The Melt-Up Machine

Tech keeps trading like a self-reinforcing melt-up machine. Every small dip gets mechanically bought, flows keep chasing AI and semis, and upside positioning continues feeding on itself despite already crowded large-cap tech exposure.

Upside call skew across large-cap tech is now reaching meme-mania style extremes, increasingly echoing melt-up environments like 1997 and parts of 2003.

Perfection

NDX futures bounced right off the lower end of the steep trend channel, with the 21-day moving average still very much intact. Upside pain remains the dominant force.

Source: LSEG Workspace

Tech mania

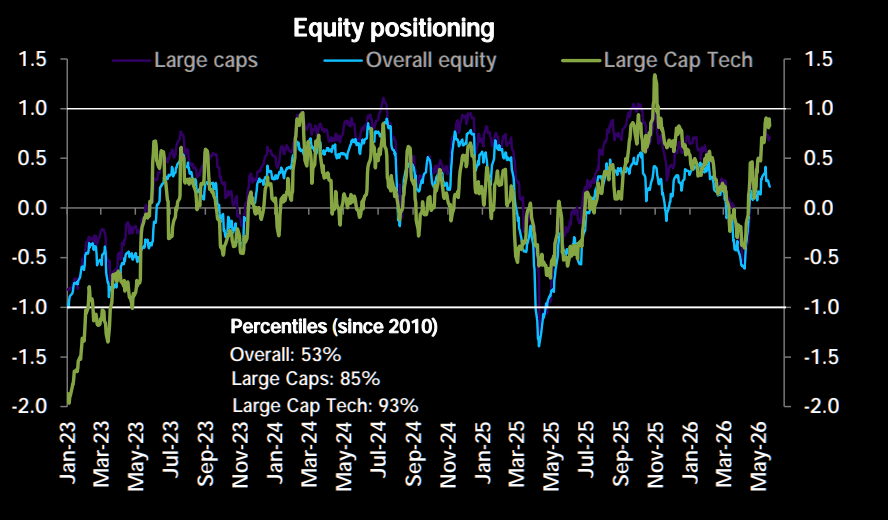

Positioning in equities overall still looks fairly neutral, but large caps and especially large-cap tech are increasingly crowded. Percentiles since 2010 stand at 53% overall, 85% for large caps, and 93% for large-cap tech.

Source: DB

Must have tech

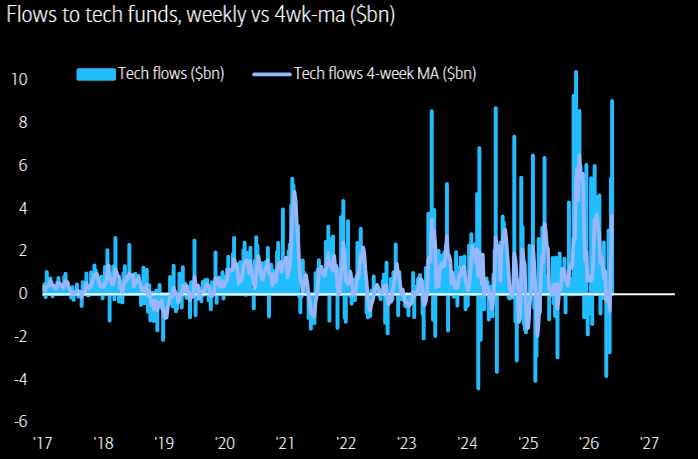

Massive inflows into tech again. We just saw the biggest weekly inflow to tech since October last year.

Source: BofA

Must have AI

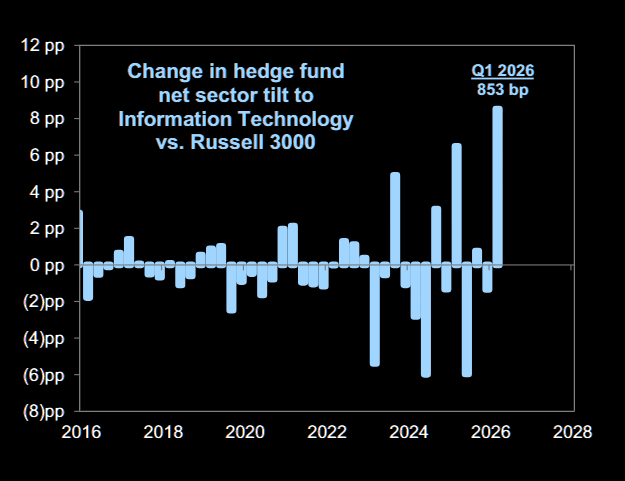

Hedge funds entered Q2 2026 going all-in on AI. Their net tilt toward Information Technology surged by +853bp, marking the largest quarterly increase to the sector on record.

