ING har analyseret fire scenarier for, hvordan markedet vil reagere på Bank of Englands beslutning torsdag om en rentestigning. ING venter en stigning på 50 basispunkter, men en mindre stigning kan ikke udelukkes, da markedets reaktion er skiftet fra frygt for inflation til frygt for recession. Det kan føre til en renteudvikling på de 10-årige statsobligatiobner på mellem 1,75 pct. og 2 pct., og en sådan beslutning løser ikke de store problemer i England.

Bank of England: Four scenarios for markets this Thursday

Four scenarios for the Bank of England this Thursday

Rate hike size

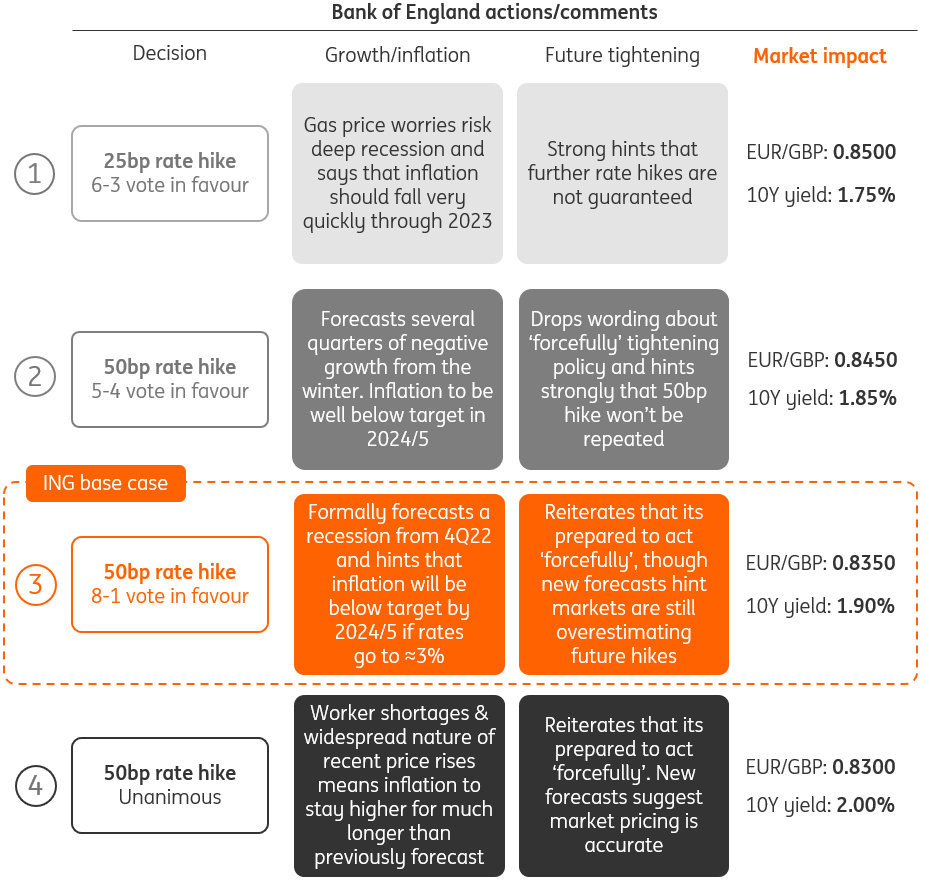

The Bank of England announces its latest decision this Thursday, and a 50bp hike looks highly likely now, especially given recent comments from Governor Andrew Bailey a couple of weeks ago that specifically put a hike of this size on the table.

Admittedly, there’s a chance we simply get another 25bp move, given there’s not much in the recent economic data flow to suggest the BoE needs to move more aggressively than it did in June. But concerns among hawkish committee members about job market tightness and a weaker pound point to a larger move this week – especially given that this is what markets are pricing.

