Fra Zerohedge/ Goldman:

Having already goalseeked a narrative how a Democratic sweep would be great news for markets (which, as we reported yesterday, consists of as much as $7 trillion in fiscal stimulus offsetting the net income losses from Biden’s proposed corporate tax rate hike from 21% to 28%), Goldman is now moving on to the really important stuff: how much the holy crusade against climate change under the Biden administration will cost.

Now that it is conventional wisdom on Wall Street that Biden will defeat Trump (similarly to how it was a virtual certainty that Hillary would defeat Trump in 2016), big bank strategists are moving on to the key policies of a Biden presidency, where few are more important (or expensive) than Biden’s targets to tackle climate change.

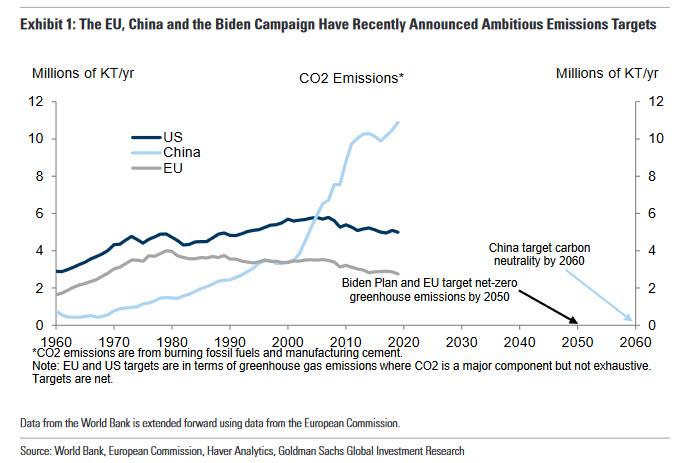

Here, a quick aside: while it has long been a favorite trope of Democrats to attack Republicans for destroying the earth with their evil emissions, the reality is that US CO2 emissions are near the lowest levels of the 20th century, and have been declining every year since the mid-2000s. The real culprit, as shown in light blue in the chart below, is China, whose emissions are more than double those of the US, and greater than the US and Europe combined. Which is truly hilarious, because recently President Xi Jinping announced that China is targeting carbon neutrality by 2060. We ask anyone to explain to us how China’s soaring CO2 emissions will magically collapse by over 10 million KT/year from the current record level to 0 in just 40 years.

None of that matters to Joe Biden of course, who has proposed a $2 trillion plan for a “Clean Energy Revolution” to achieve net greenhouse gas neutrality by 2050. And with billions to be made from aiding this crusade again “global warming”, Goldman – which has long been in the “let’s monetize climate change business” isn’t far behind.

Which is also why in a note from Goldman’s Jan Hatzius titled “Mitigating Climate Change via Taxes and Subsidies”, the bank’s chief economist writes that “the European Union, China, and the Biden campaign have recently announced ambitious targets for net carbon neutrality around the middle of the century.”

However, as the targets have grown more ambitious, Hatzius notes that it has become less clear how to achieve them, in other words: “who will pay?” To that point, Hatzius writes that “many commentators believe that a high carbon tax—the favorite climate change policy tool of many economists—would be too regressive in its distributional impact, while a low carbon tax would have little impact on emissions.”

Here the Goldman strategist disagrees, arguing that “this view is too pessimistic” and speaking the two words that will melt Democrat hearts, Hatzius says that the massive wealth redistribution resulting from the “clean energy revolution”, will actually be “highly progressive.” He explains:

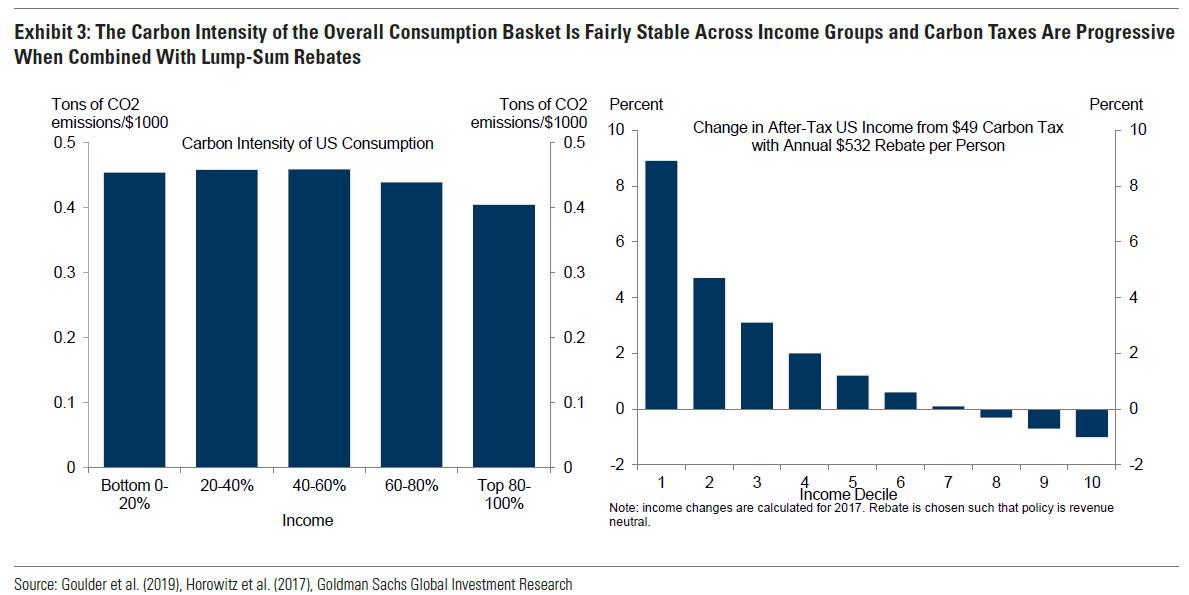

First, carbon taxes do not have to be regressive. Although low and middle income households spend a relatively larger share of their income on energy, the carbon intensity of the overall consumption basket does not vary much across the income distribution. And if revenues are rebated to households through lump-sum transfers, carbon taxes can actually be highly progressive.

To justify such “highly progressive” measures which are basically forms of wealth redistribution, Hatzius frames the debate as one of emission lowering equivalency.

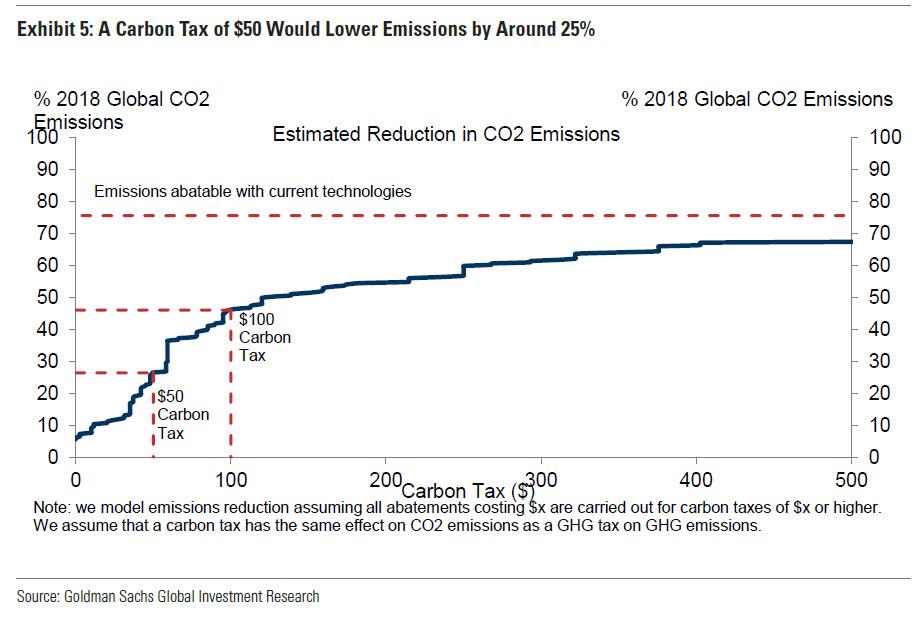

And here are some numbers: Goldman estimates that a carbon tax of $50 per metric ton—equivalent to 45 cents per gallon of gasoline—would lower emissions by around 25% over the next 5-10 years, broadly consistent with top-down studies in the economics literature.

A broader look at the carbon intensity of the overall consumption basket and the ability to rebate imply that carbon taxes are not necessarily regressive. Although lower income households spend a relatively larger share of their income on energy, the carbon intensity of the overall consumption basket does not vary much with income. To show this, we estimate the carbon intensity of US consumption by income group, combining data on carbon intensity by consumption category and US consumption shares by income group (Exhibit 3, left panel). While the top 20% of earners have the lowest carbon intensity of consumption, the differences across groups are relatively small.

False equivalency aside, Goldman next makes a lay up argument for why Biden and his socialist/progressives backers will rush to implement such taxes: Hatzius explains.

carbon taxes can actually be highly progressive if revenues are rebated to households through lump-sum transfers. Economists at the US Treasury estimate that an evenly-rebated $49 carbon tax would raise after-tax income of the bottom 10% of households by nearly 10% (Exhibit 3, right panel).

“Rebates”, of course, is just another word for higher taxes on the rich. And the punchline: “Recent polling finds that around two-thirds of the US population supports carbon taxes if the revenues are rebated.” Hardly a shock that the lower classes would be in favor of redistributing the income of the wealthy.

Finally, just to appease the environmentalists in addition to the socialists, Goldman self-servingly shows a chart according to which a carbon tax of $50 would lower emissions by around $25. But why stop there: a tax of $100 would lower emission by almost 50%, while a $500 tax would lower emissions by a lovely 70% and so on thus handing progressives a “noble” cause with which to soak the rich.

But wait there’s more, because in addition to carbon taxes, Goldman also recommends “Green subsidies” which would go a long way to further “cutting emissions”:

While a 35% cut in emissions would be far from sufficient to achieve a mid-century net zero target, the combination of a $50 carbon tax with clean energy subsidies in areas such as renewables, electric cars, and batteries could be quite powerful.

In the short run, subsidies promoting, for example, solar installation or electric vehicles purchases, should reduce emissions as clean alternatives replace carbon-intensive products. Using estimates from the research literature of the effectiveness of energy subsidies at reducing emissions and assuming that this effectiveness increases over time with technological progress, we estimate a 10% decline in CO2 emissions from an increase in green energy subsidies worth 0.5% of GDP.9 For context, such an increase in green subsidies would take global subsidies as a share of GDP slightly beyond the 2017 EU level and is roughly consistent with 20% of the Biden climate plan being spent on green energy subsidies.

