ING finder gårsdagens møde i ECB positivt. Der skete ingenting! Ifølge ING er det udtryk for, at rente-høgene i ECB ikke har fået vind i sejlene. Først i juni kan der komme nye signaler om den fremtidige udvikling. I mellemtiden bevæger den 10-årige tyske Bund-rente sig opad mod nul procent, og samtidig falder den 10-årige italienske rente. Rentespændet mellem de europæiske renter vil blive mindsket, og det skyldes primært den massive genopbygningsplan på 220 milliarder euro, som regeringschefen Mario Draghi har lagt frem. Han bliver storforbruger af EU-fonden.

Rates Spark: on the one hand…on the other hand…

ECB: avoiding the hawk trap

Despite facing a barrage of questions on the appropriate pace of PEPP purchases, president Christine Lagarde did a good job at keeping the ECB’s options open. Through her answers, we gleaned that there is no pre-determined monthly amount and that purchases are instead data dependent.

As our economics team has stressed, that question will be a lot more pressing at the June 10th meeting. In fact, there seems to have been no major display of dissent according to Reuters, probably more a reflection of the fact that no decision was taken yesterday rather than due to a newfound unity on the governing council. Hawks’ views are well known and we can expect them to grow louder in the run-up to June.

Those looking for signs of optimism were satisfied, but so were those looking for prudent communication. In Lagarde’s own words, this proved a ‘on the one hand…on the other hand’ meeting. The ECB successfully walked that tightrope. The upshot for rates is twofold. The lack of communication accident and of policy signal leave the market free to gradually price the recovery, by converging to 0% in the case of 10Y Bund. We also think it clears the way for further tightening of peripheral spreads.

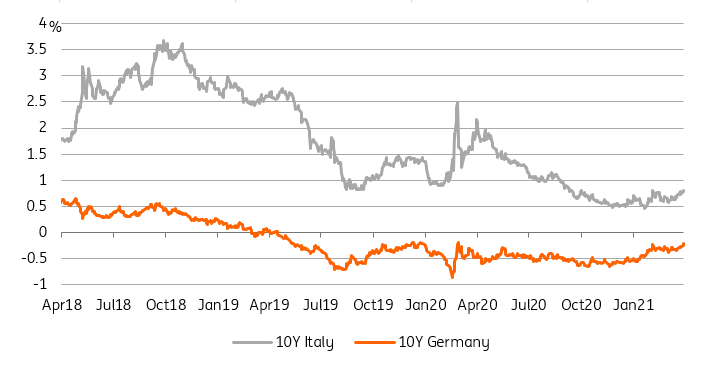

More yield convergence is in the cards between Italy and Germany

Italy: riding the Draghi wave

In addition to a peaceful ECB meeting, this week has renewed our conviction that peripheral spreads are due for another leg of tightening. The German constitutional court has paved the way for the ratification of the EU recovery fund.

This is not the last bump on the road for the embattled fiscal tool but it removes a tail risk that sat uncomfortably with our bullish Italian debt call. Draghi’s government has also published its €220bn recovery plan which he intends to accompany with much discussed structural reforms to boost Italy’s competitiveness. We do not expect S&P to modify Italy’s rating tonight but its assessment on Draghi’s plan could a shot in the arm for Italian confidence.

This week has also shed light on a political development that, in time, might shrink the spread between Italian and German government bonds: the rise of the German Green party ahead of September’s federal election.

As the EU recovery fund saga best illustrates, changes at the EU level tend to play out over long timeframes, but a staunchly pro-EU integration party as part of a governing coalition would greatly reduce the perceived risk of Eurozone breakup, one of the main reasons why 10Y Italian bonds trade 100bp above their German counterpart. We renew our call for this spread to sink to 75bp in the coming months.