ING har en omfattende analyse af de elektriske busser i Europa. Sidste år var der en fordobling af e-busserne, men nedgangen i den offentlige transport under coronakrisen har lagt en dæmper på udviklingen. Det kan få en langvarig effekt, men på sigt har e-busserne en god fremtid. Busser bruges mest i Øst-og Sydeuropa, men e-busserne har størst fremgang i Nordeuropa og Frankrig. Danmark hører til spidsen.

The buses of the future: another Covid-19 casualty

Electric buses are the future of public transport as many European countries decarbonise their economies. But the coronavirus crisis has dramatically impacted passenger numbers and given all this uncertainty, uptake is slowing

Investments are at stake

The Covid-19 pandemic has had a tremendous impact on European public bus transport. Passenger volumes dropped significantly and recovery to previous levels will take several years. As the crisis slashed ticket income and promises to change travelling behaviour, investments are at stake. This slows the transition to electric buses rather than speed it up.

Electrification of public buses was leading within heavy-duty vehicles in recent years. The EU’s fleet of battery-electric buses started accelerating from 2018 and it more than doubled to 3,500 in 2019, but growth remained limited to an extra 500 units to 4,000 in 2020 so far (of an estimated 190,000 in total). This shows Covid-19 is already impacting the transition and it’s with little doubt that this trend will continue in 2021.

All this comes at a time when all things electric are becoming increasingly attractive. Several countries have already adopted minimum targets for 2025 and the transition becomes even more important with the focus on clean air and plans to raise the CO2-reduction target to 55% in 2030.

The importance of bus transportation

*Excl. UK **YTD 17/11/20

2The public transport sector and its green ambitions for the fleet

Electric public buses are the future; new generation covers 90-95% of the lines

European countries are increasingly adopting the ambition to decarbonise the fleet, improve air quality and reduce emissions to zero. To reach this goal battery-electric buses (BEV) are most in focus.

The latest models of electric buses have a range of over 400km which covers probably 90-95% of urban area dominating European public bus connections. The purchasing price of battery-electric buses is still substantially higher than diesel buses (with € 400,000 – 500,000 against € 200,000 – 250,000) and charging infrastructure is required as well.

However, the operational cost of these buses is much lower as electricity is cheaper than diesel, less maintenance is required and the economic life will be longer. In combination with fast charging the new models, electric buses could already be competitively deployed (source: BNEF).

Battery-electric buses leading the zero emission charge rather than hydrogen

The question’s often raised as to whether hydrogen would be a viable option for public bus transportation. Given the moderate weight of passenger transport buses, the loss of energy in production and the usage of hydrogen and the relatively high total cost of ownership of fuel cell buses, we expect the battery-electric buses to be dominant at least until 2030.

Hydrogen might play a larger role in public transportation as well, but heavy users without alternatives, such as the chemical industry, are expected to benefit first when (green) hydrogen production goes up and prices drop. As soon as green hydrogen is abundantly available the trade-off between electricity and hydrogen might change.

3The size and composition of Europe’s bus fleet

Share of public buses higher in North-West European countries

The total rolling stock of buses over 3.5 tonnes in the EU adds up to roughly 770,000 units (2018). An estimated 190,000 (app. 25%) of these vehicles are qualified as public transport buses. The remainder is other (privately deployed) buses and coaches.

Southern and Eastern European countries such as Greece, Romania and Poland have relatively large and old fleets with a small fraction of public buses.

