ING fokuserer på finanspolitikken i EU kontra pengepolitikken, dvs. regeringerne kontra ECB. Rentespændet mellem landene er faldet drastisk de seneste år, og med nul-renter er der grænser for, hvor meget centralbankerne kan gøre yderligere for at stimulere økonomien. ING mener, at de to valg i Tyskland og Frankrig i år og næste år vil sætte finanspolitikken mere i fokus, dvs. åbne op for større finanspolitisk stimuli end hidtil som med den nye EU-fond. Sagt med andre ord: Det bliver regeringerne, der fremover skal i arbejdstøjet, mere end centralbankerne.

Uddrag fra ING:

Rates Spark: excess of caution

Cautious price action, with a nervous eye on the stock market

Trading so far this week has been characterised by a cautious tone that has seen US Treasuries weaken after their early April rally, and stock markets retreat from all time highs. Central bank meetings, especially now that their presence in financial markets is so significant, is one of those rare times when correlation between the two asset classes, stocks and bonds, can stay positive.

Weak risk assets can coexist with rising yields

Whether warranted or not, there seems to be a degree of nervousness pervading rates markets about the valuation in some risk assets, including stocks and riskier bonds. This has provided a key justification for the stabilisation in USD rates after the Q1 rout.

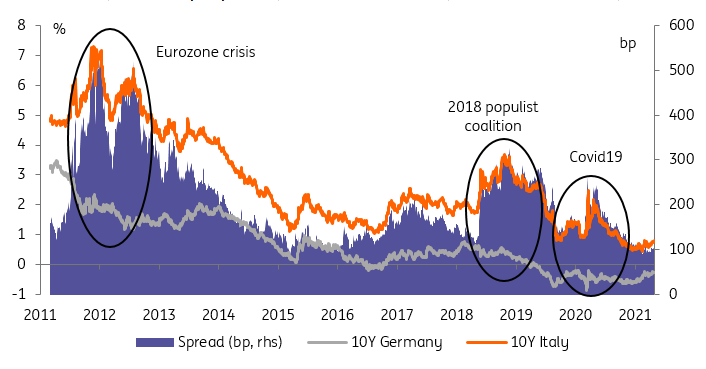

Eurozone: keeping the long-term picture in mind

April price action has been more in line with what one would expect in the Eurozone: nominal rates have kept on climbing steadily alongside stocks. This recent improvement in sentiment has its roots in the delayed start to the Eurozone recovery, and in particular to an acceleration in the EU’s vaccination drive in Q2.

Unfortunately, this return of optimism seems not to have benefitted peripheral bonds. Supply can be blamed for temporary pull-backs in spreads but the conclusion looking at price action in recent weeks is that a 10Y Italian bond is struggling to find demand when it yields less than 100bp over Bund.

Faster growth and fiscal stimulus would bring further yield convergence

It could also be that recent news about Italy’s recovery plan, most of which paid for by the EU recovery fund, but some self-financed, has shed light on further borrowing needs. We think this is misguided. Greater fiscal spending needs not be detrimental to a sovereign’s debt metrics, as long as it durably raises growth (a tall order admittedly).

Greater demand across the monetary union will chip away at the economic divergence between its members

More importantly in our view, it reflects a structural shift in the attitude towards fiscal spending that is shared at the European level. In time, greater demand across the monetary union will chip away at the economic divergence between its members, especially if it is handled at the EU level. The upcoming German and French elections should pave the way for such a shift.