ING har analyseret virkningen i Storbritannien af Brexit. Transporten af varer mellem UK og EU er faldet kraftigt, og fragtskibes anløb i UK er lavere end normalt. Praksis viser, at det er besværligt for erhvervslivet at håndtere de nye regler om f.eks. moms. Mange virksomheder har reelt ikke været forberedt på de nye vilkår. Produktionen er faldet, men det er uklart, hvad den langsigtede virkning bliver, især for serviceindustrien og beskæftigelsen, og det bliver afgørende, om der kommer handelskonflikter med EU. Det er slående, at de britiske investeringer ligger langt efter investeringerne i EU og USA. Alt i alt: Brexit har ikke givet et boost til UK.

Brexit and the impact of new trade ties on the UK outlook

Trade disruption will deliver a sizable hit to UK manufacturing output this quarter, while lingering uncertainty and potential instability surrounding the UK-EU trade deal will keep a lid on investment. We expect consumers to lead a sharp GDP rebound this year, but higher costs and disruption will likely prevent a full recovery before late-2022

Despite the deal, there’s been plenty of disruption

The dust has begun to settle on the new UK-EU trade deal, where initial pre-Christmas relief has quickly given way to widespread reports of disruption. The deal achieved tariff-free trade, but the UK’s exit from the single market and customs union has heralded large – and abrupt – changes to the way the UK trades with Europe.

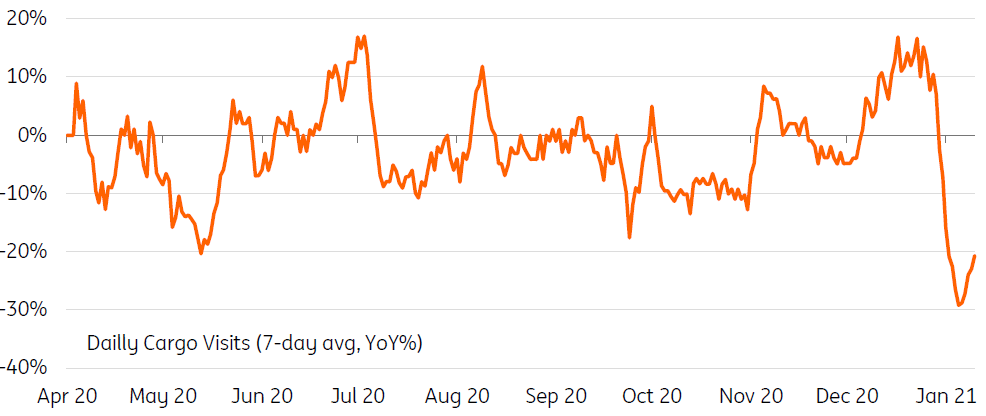

So what’s been happening? Well firstly, it’s pretty clear that trade between the EU and UK has slowed noticeably since the start of the year. New ONS data shows fewer visits by ships to UK ports, while there have also been fewer lorries crossing the Channel.

Visits by cargo ships to the UK are lower than usual

Measured as total visits to port across UK

Rules of origin and VAT changes are creating a headache

Partly this is because firms stockpiled during 2020, opting to ‘wait-and-see’ what happens in the first few weeks of January (and therefore traffic will inevitably build again over coming days). But increasingly it is also because many firms are struggling to adapt to the new trade barriers, which are many and varied, but ‘rules of origin’ is arguably one of the biggest. These barriers dictate whether a good qualifies for tariff-free entry and can be a bit of a minefield, particularly for those businesses who’ve only ever traded with the EU.

Fewer transport options have amplified the hit from new customs processes

But the situation has been amplified by transport issues – and the lack of lorry queues shouldn’t be mistaken for a lack of disruption.

Some hauliers have been reluctant to carry multiple firms’ loads together in one shipment – particularly for food – given the added challenges it poses for collating paperwork and clearing customs. A handful of major logistics firms have also paused deliveries to/from the UK given a high number of consignments reportedly not meeting new requirements.

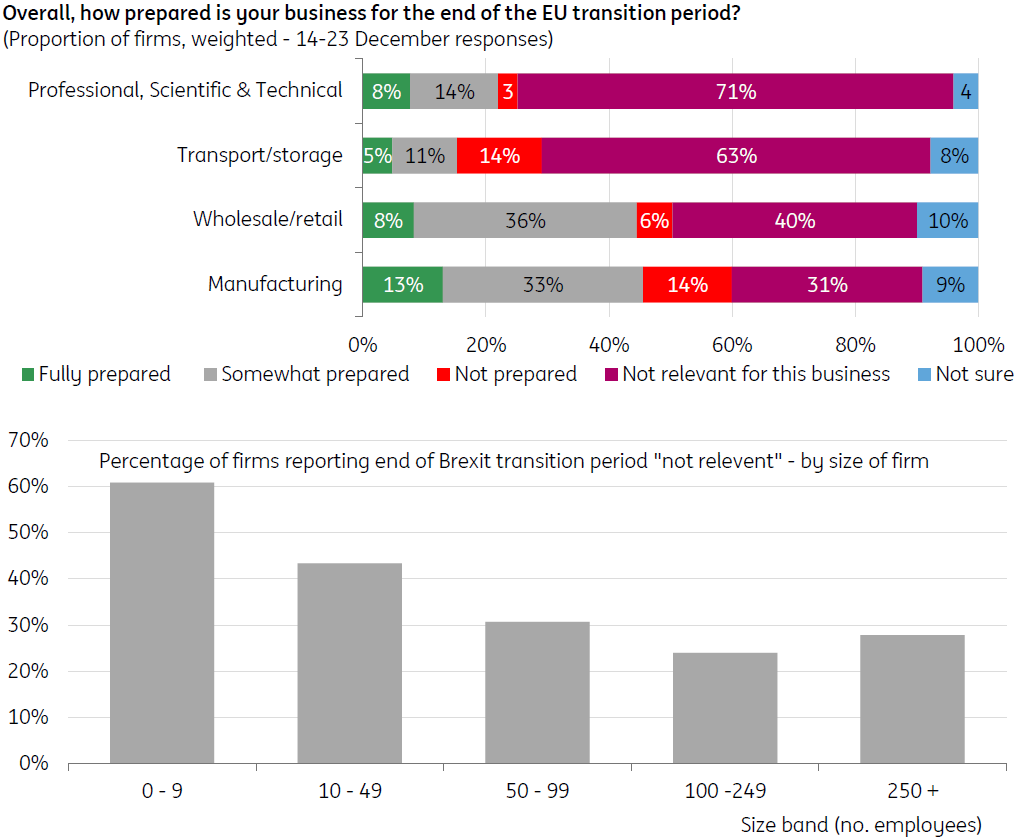

How prepared were firms for these new changes?

![ONS Business Impact of Coronavirus survey Data taken from survey wave 20]() ONS Business Impact of Coronavirus survey

ONS Business Impact of Coronavirus survey

Manufacturing production has likely fallen

The ONS Business Impact survey from mid-December indicated that half of manufacturers were only somewhat prepared, or not at all. And across the economy, a high proportion of firms reported the changes weren’t relevant to their business – which in some cases may have been because they weren’t fully aware of the forthcoming changes. The chart above showed this tended to be more common among smaller businesses.

One thing that looks inevitable is a fall in manufacturing production in January – perhaps in the region of 3-4%, and things may become worse in the short-term

That said, it’s a mistake to assume this is only hitting smaller firms. While in general larger firms are likely to have been better prepared, many rely on SMEs as part of their supply chain. That was demonstrated in December when some of the major carmakers had to pause production amid a lack of supplies coming across the Channel.

One thing that looks inevitable is a fall in manufacturing production in January – perhaps in the region of 3-4%. That’s partly because the situation is unlikely to resolve itself quickly – and in fact may become worse in the short-term as border traffic builds up once again. Net trade is also likely to weigh on GDP through this year, assuming imports recover as lockdowns are unwound but exports take much longer to recover.

Of course it goes without saying that the Covid-19 crisis will dominate the GDP figures for the next few months. But assuming the economy starts to get back on its feet through the middle of 2021, the more interesting question is how Brexit will affect the recovery – and here are three factors to bear in mind.

1New frictions likely to add further pressure to unemployment

Firstly, the new costs of customs declarations and transportation are here to stay – and this, combined with the higher administrative burden for European buyers, will inevitably reduce the competitiveness of UK exports. Unsurprisingly that’s also likely to mean some British, Europe-facing firms will ultimately no longer be profitable, and some will be forced to move more parts of their operation overseas.

