Uddrag fra Authers, FT

DeepSeek matters so much because it calls into question two fundamental assumptions that have underpinned the market since the launch of ChatGPT in November 2022. First, companies wanting to compete in AI, or to use it, will have to make massive and very energy-intensive expenditures to do so. And second, Nvidia’s lead in producing the chips needed for AI was so great that it effectively had a monopoly. Companies would have to spend a lot of money, and they would have to spend it with Nvidia.

To show how important these concepts are, mark these words from Louis Navellier, a veteran and very canny growth investor. He doesn’t try to be politically correct about why he holds a large chunk of Nvidia. Back in May, he upped his price target for the company by 40% and said:

Nvidia is a monopoly and it’s going to remain a monopoly for the end of the decade. They’re not going to have competition because they spent over $2 billion to build their Blackwell chip and no one can afford to compete with them.

In November, he pressed on with the bull case as follows:

Since Nvidia spent approximately $2 billion developing the Blackwell GPU, it has no competitors and as it develops even more powerful GPU successors to Blackwell, I do not expect any competitor to “crack” Nvidia’s monopoly on generative AI. By the end of the decade, there are not expected to be any Nvidia GPU successors since the transistors in each chip will be approaching the “atomic” level, so sheer physics will prohibit Nvida from making its CPUs faster.

If this sounds like an exaggeration, look at the profit margins that Nvidia has been able to generate. They have been running at more than 50% for the past year, a rate of profitability that even tech groups once dominant in fast-growing sectors could not match. Nvidia’s current level of profitability is roughly double any margin that Apple Inc. or Cisco Systems Inc. has ever been able to produce:

Capitalism, working properly, would spur someone to come up with a technology to grab a share of those margins. That might just have happened.

AI Deepsruption |

The question remains: Is DeepSeek really such a big deal? Unlike OpenAI and other AI ventures at the forefront of US tech optimism, relatively little is known about it, but it certainly appears to undercut the dominant players. It has speeded up a rotation away from Big Tech that looked overdue. The tension between the US and China is likely to curtail advances, but others might benefit.

As Keith Lerner, chief market strategist at Truist argues, if DeepSeek’s claims are true — that it offers a robust AI tool utilizing low-level Nvidia chips, open-source code, and can be deployed at a fraction of the cost — then it could inspire hundreds of copycats, especially in the US. That’s where the damage will be felt, and it’s not necessarily a win for DeepSeek.

Also, as experts unravel DeepSeek’s capabilities, they will also get to examine the lofty tech valuations and concentration risks that have grown since ChatGPT’s introduction. An efficient and cost-effective open-source artificial intelligence model should be good news for the economy, but not necessarily for the stock market.

As Adrian Cox and Galina Pozdnyakova of Deutsche Bank AG put it, there’s a sudden realization that you don’t need a Tesla Model X to drive around the corner to pick up a pint of milk — a much cheaper Chinese BYD can do the job just as well. If this belief becomes conventional wisdom, then Nvidia will find it hard to claw back much from its half-trillion-dollar hit.