Vote split

In June, the committee voted 6-3 in favour of a 25bp hike. That suggests a decision to hike more aggressively won’t be unanimous this week, and we’d expect at least one official (Silvana Tenreyro), perhaps two (Jon Cunliffe) to vote for a smaller move. But assuming Governor Bailey votes for 50bp, then we’d expect others to follow suit, generating a majority in favour.

Forward guidance/signals

We’ve argued that the Bank is probably nearing the end of its tightening cycle. But even if that’s the prevailing view on the committee, we doubt they will say so this week. Partly that’s just because everything is so uncertain right now. But also because the hawks in particular won’t want to see UK-US rate differentials widen materially at this stage, amid concerns about adding to recent sterling weakness. We therefore think the Bank will repeat its guidance that it’s prepared to act ‘forcefully’ where needed.

Nevertheless, expect the Bank to hint that market pricing on the path of rate hikes is still too aggressive. Back in May, the Bank’s projections showed unemployment rising by almost two percentage points and inflation below target in a couple of years’ time, if they were to implement the rate hikes markets were pricing. Investors had been expecting Bank Rate to go even higher than they did back then, though they’ve noticeably pared back expectations for the peak from 3.5% to 2.8% over recent weeks. Assuming the new forecasts show a similar pattern to May’s, then this should be read as a subtle but important signal that markets will need to pare back interest rate expectations further.

Our view

Beyond August, we’ve been pencilling in another 25bp hike in September, before a pause, though we accept this may be a slight underestimate. We highlighted last week that persistent worker shortages, as well as potential tax cuts depending on the result of the Conservative leadership contest, could ultimately see the Bank deliver another 25-50bp on top of what we’ve been forecasting.

Quantitative tightening

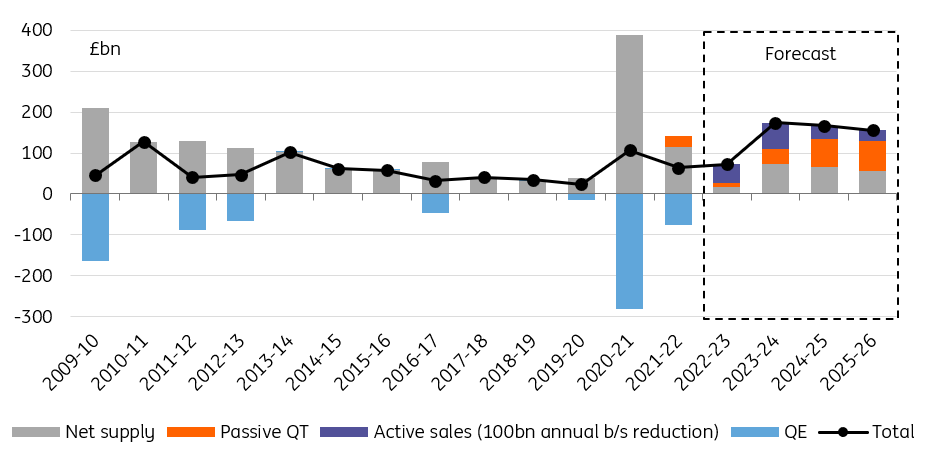

Governor Bailey has confirmed the Bank will offer fresh details this week on its plans to actively sell government bonds, a move that would accelerate the BoE’s balance sheet reduction (or quantitative tightening). Bailey suggested it could amount to £50-100bn a year (passive reduction and active sales) in the first year. Look out for operational details on how these sales might be conducted, be it by Bank of England auctions (effectively the reverse of how it conducted QE) or through the Debt Management Office.

But here’s the crucial detail: what would it take for the Bank to pause its QT programme? Bailey has hinted in the past it wouldn’t sell gilts in market turmoil, but will the BoE set out some more formal triggers for stopping sales? Arguably policymakers would rather keep it vague, though there’s a trade-off between this and keeping the policy predictable for markets. Incidentally, current market conditions mean now isn’t an ideal time to start selling, though the Bank may hint it is willing to start in September.

