lays out the “two major policy announcements” which are meant to stabilize the bank run gripping small banks as follows (more details in the full note):

The FDIC has used the ‘systemic risk exception’ (SRE) to protect uninsured depositors in two bank resolutions, Silicon Valley Bank and Signature Bank. In both cases, the costs not covered by the banks’ assets would be funded out of the FDIC’s Deposit Insurance Fund (DIF), which had a $125bn balance as of Q4 2022. The SRE waives the requirement that FDIC resolution uses the method that is least costly to the DIF.

Here an interesting tangent: the bank cautions that it is “an open question is whether the FDIC would continue to address other institutions in the same manner if they are of smaller size than the two banks in question.” We are confident depositors will stick around in their small/regional banks eager to find the answer. Or maybe not.

The Fed and Treasury also announced the Bank Term Funding Program (BTFP), which would provide advances of up to one year to any federally insured bank that is eligible for discount window access, in return for eligible collateral (generally Treasuries and agency securities). A key aspect of the facility is that the Fed would value collateral at par without the standard haircut the Fed applies in other programs. This will allow banks to fund potential deposit outflows without crystalizing losses on depreciated securities. The loans are made with “recourse beyond the pledged collateral to the eligible borrower” suggesting that the par valuation of the collateral would only become relevant if the borrowing institution lacks sufficient assets to repay the loan. The facility is backstopped with $25bn from the Treasury’s Exchange Stabilization Fund (ESF), which has a net balance of $38bn.

… and is thus woefully insufficient, something we discussed earlier.

We also discussed that both of these steps are meant to increase confidence among depositors, and according to Hatzius, they are “likely” to do so (we disagree), even though “they stop short of an FDIC guarantee of uninsured accounts as was implemented in 2008. The Dodd-Frank Act limits the FDIC’s authority to provide guarantees by requiring congressional passage of a joint resolution of approval, which is only marginally easier than passing a new legislation. Given the actions announced today, we do not expect near-term actions in Congress to provide guarantees.”

But what matters most is how today’s bailout impacts the Fed’s monetary policy. The answer: the hikes are over.

In light of the stress in the banking system, we no longer expect the FOMC to deliver a rate hike at its next meeting on March 22 (vs. our previous expectation of a 25bp hike).

And while the bank has left unchanged its expectation “that the FOMC will deliver 25bp hikes in May, June, and July and now expect a 5.25-5.5% terminal rate” it sees “considerable uncertainty about the path.”

Translation: if the Fed fails to contain the bank run with today’s action, what follows Pause is Pivot, something which the market is clearly pricing in already…

… as is Jeff Gundlach.

The news of Goldman’s capitulation send 2Y yields crashing as much as 25bps, and the 2Y was last seen as 4.3725, down from 5.06% on Wednesday…

… crushing countless Treasury shorts.