While impossible to quantify, this will put additional pressure on unemployment – which is likely to rise close to 7% through 2020 assuming wage subsidies are gradually removed.

2The impact on services is arguably more complicated than goods

Secondly, given Covid-19 travel curbs, the impact on services is only likely to become fully visible after the pandemic.

This is where the UK’s competitive advantage lies, and it is also where arguably life outside the single market is more complex. For goods trade, shipments need to meet a series of hurdles to cross the border, but after that they are more-or-less free to be sold anywhere in the EU. For services, the barriers generally take the form of regulation, and this can vary significantly between member states.

3Long-term relationship will be mired by uncertainty and possible instability

Finally, the big question is what happens to the UK-EU relationship in the long term.

Will the UK seek closer economic ties with time – for instance, rejoining a customs union? For now this is difficult to see. The deal includes a review clause in 2024, and that almost certainly means the issue of EU trade will play a role in the election that year.

Perhaps the real question we should be asking is whether the UK-EU deal will stand the test of time

Instead, perhaps the real question we should be asking is whether the UK-EU deal will stand the test of time. In part, this depends on how the UK decides to shape policy surrounding ‘level playing field’, the issue that monopolised much of the negotiating time last year. Under the terms of the deal, the UK has committed not to lower worker or environment standards, and accepted state aid controls.

Trade disruption will be a drag on the recovery process

For the economy, this means a degree of uncertainty and potential instability will be a feature of the UK’s European trading relationship.

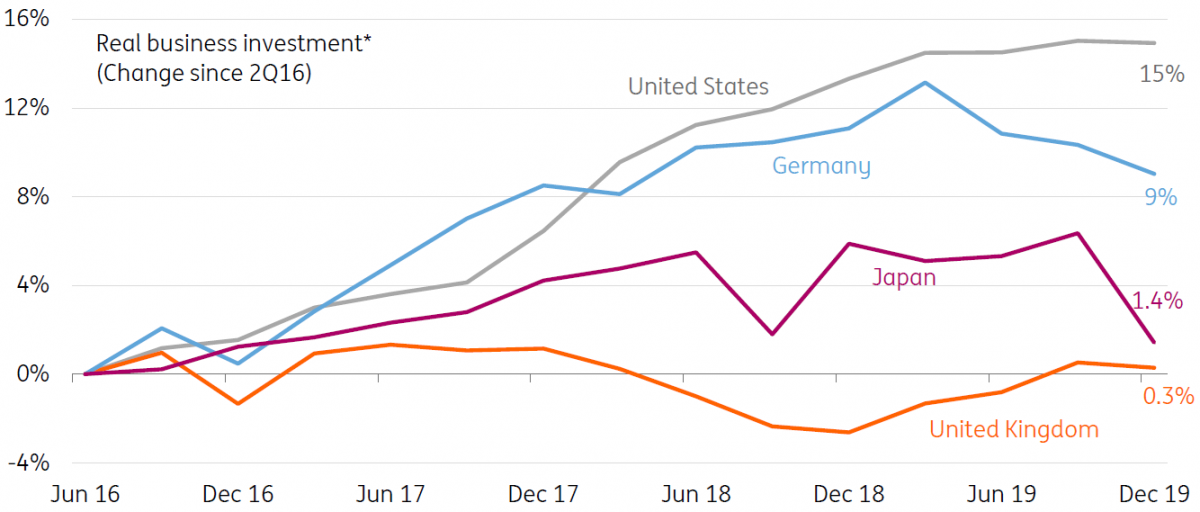

Even before Covid-19 struck, investment had underperformed G7 peers, and this is likely to continue in the post-Covid-19 recovery phase. Businesses will be wary about possible future changes to the relationship that may require further tweaks to their operating model.

While we expect consumers to lead a rebound in GDP through the remainder of 2021 (assuming the vaccine programme goes as hoped), investment is likely to lag behind – and correspondingly drag on hiring. This will likely prevent the UK economy returning to its pre-virus size until late 2022 at the earliest.

UK investment underperformed peers after referendum and before Covid-19

Definitions vary: Business investment for UK, private non-residential investment for US/Japan, private investment in machinery and equipment for Germany