Resume af teksten:

Inflationen i USA steg i marts, hovedsagelig på grund af en stigning i benzinpriserne. Den samlede Consumer Price Index (CPI) steg 0,9% måned-til-måned, med benzinpriserne, der steg 21,2%, som den primære faktor. Flypriser og tøjpriser steg også, henholdsvis 2,7% og 1% måned-til-måned. Ekskluderer man mad og energi, steg inflationen kun 0,2% i marts, lavere end forventet, hvilket skyldtes fald i brugtbilspriser og andre omkostningsreduktioner. Trods stigende energipriser vurderes inflationen at være forbigående, da arbejdsmarkedet er mere afdæmpet med lavere lønvækst. Højere energiomkostninger kan resultere i reduceret forbrugsstyrke, med mulighed for lavere inflation næste år, hvis energipriserne falder.

Fra ING:

Gasoline price hikes prompted a jump in headline inflation, but core pressures were more benign than feared. We have much greater confidence that inflation will be transitory this time around, given the lack of demand impetus and weaker corporate pricing power versus 2022

US CPI for March rose on higher gasoline prices, but we do think higher inflation will be transitory

Gasoline prompts an inflation jump, but core pressures were softer than feared

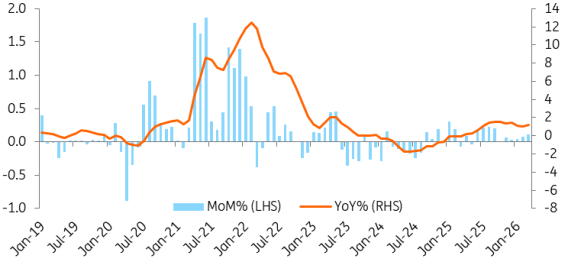

US headline CPI showed prices rising 0.9% month-on-month in March, as expected by the market, with a 21.2% MoM jump in gasoline prices contributing the bulk of upside impetus. Airline fares rose 2.7% MoM and apparel prices rose 1%. However, excluding food and energy, inflation was softer than feared, rising only 0.2% MoM/2.6% YoY versus expectations of a 0.3%/2.7% outcome. This was thanks largely to a 0.4% drop in used car prices, a 0.2% decline in medical care and a 0.4% decline in “other goods & services”. Housing costs, the single biggest component by weight, rose 0.3%.

The economy has handled tariffs well, with limited goods price inflation. Core goods prices (ex-food and energy), remain benign, rising just 1.2% year-on-year. Instead, the tariff cost is largely being borne by the US corporate sector – next week’s import prices will show another monthly rise, indicating foreign producers are not “paying” the tariffs.

Core goods price inflation

Source: Macrobond, ING

“Transitory” inflation far more likely this time

While the rise in energy costs will push the annual inflation rate even higher over the next few months, we don’t expect a repeat of 2021/22 when the Fed called inflation pressures “transitory” only to then hike rates 525bp as inflation got within touching distance of 10%.

The supply shock this time around is arguably far smaller, focused in the US’ case on gasoline and other fuel costs rather than all goods AND energy in the wake of pandemic-dislocated global supply chains. More importantly, there isn’t the demand impetus this time around to generate broad and persistent inflation. 2022 saw 4.5mn jobs added, wage growth touching 6%, significant pent-up demand, record savings levels and stimulus checks. This time we have a much cooler jobs market with wage growth closer to 3%, weaker confidence and flat-lining real household disposable income.

Rising fuel costs likely to be demand destructive

Fuel price hikes are more likely to be demand destructive, via reduced discretionary spending power. This point was underlined by yesterday’s personal income and spending report, which showed real household disposable incomes were flatlining before the Middle East conflict. We are likely to see this turning negative in coming months. Furthermore, if we see a successful outcome for the US-Iran negotiations and the flow of oil and gas starts to trickle out before coming more of a proper flow through the second half of the year, lower energy costs could possibly drive inflation below 2% at some point next year. As such, we still think interest rate cuts are more likely than hikes, especially given the Fed’s dual mandate (price stability AND Maximum employment).

What would change our Fed view? If inflation expectations were to start rising and wage demands pick up, but right now both market and consumer long-term inflation expectations appear anchored and there continues to be more unemployed Americans than there are job vacancies – remember back in 2022 there were two job vacancies to every unemployed American. This highlights how the demand-supply balance has shifted within the jobs market and explains why we think second-round price effects will be far more muted this time relative to the post-pandemic inflation shock.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.