Still playing out – for now | The déjà vu setup continues to play out, with price action, positioning, and macro signals all moving in the same direction. While short-term bounces are possible given stretched conditions, the broader backdrop, from flows to volatility dynamics and macro pressures, still argues for a fragile market. |

|

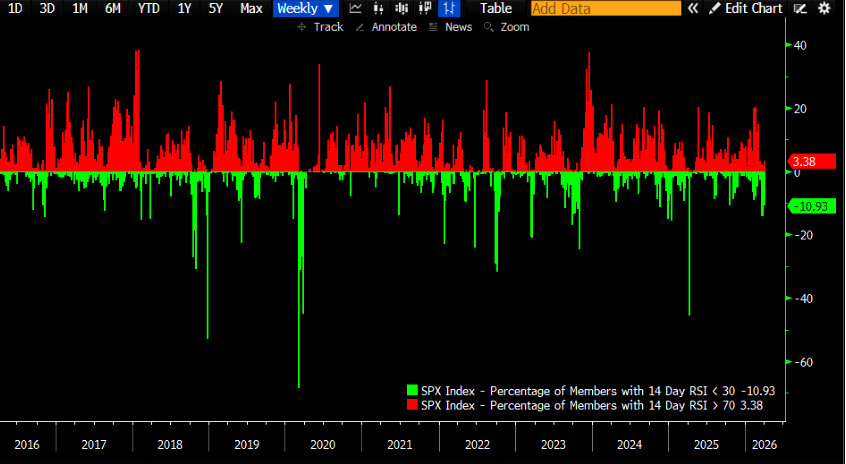

Base case stays intact | Our déjà vu framework that we’ve been outlining over the past weeks continues to play out almost perfectly. We’re now well below the 200-day, with the 21-day crossing below it, a “light” death cross. RSI is at its most oversold levels since the Liberation Day panic, so a bounce is possible. But catching falling knives isn’t a strategy we like. |  LSEG Workspace |

|

“Muted” vol | Volatility is about pace, not direction, a point often overlooked. As we noted last week, markets can move lower without volatility needing to rise much (unless we crash), if at all. |  LSEG Workspace |

|

No bueno | “The collapse in forward inflation like 5y5y is telling you something…energy shocks generally not good for growth.” (GS Privorotsky) |  LSEG Workspace |

|

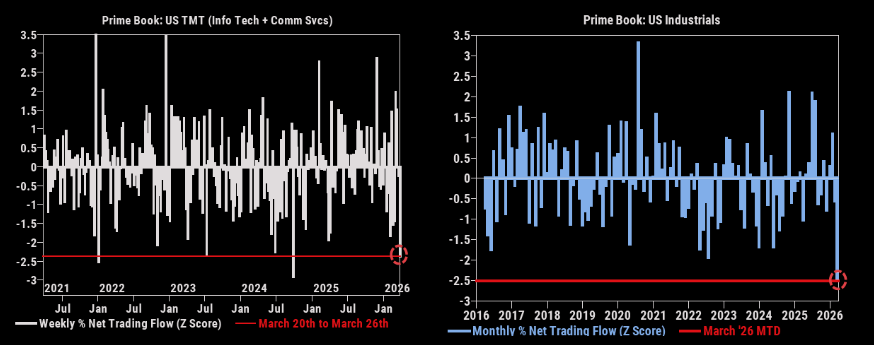

Selling superlatives | Selling has broadened. TMT has seen one of its largest net selling weeks in years, with Mag7 names sold in 12 of the past 13 sessions. Industrials have now been net sold for five straight weeks, with March tracking as the largest percentage net selling on record, writes GS. |  GS |

|

We could see more pain | Only around 11% of SPX constituents are oversold. |  Bloomberg/GS |