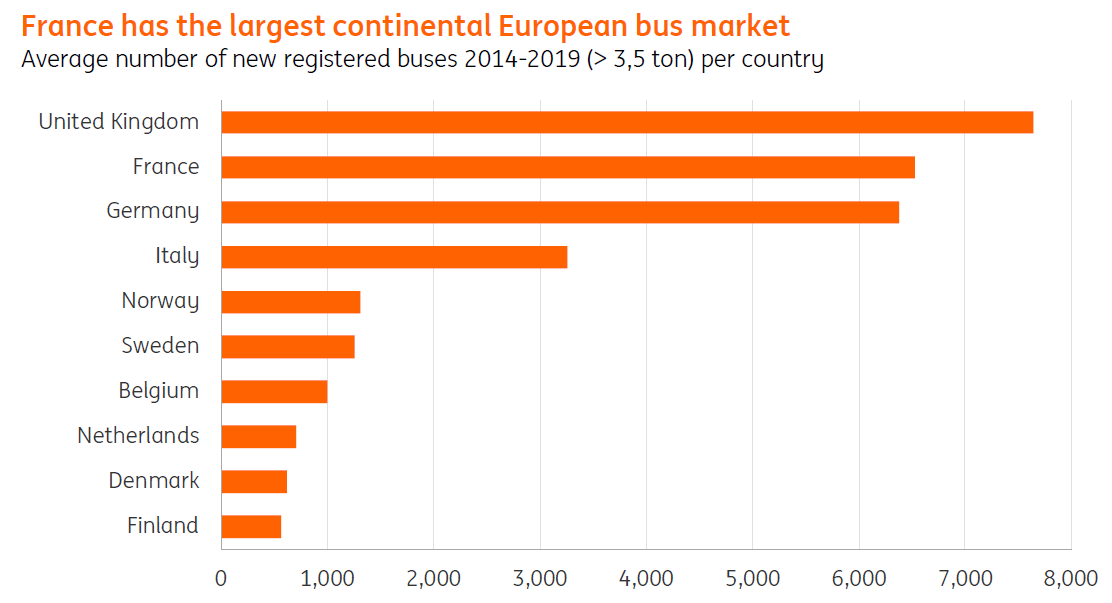

In-service public use in Belgium, the Netherlands and Sweden has a respective share of 48%, 51% and over 70% of the fleet. In new registrations, the portion of public transport buses is relatively high as public buses are intensively used and regularly replaced in concession cycles. The UK and France are the largest European markets for new buses.

The European bus market

4Where we stand on electrification

Electrification of public buses was gaining traction before Covid-19

Whereas China is the world leader in the electrification of buses in order to improve air quality in cities, in Europe this process just started five years ago. Just before the coronavirus crisis in 2019 the inflow of battery-electric buses accelerated and the total fleet more than doubled from 1,500 to 3,500, but that growth slowed to 4,000 in November 2020.

