Fra Zerohedge/ Goldman Sachs

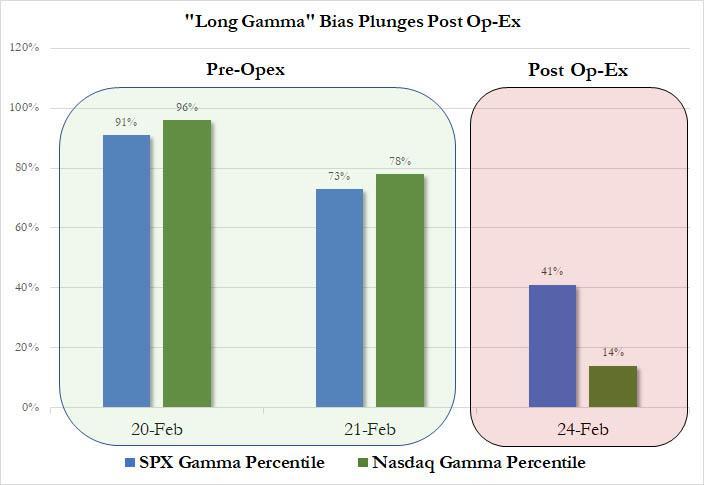

Earlier today we noted that according to Nomura’s Charlie McElligott, the biggest risk facing the market was a “shock down” as dealer gamma bias had evaporated following Friday’s Op-Ex (especially in the Qs)…

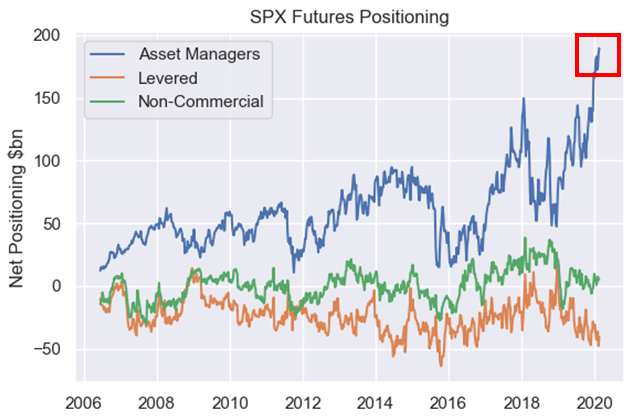

… which meant that instead of providing a natural buffer to any selling (“buy weakness/sell strength”), dealers are now procyclically positioned, and any accelerated selling would only lead to more selling, resulting in even lower gamma, even more selling, and so on, in a typical gamma feedback loop. A separate, and just as tangible risk according to McElligott, was the record positioning (100%ile) across asset managers, whose net long exposure across SPX futures hit a record $190BN.

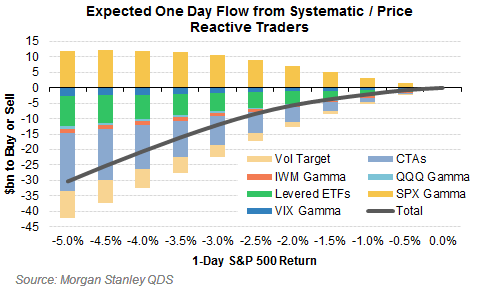

At roughly the same time, Morgan Stanley’s Christopher Metli, executive director in the bank’s QDS division, looked at selling pressure from another source, and calculated that while there is up to $10BN in notional selling pressure today from “systematic and price reactive traders”, this liquidation amount could soar to $60BN which would “generate a self-fulfilling downward move in QDS’ view” if the S&P closes below 3,235 or just a handful of points from here.

As Metli writes, “on the worst pre-open selloff since June 24th 2016″…

… QDS estimates $5 to $10bn in equity needs to be sold today with an additional $20bn over the rest of the week from systematic and price reactive traders.

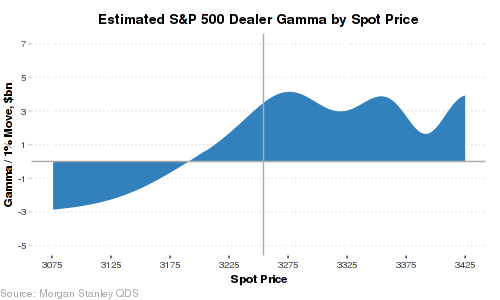

As MS further notes, this number would be a lot higher except dealers are long $3 to $4bn of SPX gamma per 1% move here…

… which cuts today’s number in half (i.e. option rebalancing is about $9bn to buy, offsetting other drivers of supply), and the rally in bonds cushions some of the blow as well.

That said, for every extra 50 bps selloff here QDS models roughly $20bn in more supply this week, and a close below ~3235 (-3%) on the SPX threatens to bring in enough supply ($60bn+ total) this week to generate a self-fulfilling downward move in QDS’ view.

The silver lining: some of this supply should be offset by pension demand – Metli has previously estimated (when stocks were at all time highs) a US equity-for-sale imbalance for asset allocators this month, but today’s selloff, which has sent yields to record lows, flips that number to $7BN to buy over the next two weeks (and $15bn ex-US). Yet even so, while this demand is an “offset”, the MS quant warns that “it should come through more slowly than the supply.”

* * *

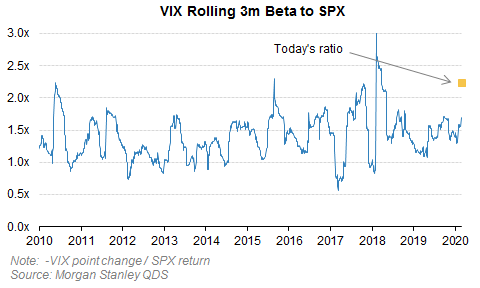

We doubt that a blind liquidation panic causing even more selling, is news to any trader. However, what is notable is that the pace of the selloff (i.e. volatility) is the key driver of how much needs to be sold, according to MS, which echoes McElligott in observing that CTA triggers / moving average crossovers “are far away for US futures so most of the likely supply comes from deleveraging on the back of higher volatility.”

… which according to Morgan Stanley is a bigger move than normal beta would suggest, but isn’t a massive overreaction (over 3x ratio on a daily basis it starts to get extreme).

In other words, despite the frenzied liquidation at the start of trading, for now at least the volatility market is showing relatively ‘normal’ behavior for this size selloff.