Fra ING:

Wind and solar energy are expected to gain cost competitiveness over fossil fuel and nuclear power in 2021. Increasingly, it is becoming cheaper to add new wind and solar capacity compared to new fossil fuel power plants or nuclear power plants

- First tipping point: gifts of nature

- Second tipping point: new-build wind and solar cheaper than new-build coal, gas and nuclear plants

- Third tipping point: new-build wind and solar cheaper than existing, gas and nuclear plants

- Renewables and power prices: a comparison between Germany and the Netherlands

- Higher shares of renewables make German power markets more volatile

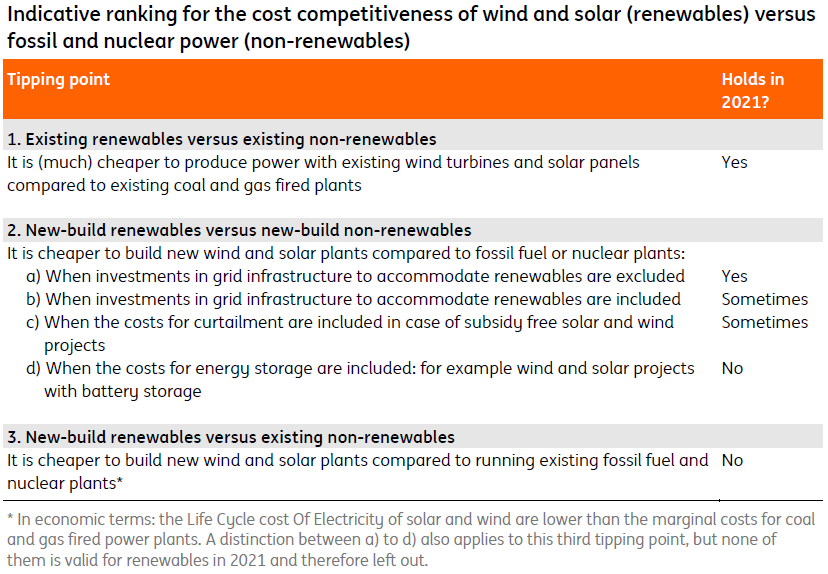

The price development of wind and solar is marked by three important tipping points (see table). First, wind and solar power have always benefited from close to zero marginal costs. Once the panels and turbines are in place they are the cheapest technology to produce an extra MWh of electricity, as wind and sun are freely available whereas fossil power plants need to pay for gas or coal. In short, existing wind and solar projects outcompete existing coal and gas power plants. Renewables drive out fossil fuel production once they enter the power mix.

Overview of renewable energy price tipping points: competition continues in 2021

Second tipping point: new-build wind and solar cheaper than new-build coal, gas and nuclear plants

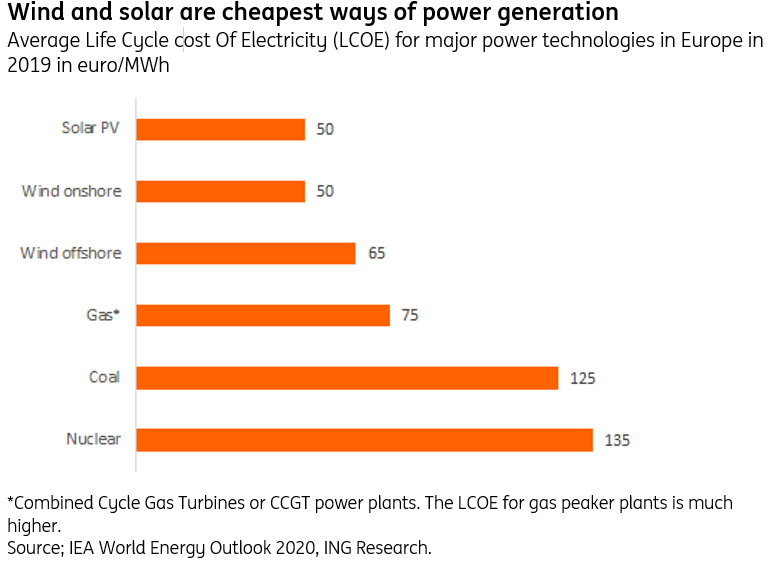

For investment decisions, one must also include the initial investment through capital costs and the maintenance costs to keep the technology running. The Life Cycle cost Of Electricity (LCOE) does just that and can be viewed as the total cost to produce a MWh of electricity during the lifespan of the asset. Nowadays, even new-build renewables are, on average, cheaper than new-build fossil fuel or nuclear power plants (see graph). We expect this gap to widen further in 2021. First, solar panels and wind turbines continue to get cheaper and experience favourable tender conditions in the current economic environment. Second, we expect upward pressure on fossil and carbon prices in 2021. Lastly, an estimated 35 GW of solar and wind capacity is expected to enter European power systems, which will lead to lower utilisation rates of fossil fuel power plants.

