ING vurderer, at renten på de tyske Bunds bevæger sig opad i sommerens løb, dog ikke til et højt niveau. Men hvad gør ECB? Centralbanken er “the wild card”, mener ING, der tvivler på, at ECB kan fortsætte sit opkøbsprogram i samme omfang som hidtil.

Higher Bund yields : What to expect when you’re expecting

Higher Bund yields are to be expected this year, and the rise may well be front-loaded. Euro sovereigns have taken the upcoming PEPP purchase slowdown on the chin, but corporate credit and Emerging Market sovereigns have escaped unscathed.

Unstoppable Bund, but the ceilling isn’t high

One development that hasn’t escaped European investors is the almost parabolic rise, at least by historical standards, in the German Bund. At around -0.1%, our 0% target for 10Y Bund yields looks eminently achievable this quarter. More is to come but, first, how did we get here?

With the benefit of hindsight, the rise in Bund yields from their pandemic-induced depth looks like the logical consequence of the strengthening European economic recovery and concerns relating to an adjustment in monetary policy. Neither was inevitable, however.

On the first point, it is fair to say that sentiment indicators have jumped ahead of the widespread reopening on the back of an accelerated vaccination programme. In fact, when EUR rates markets turned this year, much of Europe was actually tightening restrictions due to another wave of Covid-19 cases.

On the second point, the ECB at its March meeting has actually tried to stamp out a rise in yields it considered unjustified by economic conditions. It did so by accelerating bond purchases under the Pandemic Emergency Purchase Programme without changing its eventual size, €1.85tn. As the announcement in effect mostly brough purchases forward, its impact could only have been transitory. And indeed, yields stabilised for a few weeks before resuming their rise.

More upside than downside for yields

We expect both these factors will continue to drive Bund yields higher, to 0.2% this year. On the economic front, hard economic data should validate the recent improvement in sentiment, but risks abound. A failure to stamp out Covid-19 outbreaks could harm the all-important tourism sector this summer. Signs of overheating and rising prices could also derail a fragile recovery.

The real wildcard is the ECB

Casting those concerns aside for a moment, the real wildcard is the European Central Bank. The wisdom of hammering yields down in March was debatable. Continuing PEPP purchases at an accelerated rate beyond June will be harder to justify.

All hinges on whether the tightening of financial conditions – a fluffy concept to describe borrowing terms from sovereigns to households – is justified by the economic recovery. There are many ways to assess them, and the ECB has done a good job at muddying the waters.

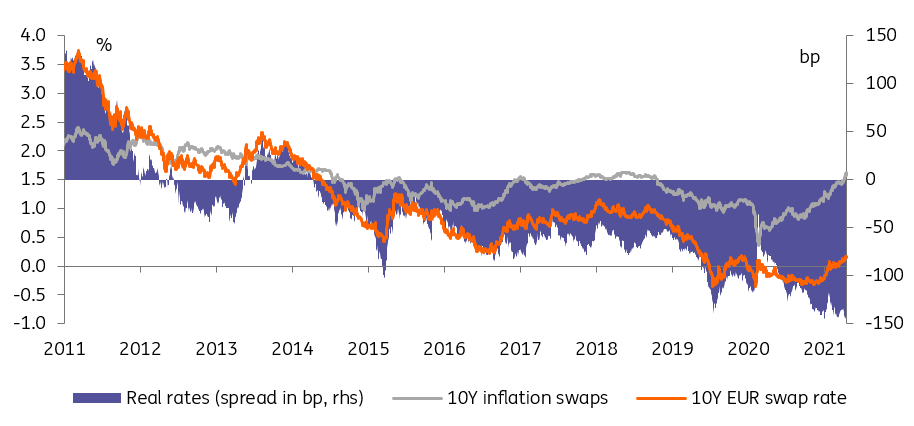

A few steps back: Real rates are as low as ever, hardly a case for more purchases

One way to measure this is by comparing nominal rates (bond yields and swap rates) to inflation expectations. By that, admittedly restrictive, measure, conditions are as easy as ever.

Real rates are consistent with an unjustifiable degree of macro angst

There is no doubt in our mind that the ECB has a much broader set of indicators at its disposal, some of which we will address in the next sections, but this one suggests the need for intervention is low.

Incidentally, it doubles up as a handy fair value indicator for rates. Where they are, real rates are consistent with an unjustifiable degree of macro angst. We conclude that there is little impediment to moderately higher Bund yields.