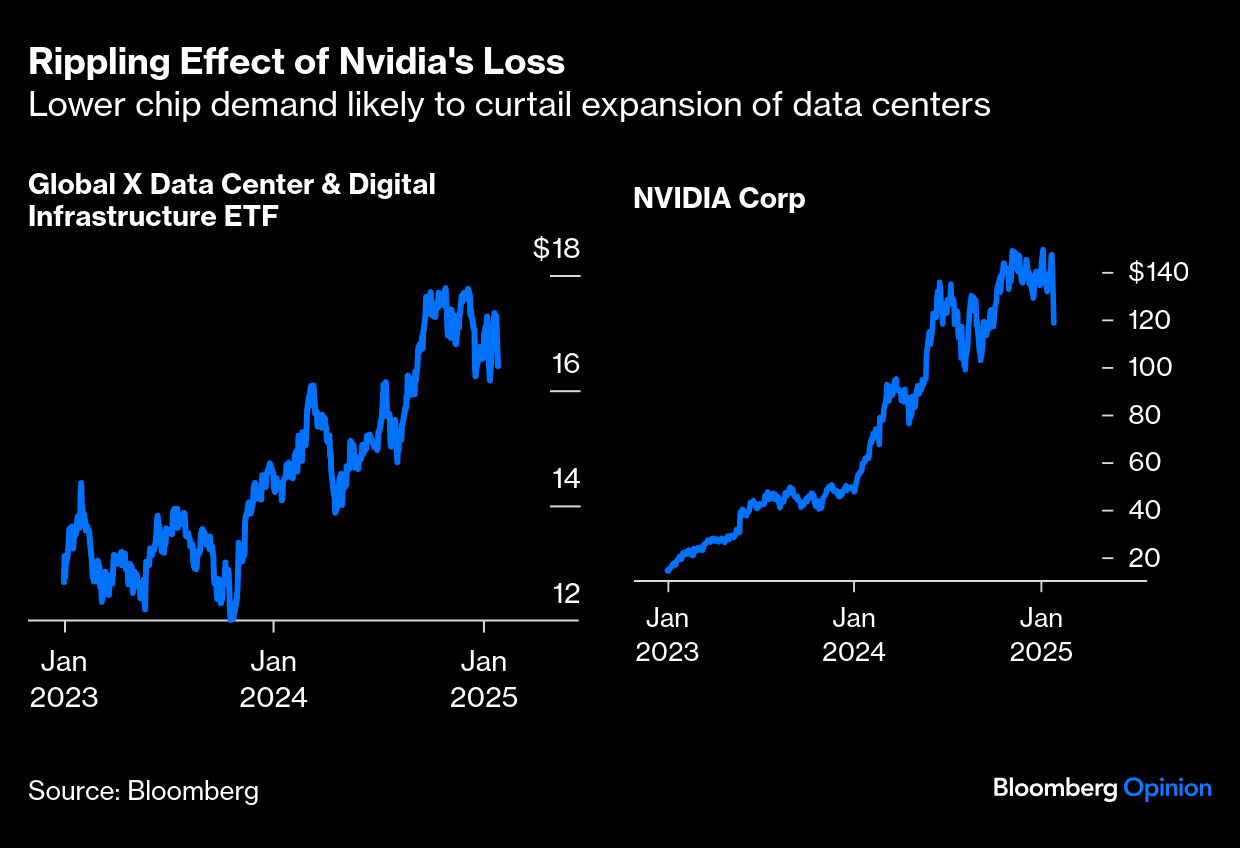

Data centers that support the supercomputers currently thought necessary to run complex AI models also stand to lose. Both Nvidia, the Global X Data Center, and Digital Infrastructure exchange-traded funds plunged by the most since 2021:

How long could the damage endure? Michael Reynolds, investment strategist at Glenmede, argues that if DeepSeek’s claims are proven, an aggregate reduction in demand for the chips would damage high expectations for both unit sales and prices:

This is kind of the moment where we turn the corner and some of these companies will begin to have to take a hit to their valuations. If it should persist and these claims prove to be true — we think investors are going to have to take a hard look at some of the premium valuations that some of these companies are garnering because embedded is an expectation that you almost have a parabolic increase in earnings into the future.

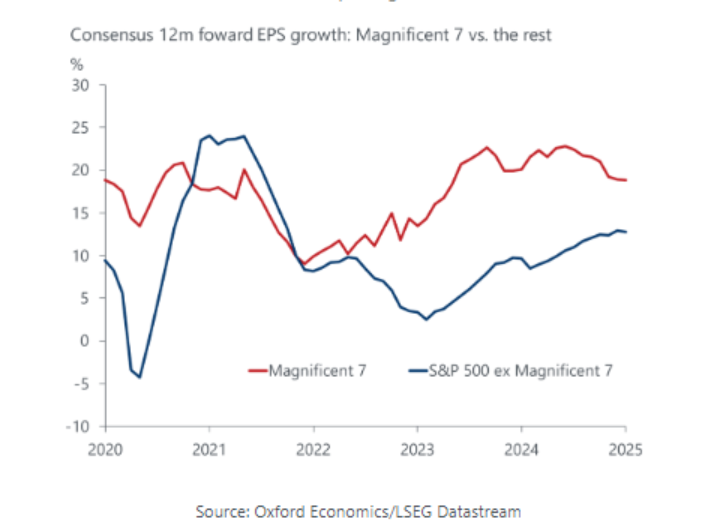

Worries about unrealistic expectations for tech have been around for a while. The question was whether there was a catalyst or mechanism to bring them down. DeepSeek might well prove to be that catalyst. Ahead of this week’s tech earnings, the Chinese firm’s introduction ups the ante. Daniel Grosvenor, equity strategist at Oxford Economics, argues that a tech correction could be a meaningful near-term headwind for the market given the high level of concentration in the US:

