Aktieugebrevets opdaterede kortsigtede aktiestrategi op til og efter rentemøde i aften beskrives i en særskilt meddelelse, som udsendes senere i dag.

Well, that was timely. The August CPI came in at -0.1% and is up a mere 0.2% over the past year. So Janet Yellen can now say, look ma, no inflation!

Once again, therefore, the Fed has an excuse to keep shoveling free money into the casino. If Stanley Fischer insists that more evidence is needed that consumer inflation is progressing toward its intended 2% destination, and Bill Dudley persuades Yellen & Co. that financial conditions have already “tightened” by 25 basis points, as measured by Goldman’s spurious Financial Conditions Index (GSFCI), we will get the 81st month of ZIRP; and with it a short-lived relief rally, not the Wall Street hissy fit that is long overdue and eventually unavoidable.

Alas, we will also get a vivid demonstration that main street America is being put in harm’s way by the posse of cowards, dissemblers and academic fanatics who run the world’s most powerful central bank. The evidence is right below in the summary table from this morning’s BLS inflation report.

It shows quite clearly that prices of commodities and goods are falling in the wake of the intensifying tide of global deflation, while the cost of shelter and domestic services is moving higher at a spritely pace. Accordingly, it does not take a PhD in economics to figure out that the resulting “average” rate of price change for the BLS’ dubious market basket of consumer items is purely a statistical accident, and absolutely outside of the Fed’s ability to shape.

In fact, it makes a mockery of the Fed’s insensible commitment to 2% inflation. The latter has always amounted to a policy target confected from wholecloth, anyway, since it is not contained in or required by the Humphrey-Hawkins Act, nor is it grounded in a shred of historic evidence that decimal points of difference around 2% consumer inflation have anything whatsoever to do with economic growth or gains in societal wealth and living standards.

But now you have a clean bifurcation in the price indices that proves the utter pointlessness of so-called inflation targeting. One the one hand, virtually everything which is directly priced and traded on world markets is carrying a negative sign on a year-over-year basis.

That includes gasoline, which is down 23.3% since last August; fuel oil, which is lower by 34.6%; and gas and electric utilities, which are down by 11.5% and 0.5%, respectively. Likewise, all other commodities are lower by 0.5%, while apparel prices posted down 0.9% versus prior year.

Even the trend in car prices confounds the Fed’s inflation mongering. Owing to seven years of drastic interest rate repression, the amount of direct auto credit outstanding is up nearly 45% and funding for the massive fleet of new leased vehicles has risen even more rapidly.

Accordingly, the auto dealer lots are once again being flooded with used vehicles. This surging supply has driven down average used car prices by 1.5% during the past year, while the price of new cars remains essentially flat in world swamped in excess production capacity.

![]()

In any event, it is truly hard to comprehend why a central bank charged with the objective of price stability would object so relentlessly to lower gasoline, utility, apparel and car prices. Surely these academic pettifoggers do not actually believe that hard-pressed main street households, which are finally getting a break on their gas and utility bills, have decided to hoard cash because the overall CPI came in at zero.

Indeed, the whole theory that “low-flation” undermines real economic growth, detracts from spending that would otherwise be directed at consumption and capital goods and somehow subtracts from labor and entrepreneurial inputs on the free market is an embarrassing shibboleth; it survives only because it is a convenient cover for hyperactive central bank intrusion in the money and capital markets and for the massive subsidies to speculation that ZIRP and QE inherently provide.

Indeed, here is a news flash for the “moar inflation” gang huddled in the Eccles Building. Since the turn of the century there has been too much inflation relative to the earnings power of American workers in today’s global economy. They are not spending up a consumption storm for the self-evident reason that real household incomes have shrunk, not because they are striking in behalf of higher inflation!