This tipping point of new-build wind and solar projects being cheaper compared to new-build fossil fuel power plants is likely to get more nuanced in 2021 and the years beyond. It holds in most cases if the cost for investment in the power grid are not taken into account. But power grids are increasingly showing their limitations to accommodate renewables in areas with a high supply of renewables (e.g. large wind and solar farms in rural areas) or strong growth in power demand (e.g. new data centres in urban areas).

Furthermore, this tipping point needs to factor in the production profile of renewables during the day. For example, power generation from solar and wind has a strong peak at noon, especially on sunny days. Production needs to be shut down (curtailed) in case supply exceeds demand or if prices are negative and the plant is penalised for power generation[1]. In 2021, new-build renewables could be cheaper compared to new build fossil fuel plants even if a couple of days of curtailment per year are factored in.

Curtailment could be technically avoided by adding storage facilities to solar and wind projects so that electricity can be stored during times that supply exceeds demand or when prices are too low to cover costs. However, new-build wind and solar projects combined with large scale battery storage or hydrogen electrolysis is not yet cost competitive with new-build fossil fuel plants.

[1] This is the case for subsidy free wind and solar projects where the owners run merchant risk.

Third tipping point: new-build wind and solar cheaper than existing, gas and nuclear plants

Finally, a third and even more disruptive tipping point would emerge if the costs of building new solar and wind projects are lower than running existing coal or gas fired power plants. In that case, it would be economically viable to replace fossil fuel power generation with wind and solar energy. A considerable part of fossil fuel generation is still needed though to act as a back-up facility at times when the sun and wind are not strong enough, especially in the absence of large scale storage facilities. This third tipping point does not hold in 2021 and power market structures are likely to change once markets reach this tipping point in order to guarantee the reliability of power systems at all times.

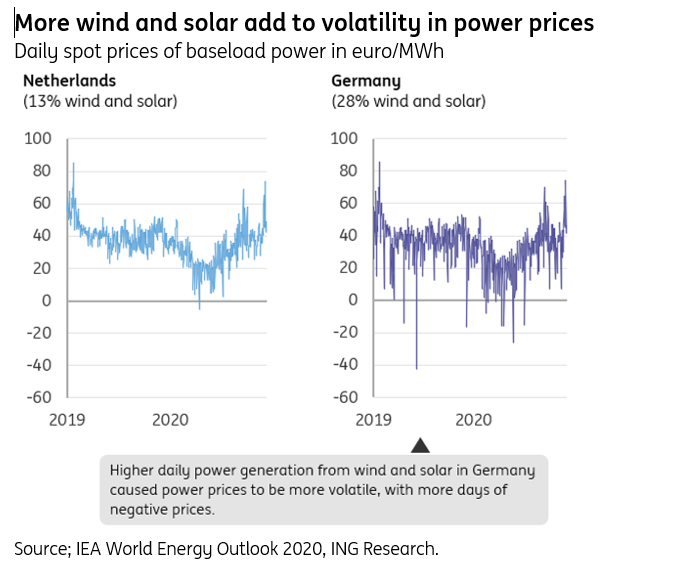

Renewables and power prices: a comparison between Germany and the Netherlands

The impact of renewables on European power prices is likely to increase. Research shows that power prices get more volatile as wind and solar leave their mark on the power mix[2]. In that respect it is interesting to compare the German and Dutch power markets. These markets are quite similar but differ in the degree of wind and solar power generation. First, the similarities. In both countries the majority of power is generated with fossil fuels. Both countries also have strong ambitions and policies to increase wind and solar generation. The vast majority of existing wind and solar capacity is subsidy-based in both countries. Producers of wind and solar power run no or little market risk and produce as much power as possible, irrespective of the power price. In Germany, however, the share of wind and solar in the power mix is twice the share of wind and solar in the Dutch power mix (28% vs 13%). That is a major difference that sets these markets apart.

[2] See for example the energy outlooks by Aurora Energy Research, DNV-GL and Bloomberg New Energy Finance.

Higher shares of renewables make German power markets more volatile

The higher share of renewables in Germany has two major implications for power prices (see graph). First, German power prices are more volatile as wind and solar push down the power price on sunny and windy days much further than in the Netherlands[3]. Second, with the lack of large storage facilities for surplus power, and with most wind and solar assets producing as much power as possible (subsidy-based renewables), the higher share of wind and solar in Germany results in more days with near zero or even negative power prices. We expect this situation to continue in 2021 for two reasons. First, more renewables will enter European power markets in 2021. Second, the vast majority of power generation from renewables will be subsidy-based in 2021 despite the early trend of subsidy-free tender bids for renewables. Therefore, owners of wind farms and solar panels have little incentive to cut back on production when prices are low or negative.

[3] In Germany, the average power price in the 2019-2020 period is €2 lower compared to the Netherlands (34 vs 36 euro/MWh). Volatility is €4 higher (standard deviation 15 vs 11 euro/MWh).