Market rates: Downside risk dominates

It is now a well-accepted fact that the focus in financial markets has dramatically shifted from inflation to recession fears. This was first visible in the aggressive flattening, and indeed inversion, of the sterling yield curve. Outright yields falling further from their June peak is the more recent and dramatic manifestation of where investors’ worries lie. In the case of 10Y gilts, this has meant crossing under the symbolic 2% level, 80bp from their peak.

Yet, we see more downside to yields over the coming weeks and months. For one thing, the Sonia swap curve is still pricing the Bank Rate peaking more than 75bp above where we are forecasting it. What’s more, global growth concerns are driving more money into the safety of government bonds. Taken together, 10Y gilts may well flirt with 1.5% over the summer months, a level not touched since March.

Private investors are set to absorb a record amount of gilts in the coming years

A key risk to this view is indeed the effect of QT, and in particular of gilt sales, on valuations. Fundamentally, active sales should be treated the same way as passive balance sheet reduction in that the latter should result in commensurate debt sales from the Debt Management Office. Assuming £100bn of annual balance sheet reduction, the total increase of gilts in circulation in the next three fiscal years will reach record levels (even if our supply forecast could well turn out to be too optimistic).

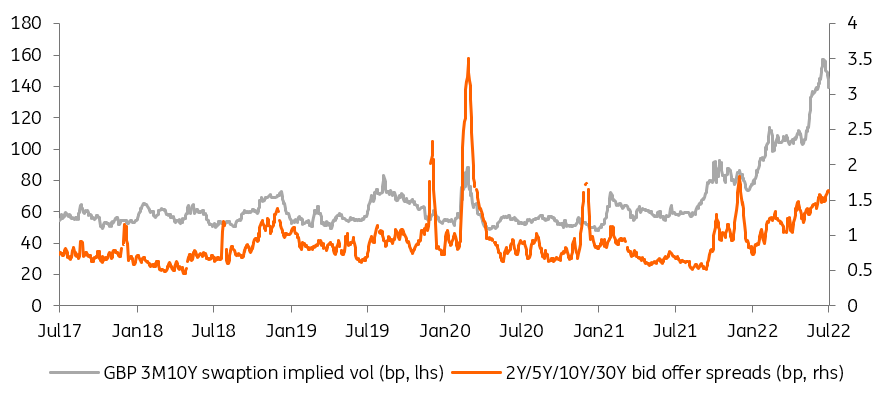

Outright sales add a financial stability element to the debate about the amount of additional gilts that private investors can absorb. The impact is difficult to quantify as the greatest impact of QE is, by the BoE’s own admission, greater when markets are in a period of stress. Judging by elevated levels of implied volatility, and by the width of bid-offer spreads on gilt benchmarks, the current period shares some of the stressed characteristics of the onset of the Covid-19 crisis in the spring of 2020, when the BoE decided to embark on an unprecedented amount of purchases to restore market conditions. In short, now doesn’t seem like an opportune time to add to market stress.

The gilt market displays the same stressed characteristics as in the spring of 2020

FX: BoE will struggle to lift the pound

The monetary policy channel has not been the primary driver of EUR/GBP lately, according to our short-term fair value model, where risk sentiment explains a larger portion of daily swings in the pair. The fact that markets are almost fully pricing in a 50bp hike this week and around 100bp of extra tightening after that by February 2023, in our view shows that a good deal of BoE hawkishness is already in the price when it comes to the pound.

An already volatile FX environment suggests the pound could show sharp moves in either direction after the BoE announcement this week. But the risks related to a dovish repricing in the BoE curve continue to highlight the net monetary policy impact for the pound over the coming months should be largely negative, if anything.

With the dollar potentially finding some stability this week, GBP/USD may start stalling around the 1.2300 level. When it comes to EUR/GBP – despite the lingering downside risks related to a full shutdown of gas supplies from Russia – we could see the 0.8400 work as a gravity line for now, with some potential BoE dovish repricing favouring a return to 0.8500.