I denne uge begynder en ny runde forhandlinger mellem Storbritannien og EU om Brexit. Forhandlingerne i juni ventes at blive barske, og et af hovedpunkterne er en fiskeriaftale, der har dansk interesse. En rådgiver for den tidligere regeringschef May mener, at en aftale må udskydes et halvt år. ING tror snarere, at der først kommer et resultat i sidste øjeblik.

Brexit returns as major headache for the pound

The fading prospect of an extension to the post-Brexit transition period, and the risk of supply chain disruption at the start of 2021, casts a cloud over the GBP outlook

The chances of a trade deal are probably higher than they currently seem

Brexit is back in the spotlight this week as the UK and EU sit down for another round of virtual talks. But there’s little to suggest we should expect any real progress, and that’s one reason why we’ve seen some risk premium creep back into the pound. So are markets right to be worried?

Well, with both sides trading accusations that the other is being unreasonable, it is tempting to conclude that the chances of a free-trade agreement (FTA) being agreed this year are fading. But it’s worth remembering that meaningful progress was always unlikely until the autumn. The last-minute pivot by the UK last October to agree on the withdrawal agreement is a good reminder that movement can come late in the day.

The message here is that we shouldn’t write off a wider free-trade agreement being struck just yet.

And amid all the hawkish language being used by both sides, there are some – admittedly pretty subtle – glimmers of optimism. Fishing, an issue that cuts deep into the Brexit debate, is going to be discussed quite a bit in this round of talks. We shouldn’t be expecting any swift progress here, but the EU is reportedly open to some movement from its ‘maximalist’ initial position on fishing.

The UK too may also be inclined to ultimately compromise on fishing. After all Britain exports most of the fish it catches, and imports most of what it eats. Failure to strike a deal could see steep tariffs placed on fish, enough to cause significant damage to the industry.

The message here is that we shouldn’t write off a wider free-trade agreement being struck just yet. It will probably boil down to whether the UK is prepared to accept at least some alignment to EU state aid rules – an issue that has been thrown into sharper focus as the UK government responds to the economic impact of coronavirus.

An extension to the transition period looks less likely

Still, we return to the point we have often made, and that is regardless of whether a free-trade agreement is signed, we should expect big changes in the way the UK trades with the EU. Even with an FTA in place, there will still be regulatory checks on goods passing across the channel, and these can be particularly intrusive for agricultural products and these agreements also typically do very little for services.

That implies some initial disruption to supply chains is inevitable, and the risk of this coinciding with a renewed Covid-19 outbreak over winter months risks putting the brakes on the economic recovery. This prospect is putting pressure on the UK government to extend the transition period – the standstill phase that’s currently set to last until the end of the year.

In the UK, at the height of the outbreak back in early April, all the signs suggested an extension may be on the cards. The polls began to suggest the public would support a delay, while a number of prominent pro-Brexit lawmakers and commentators also spoke in favour of an extension.

Whatever happens, it looks like June is going to be a turbulent month for Brexit

But the government has consistently reiterated that it won’t extend the transition beyond 2020, and while both sides have until the end of June to decide, it’s now looking pretty unlikely that it will change course. According to The Spectator, the government’s view is that it would be better to get the initial disruption out of the way during the current Covid-19 crisis, rather than letting it cloud the economic recovery.

All of this is of course very uncertain, and we’d suggest the risk to an abrupt end to the transition could instead amplify the economic disruption from coronavirus. So while it currently looks unlikely, we can’t completely rule out a fudge being agreed in June to buy more time.

One idea being floated by a former advisor to Theresa May is to extend the transition by say six months but to use this extra time purely for implementation of whatever is agreed by October. In other words, if no deal can be agreed by October, negotiations would effectively stop, but businesses would have a little longer to prepare for forthcoming changes.

GBP markets becoming less complacent, but there’s more stress ahead

Whatever happens, it looks like June is going to be a turbulent month for Brexit, and markets are beginning to brace themselves for no extension to the transition period, as well as the possibility that neither side can agree on a trade deal this year.

In our last publication, we noted GBP looked too complacent about these risks. Since then, we’ve seen a fair degree of risk premium being built into sterling, though this is more noticeable in the GBP spot than in the volatility market.

Even so, there is still further scope for stress to be built into GBP, suggesting further downside for the currency. That’s in line with our end-June forecast for EUR/GBP of 0.91, and we see three reasons for further caution:

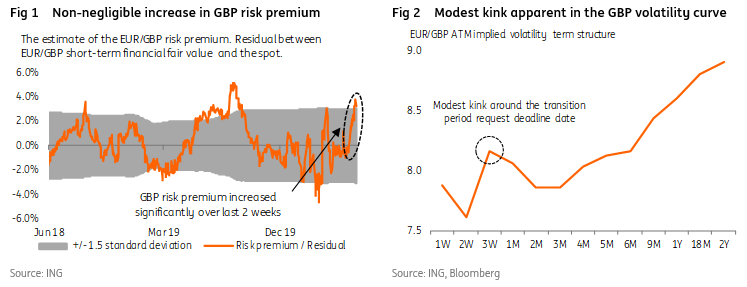

- As Figure 1 below shows, the sterling spot risk premium measure has increased (gauged by our short-term financial fair value model). Our estimate of risk premia has gone from zero to around 3%. While that’s clearly non-negligible, this is still below the highs seen back in August 2019, when our estimate of GBP risk premia reached around 5%. If UK-EU talks break down, the transition period isn’t extended, and fears about ‘no trade-deal’ return, we expect GBP risk premium to rise further (to, or above, 5%) and GBP to decline, in line with our bearish forecast.

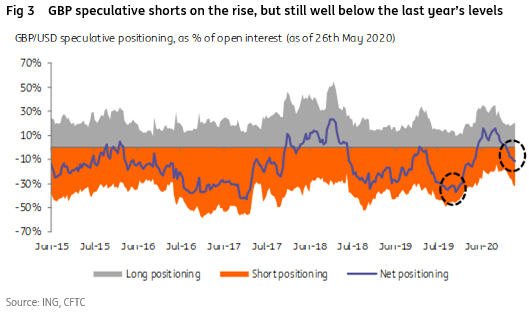

- Figure 2 shows that the GBP option market has also adjusted to the possibility of heightened UK-EU tensions, with the EUR/GBP implied volatility term structure now showing a modest kink at the end of June, which is the deadline for the transition period to be extended. But again these levels still don’t look that elevated when compared to what we observed last year. This, in turn, suggests room for further GBP downside and a spike in GBP volatility.

3. As for GBP speculative positioning, we have observed a gradual rise in GBP/USD shorts over the past few weeks. However, the level of speculative shorts still remains meaningfully below its last year highs (Figure 3), again suggesting further room for GBP weakness.

Download article as PDF