The Covid-19 effect on the electric bus fleet

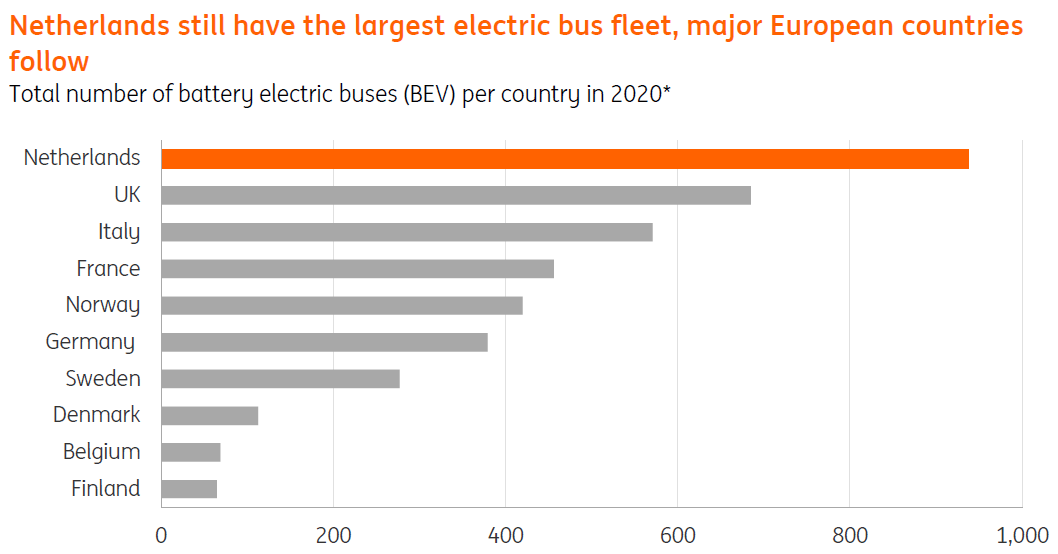

The Netherlands leads the way in Europe

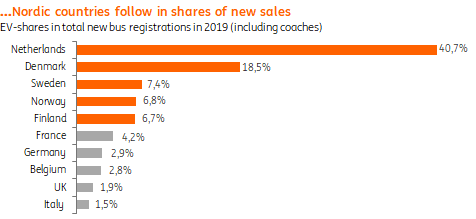

The Netherlands leads the way in the electrification of public buses following the ambition to meet the 100% zero-emission target for new registrations in 2025 and decarbonise the full fleet in 2030, In 2019 more than 40% of total new registrations were electric buses and with deliveries of pre-Covid ordered buses in 2020 it will probably hit 50%.

For public buses, this figure was only exceeded by Denmark in 2019 (by 60%) and other Scandinavian countries are also making good progress. In terms of the total number of electric buses, major countries like France, Germany and the UK will soon become the largest European markets.

Electrification in Europe; the Dutch lead the way…

…Nordic countries follow in new sales

Share of electric bus fleet

*YTD 22/11/20

5How Covid-19 has generally affected the public bus market?

Passenger numbers dropped dramatically following lockdown measures and changing travel behaviour

Public transport passenger volumes suffered heavily from lockdown measures. As people were discouraged to travel and advised to work from home if possible, they experienced a steep fall across Europe. In the Netherlands, for instance, passenger numbers dropped to initially a fifth of the 2019 levels in the first lock-down phase. In the UK bus passenger numbers showed in a similar way. Even in Sweden, which had a relatively mild lock-down, as well as Germany the impact was severe with a drop of 40-50%. During the summer there was some revival, but halfway this stagnated and fell back again during the second wave in the autumn.

6The fate of the fleet after Covid-19

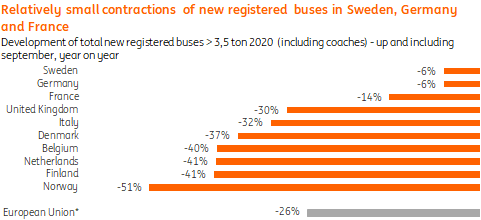

A significant drop in total new bus registrations in 2020

The Covid crisis generally leads to reduced investments in new buses. In the first 9 months of 2020, registrations of total new buses had already dropped by more than 25% compared to last year. Germany, Sweden and France showed the smallest drop. Given planning limitations, that effect will no doubt be exacerbated in 2021.

Development of total new registered buses

*Excl. UK

Uncertainty leads to postponement of investment and lower inflow of electric buses

Currently, there is much uncertainty about future passenger volumes and compensation for PTOs. This makes it difficult for PTOs to give their quotes on new concessions especially when new charging infrastructure is required. This is why various expiring concessions in 2021 and 2022 have been extended in the Netherlands and emergency concessions are implemented. In Denmark and Sweden running concessions have been extended as well.

Consequently, the pace of transition to electric buses will continue to slow as the inflow of new buses will be delayed. This will especially be true for countries where private companies own most of the fleet. In countries where most of the fleet is directly owned by companies linked to public transport authorities (PTAs), such as Belgium and Germany, this is less of an issue, although investment might still have to be reconsidered.

Manufacturers of electric buses face challenges while expected demand is delayed

For manufacturers of electric buses like VDL and Ebusco, delayed investment in electric buses will create serious challenges as orders are postponed and might be bundled in the years after. As various European countries already adopted minimum targets for 2025 and the green vehicle directive comes into force, we expect there will be a catch up prior to that. .