Uddrag fra Bloomberg, UBS og Zerohedge

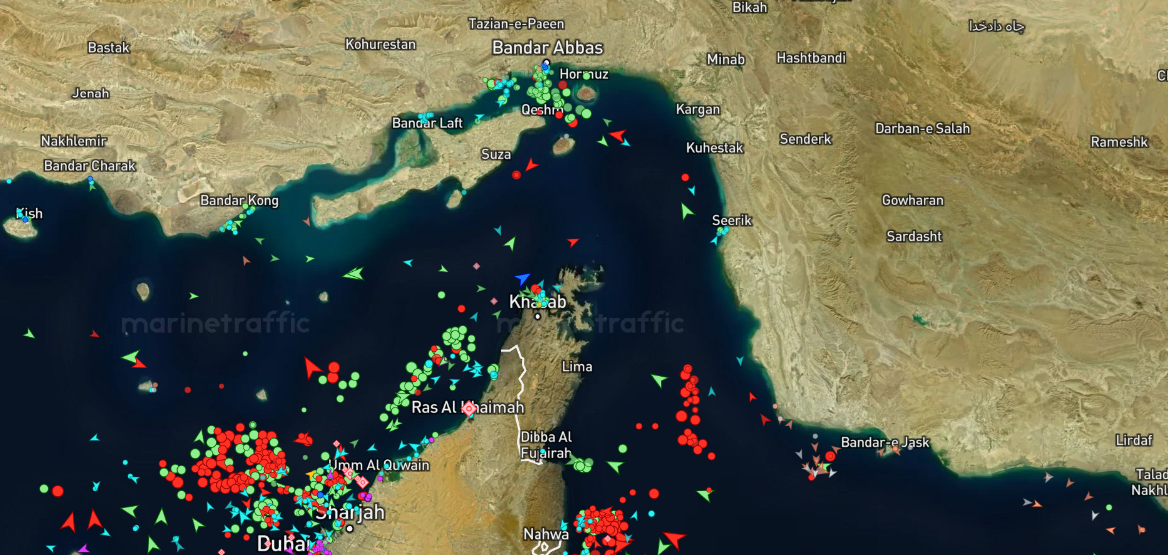

The U.S.-Iran interim peace deal has been signed, and the normalization of the Strait of Hormuz is now beginning. Tanker traffic through the critical waterway is slowly resuming, though a full return to pre-war or near-pre-war energy flows could take months.

But behind the urgency to get the memorandum of understanding deal across the finish line were two uncomfortable realities.

First, President Trump recently met with oil and gas executives, who likely informed the administration that the conflict and the shuttered Hormuz maritime chokepoint were leading to an energy cliff that would materialize by mid-summer.

On Wednesday at the G7 Summit in France, Trump acknowledged the uncomfortable truth that SPRs used to offset lost Gulf energy production were being drained at an alarming rate.

“We run out of reserves in about four weeks,” Trump told reporters.

The latest Department of Energy data showed Cushing, Oklahoma, stockpiles declined for the eighth straight week, taking inventories to just above 20 million barrels. That’s the lowest inventories have been at the storage hub since October 2014, and takes us to what are considered essentially ‘tank-bottoms’, the point at which the hub is unable to fully operate.

Second, the physical disruption in global supply chains had begun spreading beyond energy flows and into shipping costs, threatening to transmit the Hormuz crisis into broader goods inflation.

Last month, UBS analyst Pierre Lafourcade warned, “Supply chain stress is rising at its fastest pace since the early pandemic.” This prompted Lafourcade to re-launch the Global Supply Chain Stress Index.

Earlier this morning, Lafourcade warned in a new note that “supply chain stress spreads to shipping cost” and that “continues to rise.”

He continued:

Our Global Supply Chain Stress Index has continued to deteriorate, despite the recent decline in energy prices. In our update mid-May (here), we noted that the index had worsened by roughly 1.2 standard deviations since the onset of the Middle East conflict. Figure 1 below shows the latest June reading, based on weekly data up to last Friday (with missing observations proxied by the prior month’s values). The median of the 23 component series (blue line) now stands at 2.9 standard deviations—an increase of around 2½ standard deviations since the conflict began—and marks the highest level since May 2022. This reading predates the geopolitical developments of the past few days and so may well end up being a high watermark. But we suspect a sustained improvement across many indicators will likely require a tangible normalization in the flow of global energy shipments, not just a decline in prices driven by expectations of resolution alone.

Our Global Supply Chain Stress Index has After a slow reaction to the conflict, shipping costs are now accelerating The indicator is constructed as the cross‑sectional average of z-scored series—a first-order approximation to the data’s first principal component. Figure 2 overleaf shows the contributions over the past four months. The indicator most directly capturing the supply-shock nature of the Hormuz bottleneck is our measure of seaborne oil and gas flows (shown on the right of the figure, with the sign flipped to indicate rising stress). All other components reflect the shock more indirectly. Oil and gas shipping volumes have dropped even more from the immediate post-closure lows, while the volume of other cargo shipping has bounced back somewhat from earlier lows (see here for our latest read on global tracking). Delivery times and air-freight costs deteriorated primarily in March and April, with little additional movement since. Initially, supply chain stress appeared relatively contained and concentrated in these indicators. However, shipping costs now seem to be responding with a lag: after little change in March and April, prices have ramped up noticeably in May and June to date, across all major reporters (Baltic, Harper Petersen, Drewry, and Freightos).ntinued to deteriorate, despite the recent decline in energy prices. In our update mid-May (here), we noted that the index had worsened by roughly 1.2 standard deviations since the onset of the Middle East conflict. Figure 1 below shows the latest June reading, based on weekly data up to last Friday (with missing observations proxied by the prior month’s values). The median of the 23 component series (blue line) now stands at 2.9 standard deviations—an increase of around 2½ standard deviations since the conflict began—and marks the highest level since May 2022.

This reading predates the geopolitical developments of the past few days and so may well end up being a high watermark. But we suspect a sustained improvement across many indicators will likely require a tangible normalization in the flow of global energy shipments, not just a decline in prices driven by expectations of resolution alone.

If SPRs are drained and supply chain stress keeps rising, the global economy moves from a manageable disruption to a stagflationary shock. That would send energy prices higher, create weaker fuel demand, lead to margin compression for companies, and eventually risk a recession.

The sequence of disasters that could’ve unfolded:

1. Energy prices reprice violently higher

2. Shipping costs feed into goods inflation

3. Corporate margins get squeezed

4. Consumers get hit

5. Central banks face the stagflation trap

6. Emerging markets falter

7. Global equities shift into recession pricing

These two pressures help explain why the Trump administration moved urgently to secure an MoU with Iran to reopen the Strait of Hormuz. The immediate goal was to normalize tanker flows and avert an energy cliff as SPR buffers came under pressure. The second objective is to stop the Hormuz disruption from spilling deeper into global supply chains, where rising shipping costs, longer transit times, and tighter effective vessel capacity were beginning to transmit the shock beyond energy markets and into the broader global economy.