Fra Zerohedge:

It’s not just The Fed’s short-term liquidity pipes that are clogged up, there appears to be some issues in the loan market, signaled by sharp declines in the $680 billion market for collateralized loan obligations (CLO), which could be an early warning sign that the junk bond market is headed for trouble.

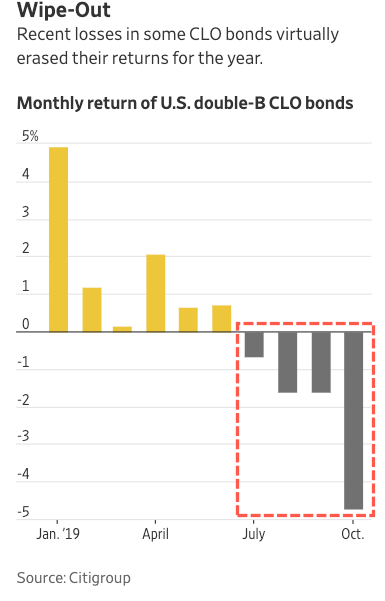

As President Trump pumps fake trade news, causing the ‘Mother Of All Short Squeezes’ in equity indexes to new highs, the CLO market in October fell 5%.

Source: Bloomberg

The rare decline in the CLO market was a result of the increasing uncertainties surrounding an economic slowdown.

S&P Global Market Intelligence data shows the CLO market has grown by $350 billion in the last three years, now stands at $680 billion, yield chasing investors mostly fueled the increase.

“We think there’s more volatility coming,” said Maggie Wang, head of US CLO strategy at Citigroup, who spoke The Wall Street Journal.

“We recommend investors reduce risk and stay with cleaner portfolios and better managers.”

This late in the cycle, a plunge in CLO bond prices with equities in parabolic up moves indicates something is wrong.

The CLO tranches that are experiencing the most stress are in the double-B tranche. These risky CLO securities netted investors 10% through June. But through the end of October, most of the gains were wiped out.

“If you think that double-B CLOs are giving a warning sign, that says something about high yield,” said David Preston, head of CLO research at Wells Fargo & Co. “It’s hard to see how both markets can be right.”

Data from Palmer Square Capital Management shows Double-B CLO bond yields are about five percentage points higher than the yield of comparably rated junk bonds.

“The yield differential hasn’t been this wide since early 2016, when dropping oil prices sparked a selloff in both leveraged loans and high-yield bonds,” The Journal noted.

Between the chaos in the repo markets, now tamped down by the promise of endless liquidity from NYFRB, and the ongoing scare in the critical-for-junk-demand CLO market, some fear the end of the year could bring a notably negative surprise.

None other than Credit Suisse’s Zoltan Pozsar (the main in charge of market intelligence for securitized credit markets for The Fed in 2008) has a warning…

“There is a very real chance that, if we don’t have a better set of pipes from the Fed and a more aggressive QE, then you have a very, very problematic year-end turn.”

But for now, record-high stocks and trade-deal optimism are all that matters, right?