Den engelske centralbank virker en smule mere optimistisk omkring økonomien end ventet, fremgår det af dens seneste udmelding, og i går gav den ingen signaler om en snarlig rentestigning. ING tror, at renten først hæves i 2023 – tidligst, som ING udtrykker det.

Upbeat Bank of England offers no new clues on rate hikes

The Bank of England’s latest statement is a little more upbeat than might have been expected, but crucially offers no new clues on rate hike timing. We’re still expecting the first rate rise in early 2023, on the assumption inflationary pressures ease through the middle of 2022

The Bank of England’s latest message is a cautiously upbeat one, though it’s clear that policymakers are essentially in a holding pattern for the time being. The central bank is caught between higher-than-expected inflation and encouraging activity data, and mounting uncertainty surrounding Covid-19.

The Bank has kept both rates and QE on hold this month, despite a vote to end the latter early from outgoing Chief Economist and arch-hawk Andy Haldane. But more importantly, the committee opted against offering any more concrete hints of future tightening. Indeed the BoE’s latest statement borrows both from the ECB and Federal Reserve hymn sheet – from the former by emphasising against a premature tightening in monetary conditions, and from the latter by signalling it wants to see ‘significant’ progress before looking at removing stimulus.

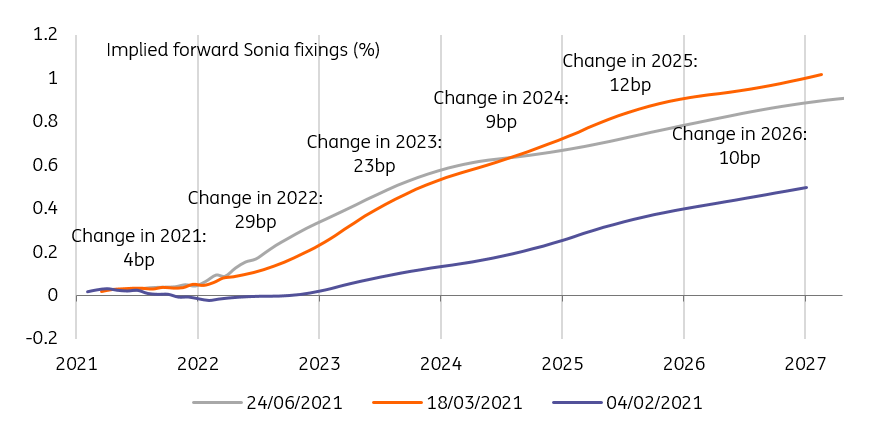

The lack of stronger hints about a rate hike timing is arguable because there’s no real need to guide markets at this stage. The Bank’s May projections, which were based on roughly 20 basis points of tightening over two years, showed inflation roughly at target over the medium-term. That’s an implicit way of saying that market pricing was broadly right, and since then, markets have brought forward their expectations and are now pricing two rate hikes by the middle of 2023.

Ahead of the meeting, markets were pricing more than two hikes by the end of 2023

Chart courtesy of ING’s Rates Strategy Team

But assuming the near-term Covid-19 concerns fade towards the end of the summer, following widespread double vaccination, then the debate over rate hike timing is likely to gain more momentum. While the latest inflation reading was higher than expected, and the Bank now expects inflation to exceed 3% at some point this year, our view and theirs is that price pressures will subside through 2022. That in turn reduces the imminent pressure to ease stimulus, and we’re currently pencilling in the first move in early 2023.

On the QE side, despite Andrew Haldane’s vote, we very much doubt the Bank will curtail the programme early. The BoE remains on track to actively stop expanding its balance sheet at the end of the year – having tapered the pace of purchases last month. Unexpectedly, ending the scheme early would potentially set a precedent in the eyes of investors, and risks limiting the potency of future QE programmes.

Uncharted territory for the BoE

That said, one thing that’s increasingly clear under Governor Andrew Bailey is that the Bank will unwind the size of the balance sheet as part of the future tightening cycle.

This is uncharted territory for the BoE so communication surrounding this process is likely to change fairly glacially. But as we wrote a few weeks ago in more detail, one option would be to stop/reduce reinvestments of proceeds from maturing bonds, perhaps by setting an annual ‘unwind’ target. One consequence of this is that the terminal Bank rate might be lower than it might theoretically have been without balance sheet normalisation.

As with rate hikes though, we think this is a 2023 story at the earliest.