![]()

At the same time, the balance of the BLS table tells the Fed’s covey of inflation doves to shut-up and sit down. By any practical reckoning, upwards of two-thirds of living costs for average households are accounted for by shelter, transportation, medical care, education, entertainment and the like. Yet the year-over-year price change for the first three of these items was 3.1%, 2.1% and 2.2% respectively, while the cost of going to restaurants was up 2.7% and education costs (not shown) were up by 3.5%.

Nor are these one-year gains for the principal domestic services categories some kind of recent aberration that will lapse back into sub-2% inflation land if the Fed does not keep interest rates pinned to the zero bound. In fact, the 2.6% gain since last August for all services less energy services, as shown above, is spot on a trend that has been extant for the entirety of this century to date.

Thus, during the year ending in August 2014, the index for services less energy was up an identical 2.6% to the amount shown above for the most recent 12 months. And the index rose by 2.5%, 2.4% and 2.4%, respectively, for each of the prior three years. Indeed, since the turn of the century, the index for services less energy services has risen by 50% or at a 2.6% compound rate; and there has been no recent trend toward deceleration whatsoever.

![]()

There you have it. If the US economy were a giant closed-system bathtub, which it manifestly is not, the price index for domestic services would arguably be the part of the cost-of-living basket most amenable to central bank influence.

Yet as today’s BLS report made clear, America’s financially strapped households don’t need no stinkin’ help from the Fed when it comes to inflating the cost of shelter, medical care, transportation and most other services. Their paychecks, which grew at an anemic 2.1% over the past year, have already been clipped by 2.6% for these every day services.

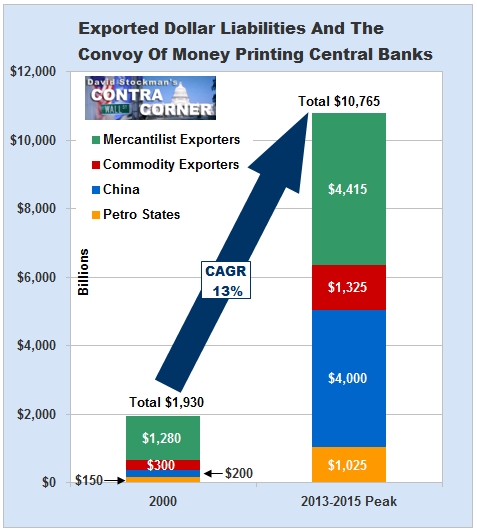

And that takes us back to the global deflation registered in the declining price of commodities and goods, and to the chart we posted yesterday on the bloated balance sheets of central banks outside of the US and Europe.

To make a long story short, the money printing jig is up. The stupendous inflation of yen, won, yuan, real, rubbles, ringgit, riyals, baht etc. that was spurred by the mad money printers in the Eccles Building over the last two decades has reached its apogee. As a consequence, the the tide of domestic credit that spurred a rambunctious but artificial boom in these economies has gone bust; prices and profits are now succumbing to a deflationary tide.

The epicenter of this reversal is the Red Casino in China, but it is only the leading edge of collapse among the petro-states, commodity exporters and mercantile exporters which feasted on the China boom.

Needless to say, the idea that the US economy can be decoupled from these epochal forces is both naïve and disingenuous. Domestic business activity from Caterpillar’s engine plants in Illinois to Houston chemical plants to sand haulers and drilling rigs in the Baaken shale patch will be seriously disrupted.

But what is unassailable is that the falling prices for commodities and goods emanating from the world’s deflationary bust can not in any way, shape or form be countered by supplying even more free money to the Wall Street casino. Nor does averaging up the latter with the deeply embedded domestic service inflation once again evident in today’s CPI release result in anything more than statistical noise.

If the Fed chooses to stay the ZIRP course yet another month it will be unmistakably evident as to why. It has unleashed the furies in the casino and is terrified by the prospect of reining them in.

Doing so will reveal that the Keynesian central banking project of the last two decades has been a failure and a fraud. It may even bring pitchforks and torches to the nation’s capital in search of the small posse of cowards and zealots who are setting the stage for still another thundering financial crash.

.

“Unless there is a miraculous turnaround