The Magnificent Seven are no longer the sole driver of US earnings, as there has been a clear broadening of EPS growth over the past few quarters. We think this trend will continue, underpinned by strong consumer spending and a revival in manufacturing, and expect it to support the outperformance of small-cap and equal-weighted indices.

As this Oxford Economics chart shows, the mega-companies’ earnings lead is narrowing:

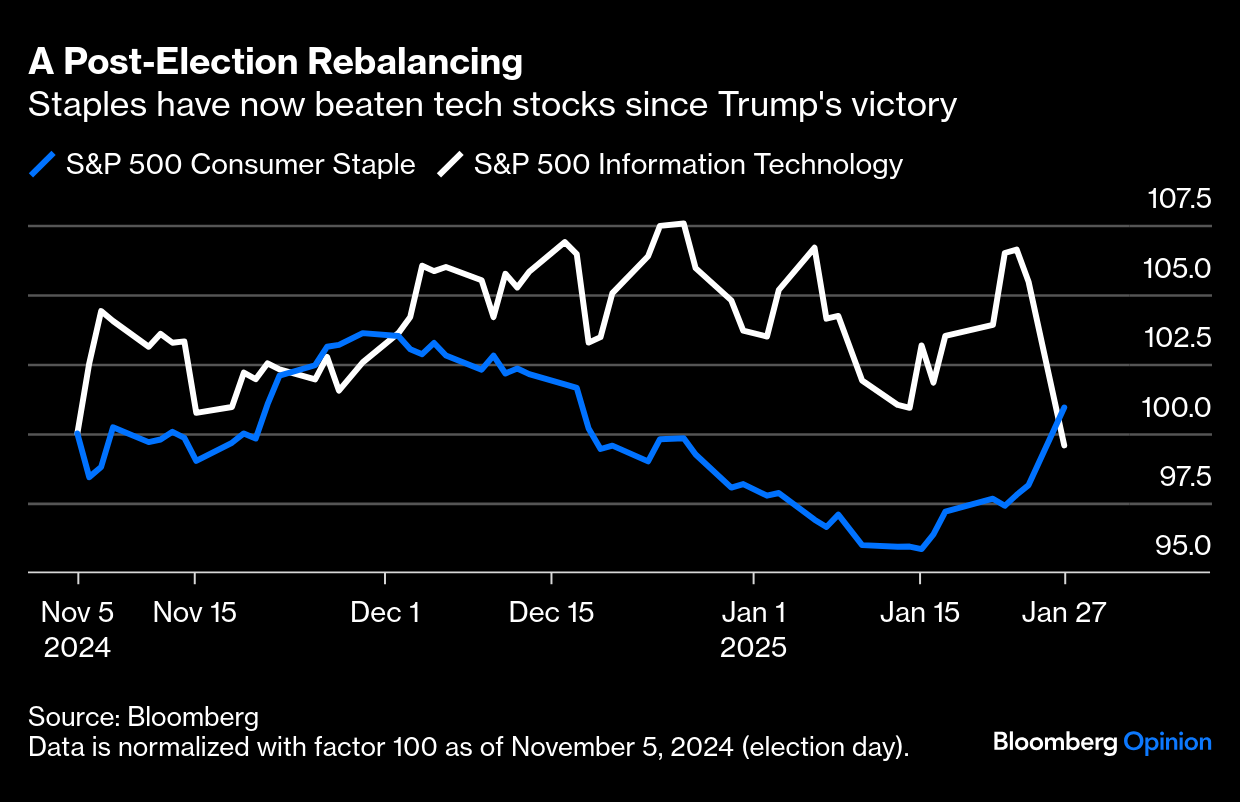

Monday’s rout has enhanced market breadth. Consumer staples stocks had a great day, and have now outperformed tech since the election: