Kina havde i første kvartal et voldsomt fald i væksten på grund af coronakrisen, med en negativ vækst på 6,8 pct. Det er første gang i årtier, at Kina har haft minusvækst. Faldet var lidt større end forventet. Til gengæld er der ved at komme gang i økonomien igen, og der er forventninger om en kraftig vending resten af året. Men det hjemlige forbrug og eksporten vil ligge underdrejet.

Uddrag fra Nordea:

China: The COVID-19 broke the GDP curve

China delivered its first economic contraction in Q1, as a result of the COVID-19. The economy is taking longer time to return to previous activity levels. Especially consumer goods and service sector will see longer-lasting effects.

As the first country to have experienced the COVID-19 outbreak, China is a step ahead of the rest of the world in terms of the Coronavirus curve and now the GDP curve.

Not surprisingly, the economy took a hard hit from the containment measures that led to a month-long standstill in February. The GDP growth in Q1 was an unprecedented low of -6.8% y/y (-9.8% q/q), more negative than market consensus (-6.5% y/y) and less so compared to our forecast (-10% y/y). It’s the first contraction of economic activities since data began in 1992.

The CNY and CNH have not seen large movements on the back of the release, and Chinese equities are in the positive territory at the time of writing.

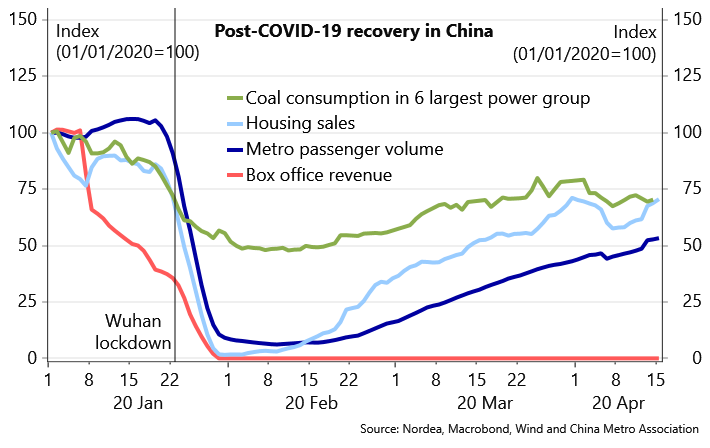

Despite efforts to lift restrictions and resume work since early March, most sectors are taking longer time to return at pre-shutdown levels. Large industrial companies are about at full operation but their smaller counterparts are still 20% below normal capacity. The offline service sector, such as restaurant, travel and sports, remains in crisis mode.

This is in line with the March number published at the same time as the GDP figure. Industrial production rebounded in March, while retail sales saw little signs of improvement.

Small and medium-sized enterprises (SMEs) are more export-oriented and can expect to take a disproportionately large hit by the lockdowns in the advanced world in Q2. The government has stepped up support for this group as they are critical to the economy. They account for about 80% of the total employment and nearly 70% of GDP. They also tend to be more innovative than their larger counterparts, a trait that is highly valued by the government.

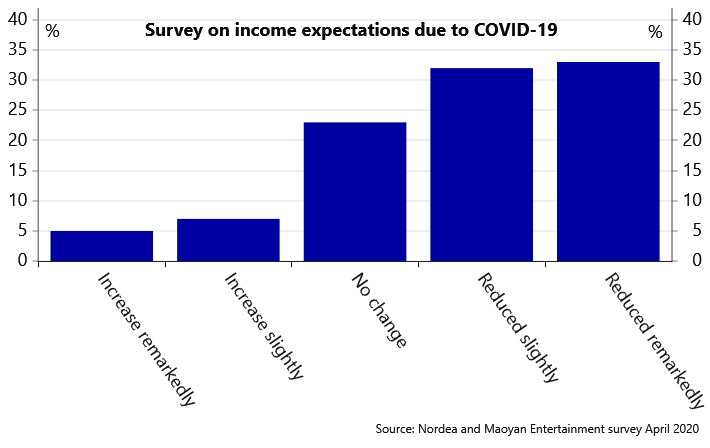

Rising job and income insecurity is exactly the biggest hurdles for the consumer goods and the service sector to return to normal activity. A recent consumer survey showed that 65% of respondents expect a income loss to mild and severe magnitude. That is likely a major concern for Beijing.

In addition to aids to the SMEs, the lion’s share of the fiscal stimulus goes to infrastructure investment, which as usually will take the responsibility to generate growth. About a half of the country’s provinces have announced a total investment plan of CNY6.6tn (USD930bn) to be completed this year. Some of the projects were already planned for this year but we think the total size will be bigger than this at the end of the year. We also think that Beijing will continue relying on fiscal stimulus rather than monetary.

The government has been easing less aggressively on monetary policy, especially compared to most other central banks. The PBoC has hesitated to cut the benchmark one-year rate for the fear that lower deposit rate would cause more social dissatisfaction on top of the virus scare. But it is too early to write off a rate cut just yet given the high uncertainty surrounded the COVID-19 development and the longer time it takes to recover in China.