Forbrugertilliden er faldet kraftigt i USA, med 14,6 til 91,5 point i Conference Boards indeks over forventningerne. Risikoen for en nedskæring af støtten til fyrede vil svækket forbruget, og ING venter et fald i forbruget i august. Der har været forventninger om, at tredje kvartal vil vise et økonomisk opsving, men det er i dag langt fra sikkert. Opsvinget ventes at blive langvarigt og vanskeligt.

US: Confidence takes a hit

Plunging consumer expectations reflect anxiety over a pick-up in Covid-19 cases, reversal of reopening strategies and worries over the financial implications of the conclusion of the $600 a week Federal unemployment payment. It reinforces our fears of negative consumer spending/retail sales in August

Things had been going so well…

The Conference Board measure of consumer confidence has fallen more than expected to 92.6 from 98.3 (consensus 95.0). The details show the present situation index actually rose to 94.2 from 86.7, but the far more important expectations component plunged 14.6 points to 91.5, casting further doubt on how vigorous the economic recovery will be in the third quarter.

To explain the rise in the present conditions component we can point to the fact that stock prices are virtually back at the highs of February and the Nasdaq is well above. This positive wealth effect is a key factor explaining why overall confidence has proved to be far more resilient than in previous recessions.

The expansion of unemployment benefits has also helped with the $600 a week Federal boost meaning the majority of recipients have higher incomes than when they were working. The CARES Act also included legislation that eased fears of foreclosure and eviction, which has also helped to support overall confidence.

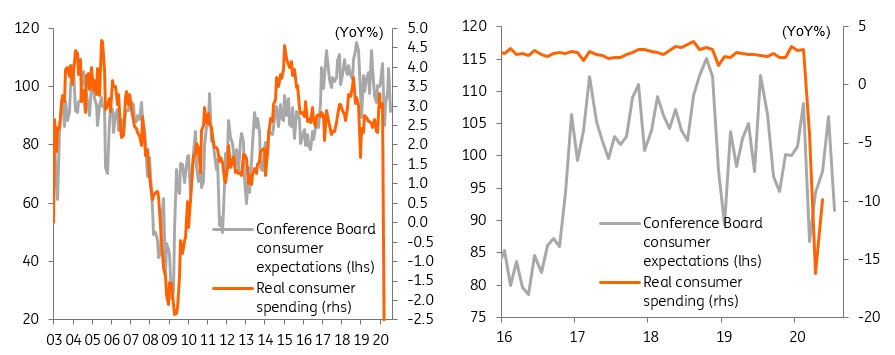

Confidence & spending: Relationship breakdown

But the consumer is facing renewed challenges

Consumer spending has historically been better correlated with the expectations component and this is the series we should really focus on. The expectations component has also proved to be incredibly resilient for the same reasons as the present situation, but spending took a massive hit due to enforced closures relating to Covid-19 containment measures. So even if households felt happy to spend, they couldn’t physically do it.

Today’s report seems to suggest we are in the second stage of the crisis. The spike in Covid-19 cases is leading to state Governors taking the decision to reverse course on the reopening plans, which is shuttering businesses and leading to another wave of job losses. At the same time, the implications for the health of the population is seemingly making households a little more anxious. Then there is the ending of the $600 a week Federal boost to unemployment benefits, which is going to make the 30 million people who had been receiving it very worried.

Recovery is a long and bumpy road

Indeed, states that are experiencing the biggest resurgence of Covid-19 were the states that saw the biggest declines in confidence. For example, California expectations fell 25 points, Texas fell 32 points, Florida fell 27 points and Michigan fell 53.3 points! In contrast, New York saw a RISE in expectations given the rapid fall in cases in the state.

Taking this altogether, the return of economic dislocations from Covid-19 makes us increasingly cautious on the prospects for the 3Q economic revival. Currently, the consensus for July non-farm payrolls (7 August release) is for a gain of two million. We think this looks optimistic given the high frequency jobs newsflow from Homebase and the reversal of state reopenings and wouldn’t rule out a negative reading. We are even more nervous about the prospect for retail sales and consumer spending in August given the declines in income from the cuts to unemployment benefits for 30 million people. The recovery is going to be a bumpy ride.