|

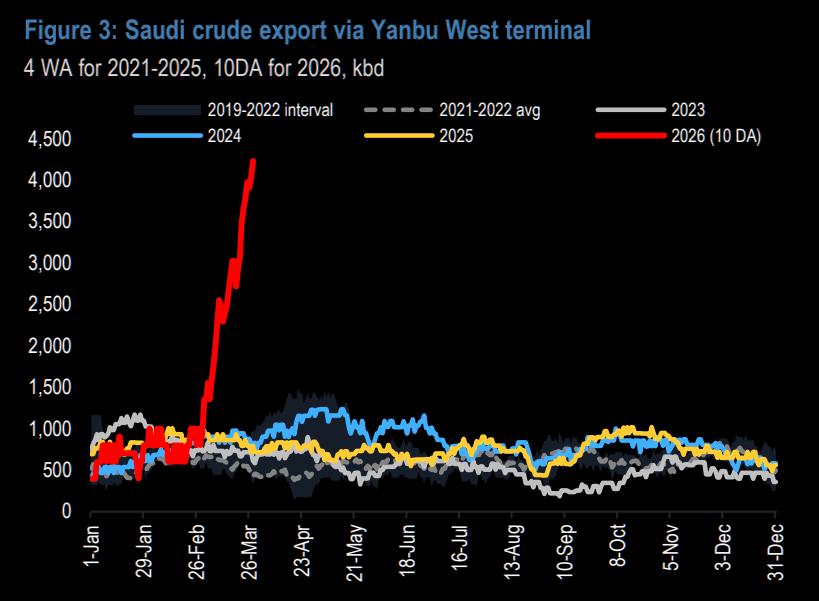

| Macro risks aren’t helping either. The Houthis’ involvement adds a second maritime pressure point in the Red Sea, with the ability to threaten Saudi Arabia’s Yanbu export hub and disrupt traffic through the Bab al-Mandeb. This puts ~5 mbd of Saudi bypass capacity at risk, potentially adding around $20/bbl to oil prices, writes JPM’s Kaneva. Workarounds exist, but longer routes could extend Asia shipping times by up to 40 days and require 130+ additional tanker voyages. Latest note on oil here. |  JPM |

|

XLE overbought superlatives | XLE’s daily RSI has only reached these levels a handful of times over the past decade, while the weekly RSI is now at its most overbought levels since 2011. Another example of stretched positioning in a fragile backdrop. |  LSEG Workspace |  LSEG Workspace |

|

EWY suckers | On Feb 27, we flagged the Korean bull as stretched, noting: “EWY weekly RSI at 90 — that’s not early, that’s crowded.”Since then, EWY is down over 20%, breaking down and printing new lows. The 21-day is about to cross below the 50-day, while the longer-term trend sits well below. |  LSEG Workspace |

|

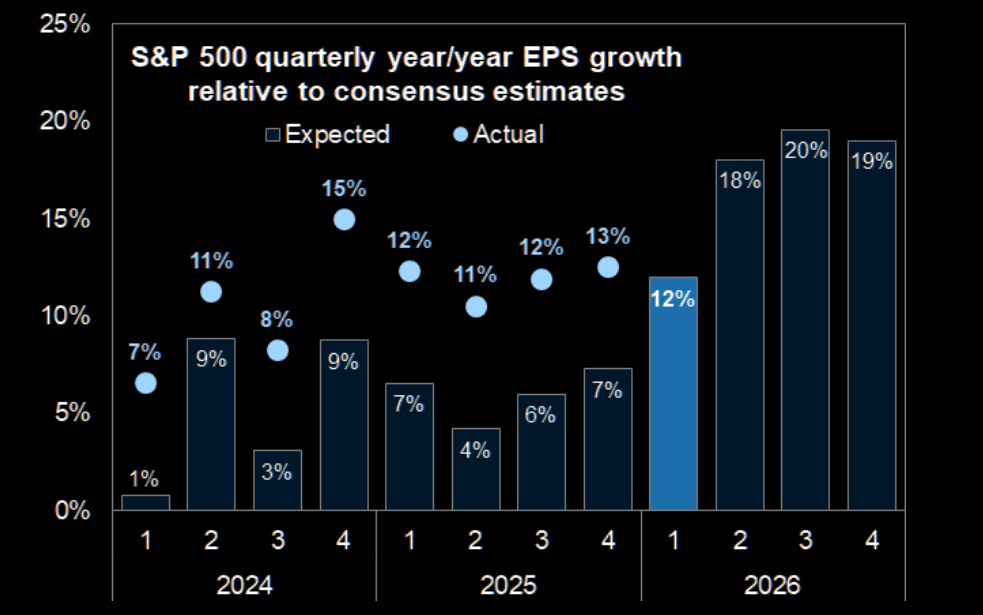

Earnings MoMo starts | Consensus expects S&P 500 EPS growth of 12% year/year in Q1 2026. |  FactSet |

|

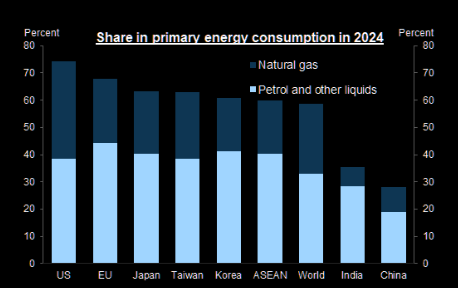

China the winner | The Chinese economy appears better positioned amid the oil supply shock than its global peers. One reason is that China’s energy and power reliance on oil and gas is much lower than its global peers. Crude oil and LNG accounting for 28% of China’s primary energy consumption in 2024, one of the lowest in the world. More on China as the relative |  EIA |

|

Everybody wants the bounce | Nothing has changed, and that’s the problem. Everyone is looking for the bounce, but the setup still points lower. |

|