Source: GS

Source: GS

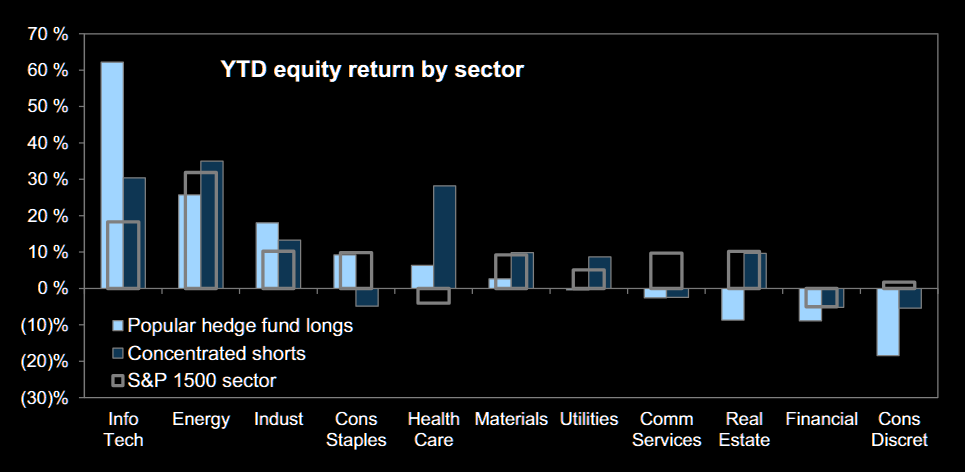

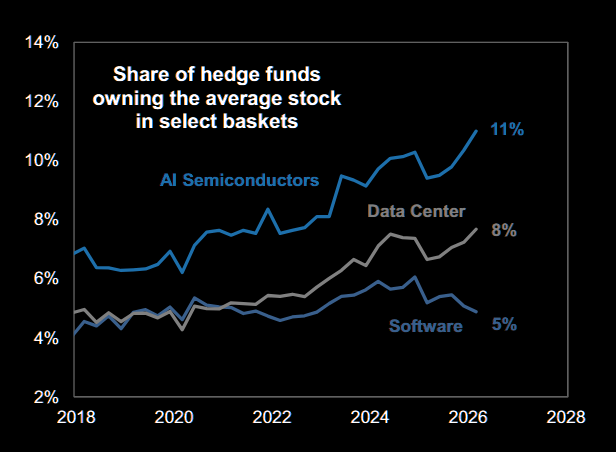

Loving it

Hedge funds keep piling into AI semis and data center trades.

Source: GS

1997

The 1997 pattern we outlined weeks ago continues playing out well.

Source: LSEG Workspace

2003 vibes

The current environment is very different from 2003, when the bull market that lasted until the GFC began, but there are still similarities in how this year is unfolding, at least from a pattern and psychology perspective.

Source: LSEG Workspace

Well bid vol

VXN has moved lower recently, but vols are still elevated relative to mid-April even as tech continues squeezing higher. Options pricing remains firm, although true upside panic has yet to fully kick in.

Source: LSEG Workspace

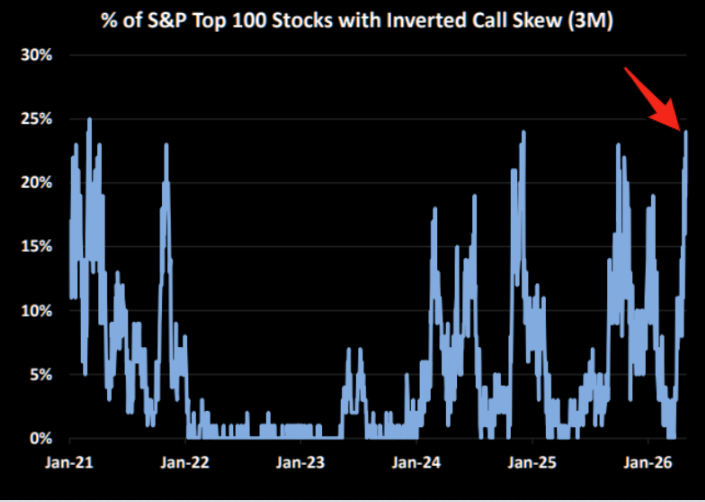

Calls on steroids

Almost 25% of the SPX top 100 now trade with inverted call skew (CBOE), matching extremes last seen during the 2021 meme mania. GS sees the skew distortions as attractive for collars, allowing investors to monetize rich upside call premiums while using the proceeds to buy downside hedges.

Investors are increasingly overpaying for upside convexity in large-cap tech. The market is starting to resemble a momentum chase where upside optionality itself has become the asset in demand.