Uddrag fra finanshuse:

Some disconnects

Here is a collection of cross-asset macro charts that matters now. Markets have mostly priced a rates shock, not recession risk, drawdowns remain limited, and earnings expectations continue higher. Some other charts are telling slightly different stories.

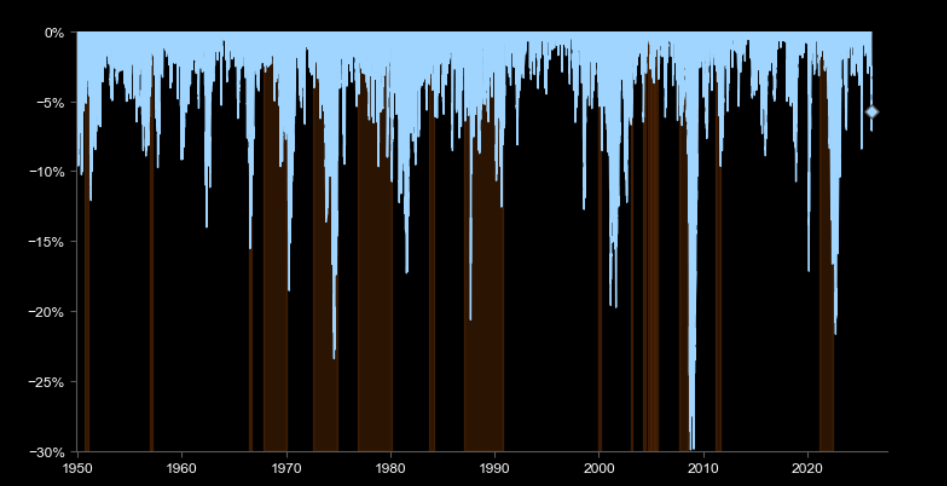

Still small drawdown

So far, the drawdown for the World Portfolio of global equities and global bonds has been limited, especially compared to previous stagflationary shocks.

Source: Haver

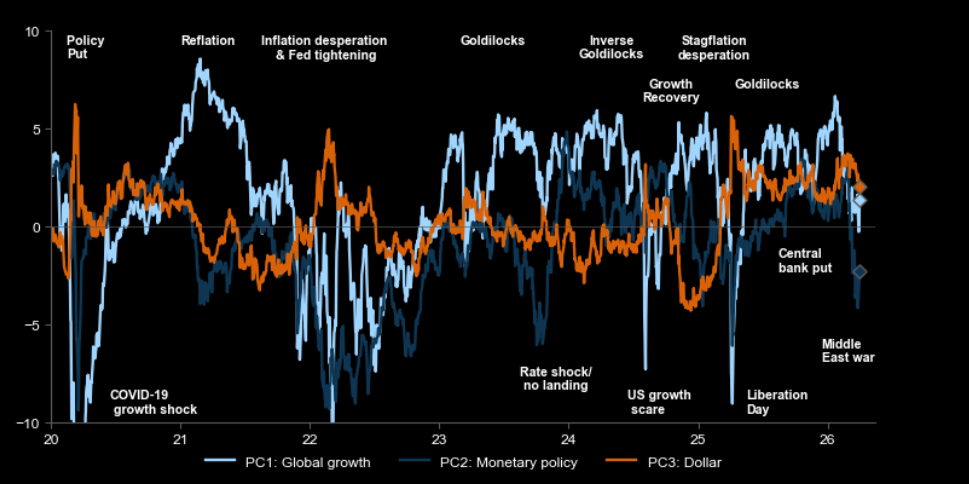

Mainly rates shock

Markets have mostly priced a rate shock but limited growth risks.

Source: Goldman

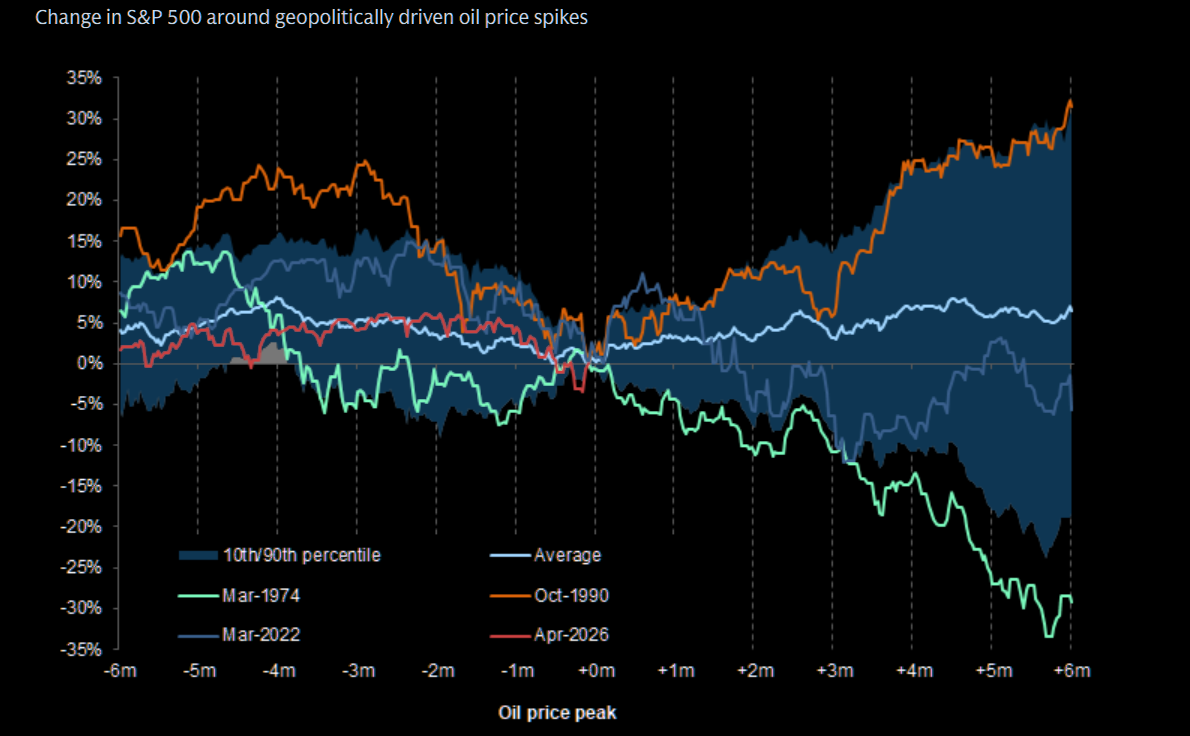

The ghost of 1974

Most historical oil spikes linked to geopolitical shocks had a temporary impact, but some weighed on equities and bonds for longer. Like 1974 -35% and >6 months.

Source: Datastream

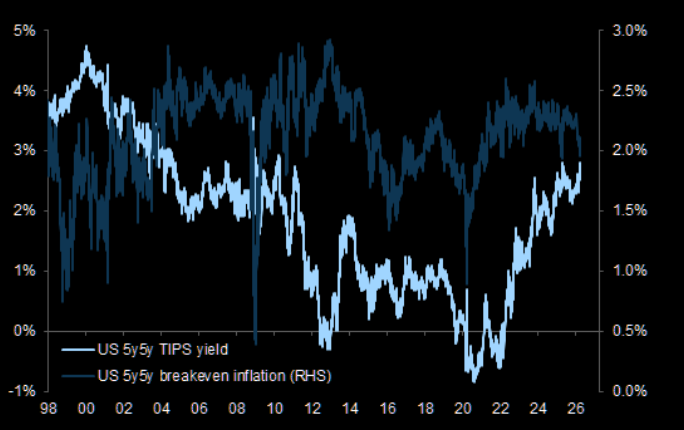

Longer-dated US inflation expectations have declined

Much in contrast to 2022, longer-dated inflation expectations (5y5y breakeven inflation) declined, with 5y5y real yields increasing. This upward pressure in yields helps explain a large part of the equity drawdown – as it has been driven by a supply-side shock without better growth, the impact on both equities and bonds has been negative.

Source: GS FICC

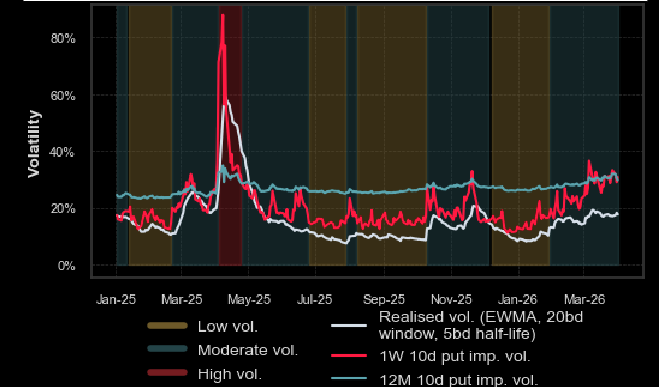

Realised and long-dated S&P 500 vols subdued

Realised and long-dated S&P 500 vols have been relatively subdued, while short-dated left tail vol has risen materially.

Source: Soc Gen Cross Asset

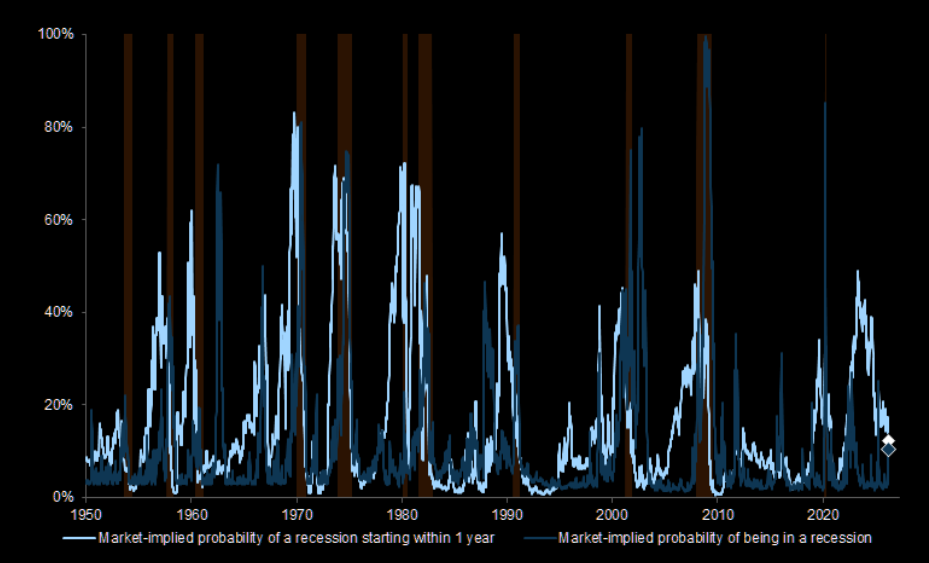

Not pricing recession

Market pricing of recession risk remains very benign.

Source: Haver

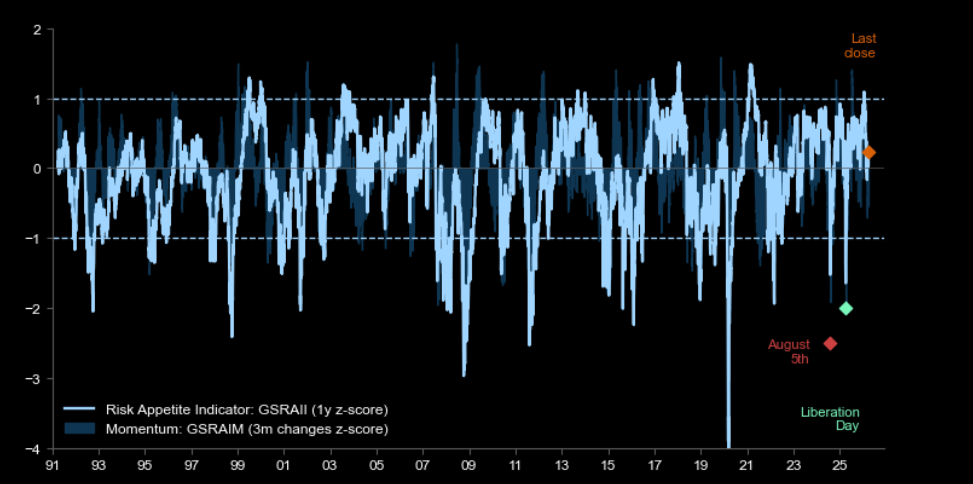

Not yet bearish level

GS: “After the bullish start to the year, our Risk Appetite Indicator declined but is not at bearish levels yet.”

Source: GOAL

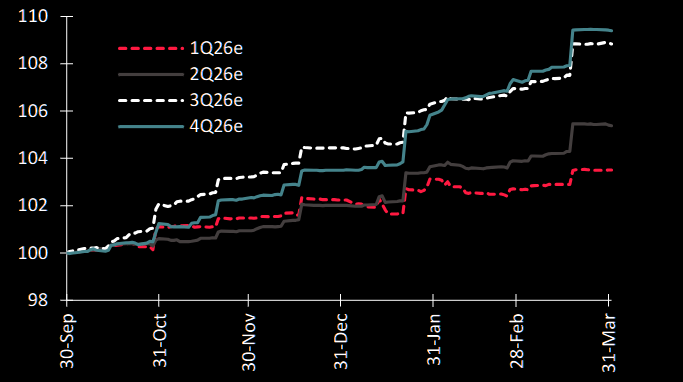

Profit expectations are still going up

S&P 500 ex oil quarterly profit expectations (indexed).

Source: Soc Gen Cross Asset

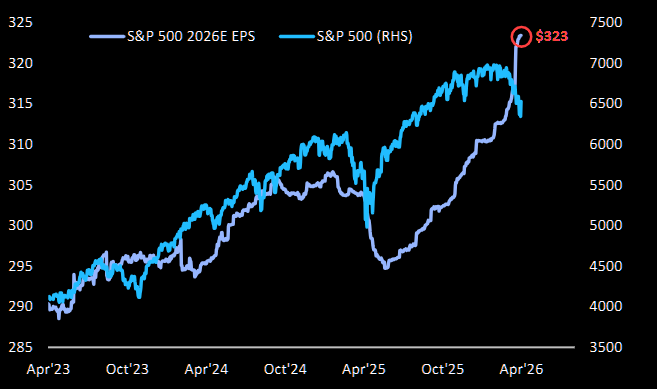

Higher

SPX ’26 EPS revised higher by 4% since Jan 1st.

Source: BofA Flow Show

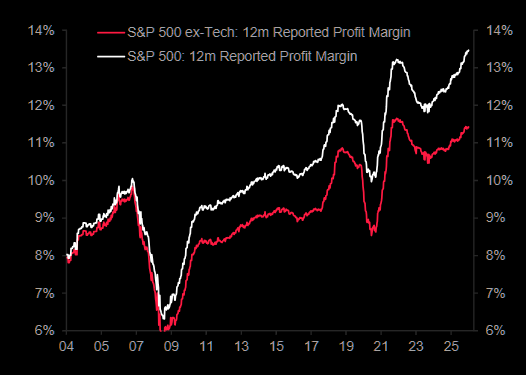

Margins improving

Margins improving outside tech too.

Source: Soc Gen

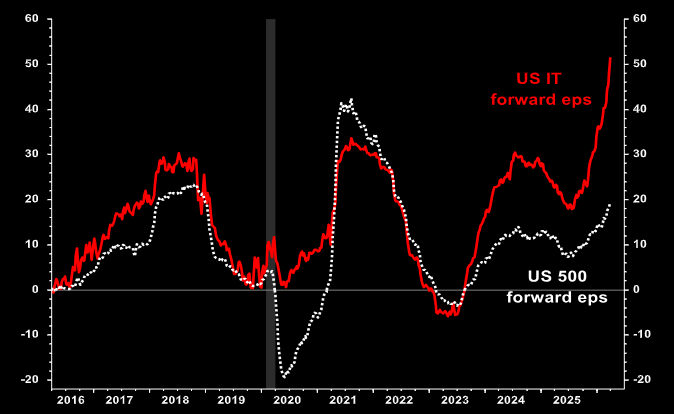

Parabolic

If we zoom out a little, there is no question that US forward earnings growth in IT has been parabolic. Chart from Albert Edwards show YoY change.

Source: Albert Edwards

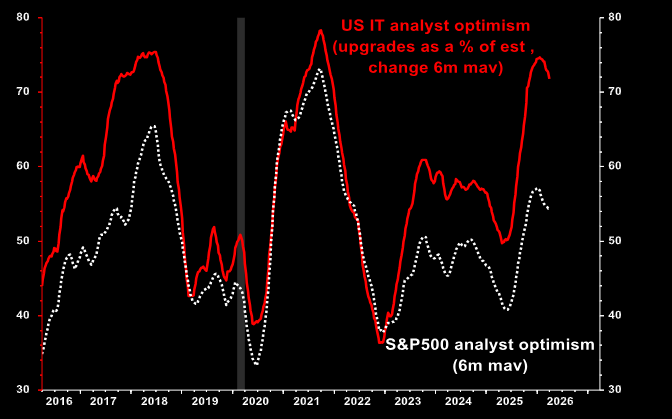

Inflection?

The pace of upgrading has turned downwards.

Source: Albert Edwards

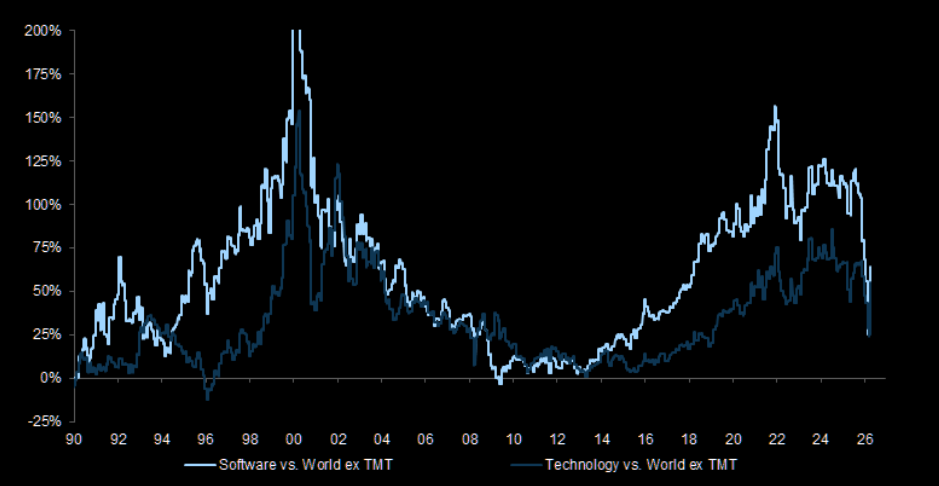

Tech de-rating

Fears of AI disruption have led to a very sharp de-rating of software and tech stocks more broadly. Not much PE premium left to erode.

Source: Datastream

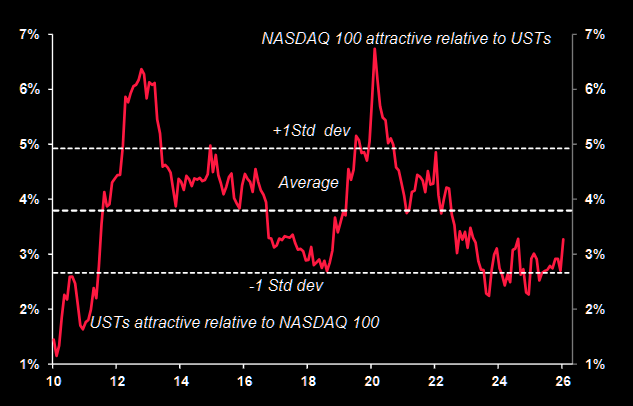

No bubble levels

Equity risk premium on Nasdaq is NOT at bubble levels.

Source: Soc Gen

Leveraged loans

Leveraged loan spreads have widened more compared to corporate credit.

Source: Haver

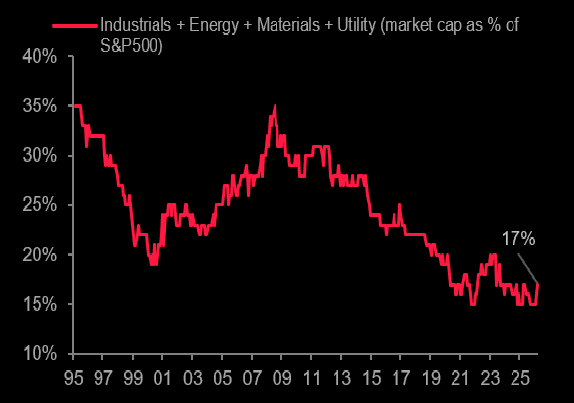

A cycle low

Physical economy market cap weight of S&P 500 is at a cycle low.

Source: Soc Gen cross asset

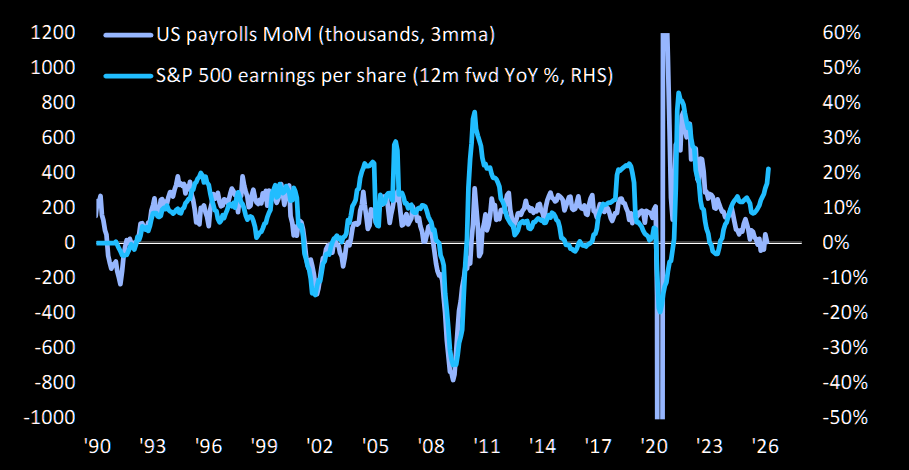

Payrolls & Profits

US payrolls MoM vs. S&P 500 12m fwd EPS YoY %.

Source: BofA

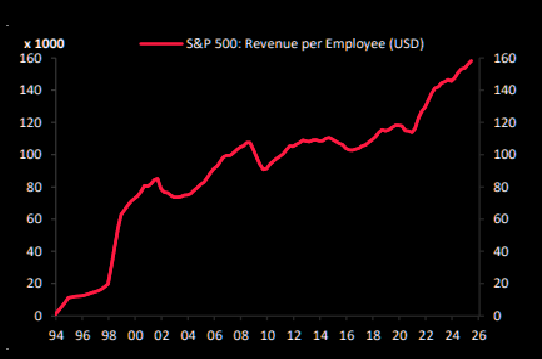

Revenue per employee

S&P 500: revenue per employee is up 40% over past 4 years.

Source: Soc Gen