Resume af teksten:

Den britiske økonomi voksede med 0,5% i februar. Væksten er i tråd med en tendens fra 2022, hvor første kvartal typisk viser stærkere vækst end resten af året. Inflationen påvirker væksten, da prisstigninger ofte forekommer i årets første måneder. Det seneste opsving hænger delvist sammen med forbedringer i indkøbschefindekserne fra januar og februar. På trods af den nuværende stigning i BNP, forventes væksten at aftage mod sommeren, da inflationen kan stige til 4%. Private lønstigninger forventes at forblive omkring 3%, hvilket kan føre til faldende reallønninger. Højere energipriser kan bidrage til stigende arbejdsløshed. Bank of England forventes at holde renten uændret på 3,75% frem til 2026.

Fra ING:

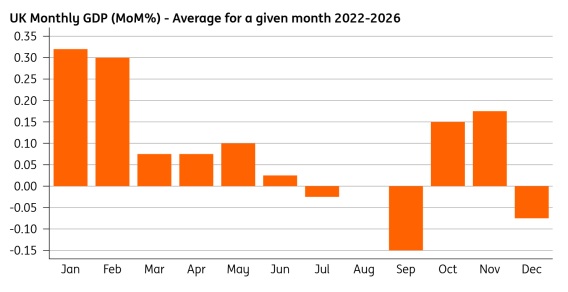

UK output surged in February, but it’s in line with a trend dating back to 2022, where growth is stronger in the first quarter than across the rest of the year. We’re taking this latest data with a pinch of salt

The UK economy grew by 0.5% in February, but the outlook points to a slowdown amid the ongoing Middle East war

If it sounds too good to be true, then it probably is.

That’s our initial reaction to the apparent surge in UK GDP in February, up 0.5% month-on-month. It’s consistent with a trend which dates back to 2022, where growth has tended to come in much stronger in the first quarter than over the rest of the year.

We suspect this can be traced back to the period of higher inflation and the tendency of price hikes to be geared towards the first few months of the year, something which doesn’t appear to be fully adjusted for in the seasonal adjustment and/or deflation process. We wrote in our reaction to the January data that February or March could see a strong bounce-back for exactly this reason.

Admittedly, the latest improvement does partially marry up with the improvement in the purchasing managers indices (PMIs) seen in January/February. But most of the latest surge, we suspect, is noise.

Monthly GDP has a tendency to come in hotter in Jan/Feb

Source: Macrobond, ING

All of this is old news anyway, given the crisis we find ourselves in today. Growth is likely to slow regardless into the summer as inflation rises towards 4% beyond July. At a time when private sector wage growth is closer to 3% and, if anything, is biased even lower in the short-term, real wages are set to fall. Higher energy prices are also likely to add to recent increases in unemployment, at a time when corporate pricing power is depressed.

This is why we’re still not convinced the Bank of England will hike rates this year. It’s a close call, which becomes closer still if the disruption hasn’t materially improved by the time of the June meeting. But for now, we’re looking for rates to stay unchanged at 3.75% throughout 2026.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.