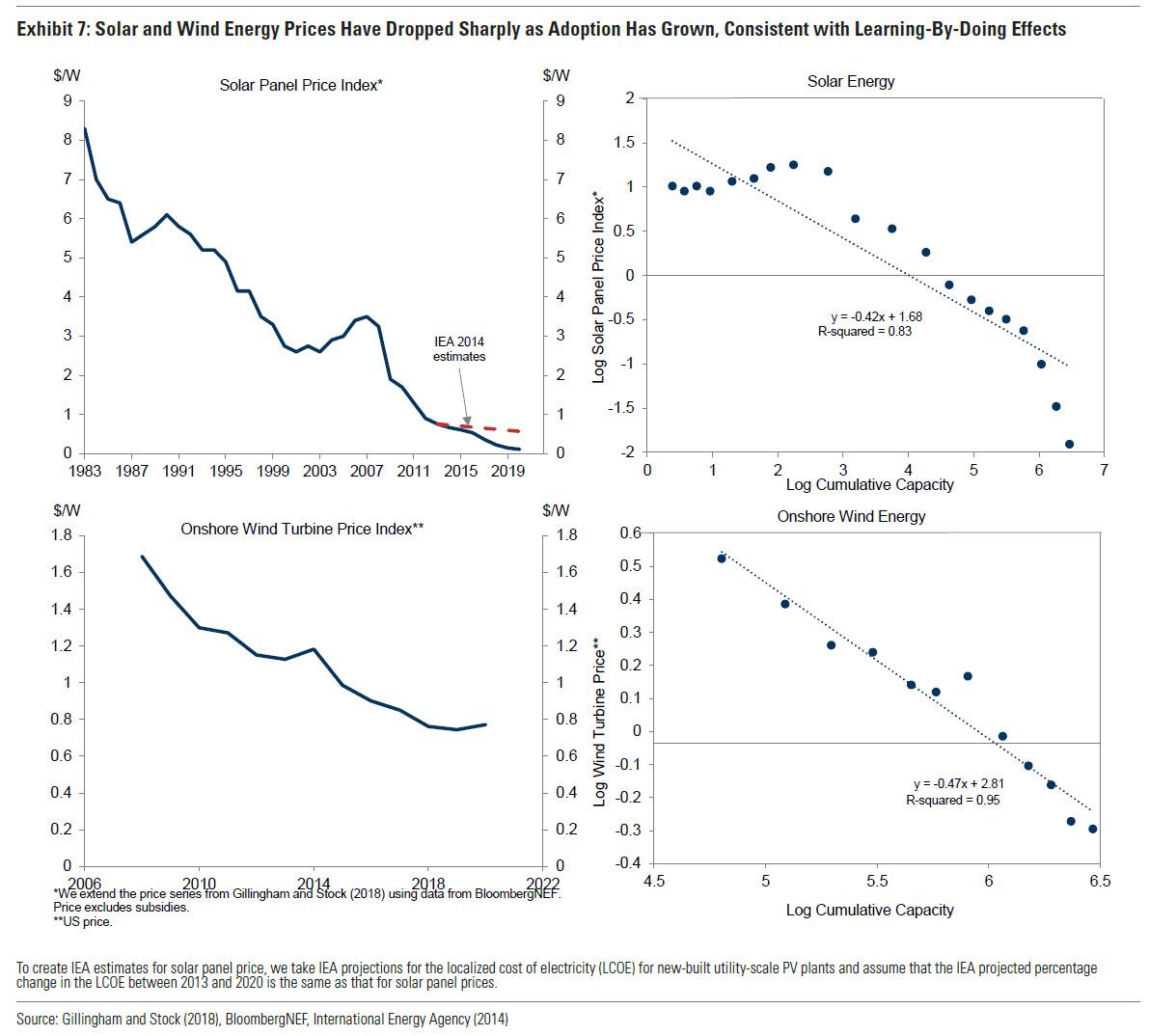

In the long run, emissions reductions would likely be much larger as the benefits from learning-by-doing and research subsidies build over time. Subsidies for production and consumption of clean tech can boost productive efficiency through accumulated experience, a learning-by-doing effect. The prices of wind turbines and especially solar panels have dropped sharply and at a much faster pace than projected by the International Energy Agency (Exhibit 7). Academic research documents that subsidies have stimulated demand, which has in turn pushed down prices via learning-by-doing1 The right panels, which plot prices against cumulative capacities, suggest that a doubling of cumulative solar and wind capacity is associated with a 40-45% reduction in prices.

What was left unsaid is that government subsidies is just another form of taxpayer-funded government generosity. And yes, the middle class will feel the biggest hit, because while the top 10% can easily afford any newly unveiled government taxes, it is the middle class that will suffer the most from the loss of discretionary spending, which will be repurposed to fighting… China’s emissions.

Goldman’s conclusion: there is great news, and global emissions will drop sharply… all that is needed is some aggressive combination of taxes and subsidies:

Taken together, our estimates imply that a combination of a carbon tax and green subsidies could reduce emissions by 45% over the next 15–20 years. This 45% reduction over the next 15-20 years would be a major step in the direction of net carbon neutrality over the longer 30-40 year horizon targeted by governments, at which point negative emissions technologies such as carbon capture and storage could also play a large role. In short, our analysis suggests that a combination of carbon taxes and green subsidies can help the world achieve its increasingly ambitious targets for emissions reductions.

After all that, just one open question remains: how will Goldman wiggle its way into extracting 2-3% from every “climate change” tax and subsidy transaction soon to be imposed on the middle class by the Biden administration. We expect to have the answer shortly.