Uddrag fra Zerohedge/Morgsn Stanley/ Bank of America:

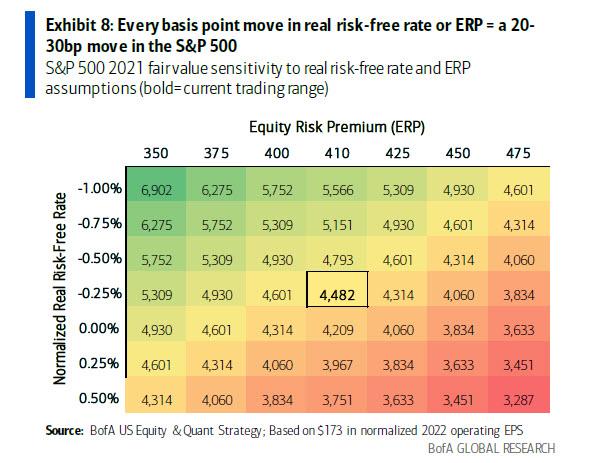

Key among them was her observation that in a world where the FAMGs trade as a long-bond substitute, the market’s duration risk has never been higher. Naturally, this means that the market’s interest rate risk is at a record high, and according to BofA calculations, the S&P 500 equity duration equivalent is a 36-year zero-coupon bond (and is why the FAAMGs now trade interchangeably with long bonds).

For the non rates gurus out there, this is a huge number…. How huge? It is so big that, according to Subramanian’s calculations, every 10bp increase in the discount rate equates to a 4% decline. And with valuations (which as DB noted are at all time highs and risk sparking a “hard correction” in stocks) leaving no margin for error, this means that once the Fed finally acknowledges the soaring inflation – it can pretend it’s not there only so long – it’s going to get very ugly for stocks.

But… but… what about every socialist’s favorite monetary pet “theory”, the “Magic Money Tree” (also known as Modern Monetary Theory or MMT) theory which claims that one can engage in absolutely idiotic monetary and fiscal policy with no negative consequences ever? Doesn’t it imply that rates will never have to rise and the Fed can taper so gradually as to never upset markets (you see, socialist theories don’t actually reflect the real world, and certainly not real world prices, so just bear with us). Well, even here there is a problem, because even if one relies on “MMT math” – as BofA puts it – the market will remain at best flat through 2022. That’s because based on 2022 EPS of $215E and BofA’s house forecast for the Fed balance sheet through year-end 2022, post-GFC correlations between non-earnings driven market cap changes and the rate of change of Fed balance sheet expansion would suggest essentially no change in the S&P 500 from current levels for year-end 2022.

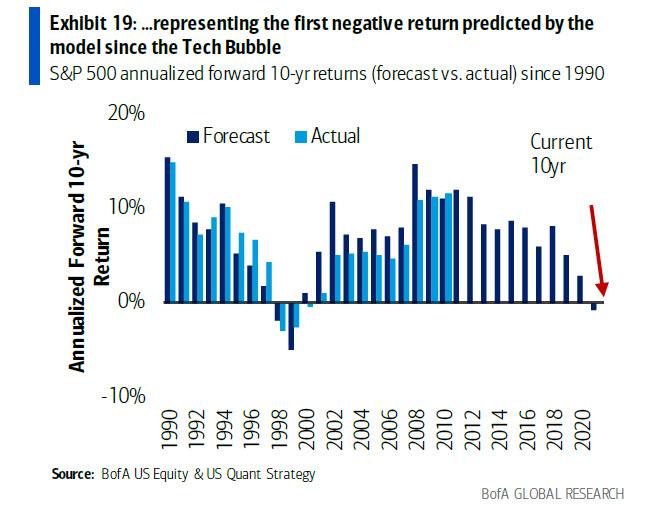

Rates – and idiotic socialist flights of fancy aside – Subramanian also looked at one of her favorite indicators, the price to normalized earnings which has a very strong relationship to subsequent S&P 500 returns over the long haul. With the S&P 500 current sporting a trailing normalized PE ratio of 29x, the BofA strategist calculates that the 10-year annual 12-month price return of -0.8%, “represents the first negative returns since the Tech Bubble.” In other words, ten years from now stocks will be lower than where they are now.

And while we gernally share Savita’s sentiment that the current episode in market lunacy will end badly…

This may not end now. But when it ends, it could end badly: If taper means no upside to the S&P 500, tightening would be worse. Canaries are chirping –PPG, a barometer of industrial activity, aborted guidance on supply chain woes; credit spreads have stealthily widened, and our valuation model (~80% explanatory power for S&P 10yr returns) now indicates negative returns (-0.8% p.a.) for the first time since ‘99

… we are certain that there is no way on earth – literally – that the Fed will ever allow 10 years to pass with zero wealth effect, and it’s also why we fully expect a major crisis in the near future, one which leads to a relatively modest market crash only to trigger ETF and stock buying by the Fed which by then will be directly wiring digital dollars into every minority’s digital wallet with the explicit instructions to spend said digital Fedbucks on stonks, which will soon be the only arbiter of social welfare in the US.