Uddrag fra Reuters:

Speculators’ net bearish bets on 30-year Treasury bond futures grew to a record high in the latest week, data from the Commodity Futures Trading Commission showed on Friday, reflecting expectations of higher yields on longer-dated U.S. government bonds.

The amount of speculators’ bearish, or short, positions in 30-year Treasury futures exceeded bullish, or long, positions by 230,312 contracts on Oct. 6, a record, according to the CFTC’s latest Commitments of Traders data.

The 30-year yield, which moves inversely to prices, has rallied to a four-month high since August, when Federal Reserve Chair Jerome Powell announced that the central bank would allow periods of higher inflation in order to average its target 2% rate.

————————————————————————

Fra Zerohedge om shortspekulation i US obligationsrenter:

….. everyone and their grandmother is already in it, and in fact, one can argue that the entire Morgan Stanley line of thought is not contrarian at all, with markets now appearing to fully price in a reflation trade.

In fact, for those betting on outcomes, the best upside/downside risk-adjusted trade is to fade the reflation trade which in the past 3 weeks has allowed Russell stocks to strongly outperform their Nasdaq-based deflationary proxies. In further fact, for those cynics among us, one could almost argue that Morgan Stanley is merely hoping to take the other side of the trade that it is pitching to its clients. The next few days of trading should reveal the answer if the unprecedented 30Y short and heavy positioning into further curve steepening can continue, or will punish the momentum-chasing macrotourists.

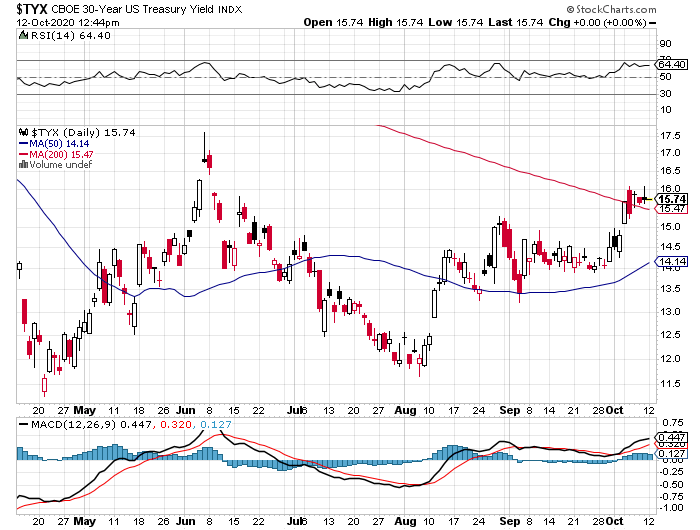

Den 30 årige amerikanske statsobligations rente er netop gået op gennem 200 dages glidende gennemsnit: