ING skriver i en analyse af det amerikanske valg, at udfaldet vil få stor betydning for Europa. Hvis Biden vinder, vil der blive mere normale relationer uden sanktioner og handelstariffer mod Europa, men der vil stadig være rester af “America First” under Joe Biden. Men selv under Trump har Europa klaret sig godt med øget handelsoverskud og flere europæiske investeringer i USA end i den modsatte retning. Under Biden bliver det lettere at nå en aftale med Europa om beskatning af digitale selskaber.

US Elections: What’s in it for Europe?

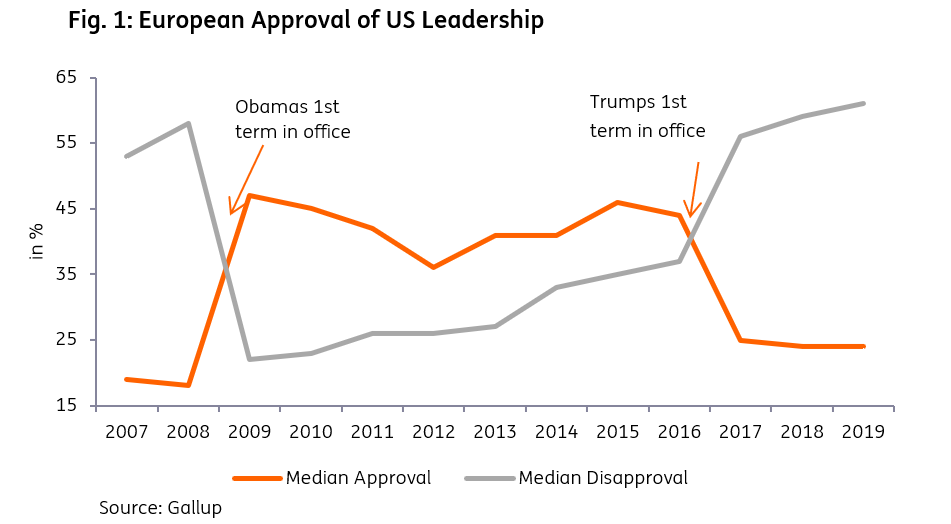

Status quo of the cracked relationship between the EU and the US

When thinking about what has recently defined the relationship between the EU and the US, two things immediately come to mind: tariffs and sanctions. The “America First” policy, applied by President Trump in order to tackle the US current account deficit, has challenged many economies over the last four years.

Before Trump moved into the White House, the US had been a reliable partner in trade and foreign policy. This included, among others, fighting terrorism and cooperation in safety and energy.

European surplus in goods trade

The US has been running a trade deficit with the EU since 1994. In fact, the deficit in goods trade with the EU has increased more than tenfold from $17 billion in 1997 to $178.5 billion in 2019, while the services trade balance has been in surplus since the recording started in 2003.

During Trump’s term in office, European exports to the US have increased by 23.7%, while US exports to the EU increased by 24.9%.

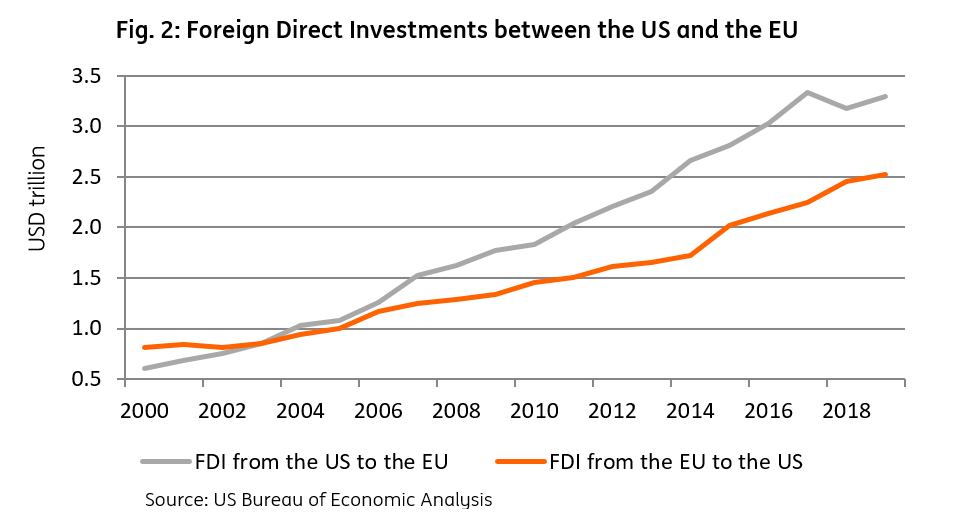

Foreign direct investment from the US to the EU has been lower under the Trump administration than in the past. When Donald Trump entered office, the stock of US FDI in the EU was $3.3 trillion. In 2018, this stock had dropped to $3.2 trillion.

At the same time and maybe even triggered by the trade war, European direct investment in the US increased from $2.0 trillion in 2015 to $2.5 trillion in 2019.

Trade frictions and tariffs

Shortly before Trump moved into the White House in January 2017, the US and EU agreed on a deal under the Transatlantic Trade and Investment Partnership Agreement (TTIP), which included the removal of 97% of tariffs. The US wished to remove 100% of tariff lines, whereas the EU wanted to keep tariffs on sensitive agricultural products.

A free trade agreement between the EU and US would have seen EU exports to the US rise by 27% while US exports to the EU would have increased by 37.5%. However, the Trump administration did not continue with the negotiations.

Instead, Trump took a different approach, imposing tariffs in June 2018, with steel (25%) and aluminum (10%) in the firing line. The administration has frequently threatened to impose tariffs on European cars and car parts but up to now, these threats have not become reality.

This means that currently – despite the tough talk – the only tariffs that Trump has imposed or increased on European goods are the ones on steel and aluminium and on Europe-made goods like e.g. Scottish Whiskey, Italian Pecorino or Dutch Edam cheese. Some of these latter tariffs were in line with the WTO ruling on Boeing and Airbus.

Back in 2016, average US tariffs on EU agricultural goods and non-agricultural goods amounted to 6.8% and 3.9%, respectively. In 2018, these tariffs had risen to 7.2% and 4.0%, respectively.

For Chinese agricultural products, average US tariffs went from 4.2% in 2016 to 4.3% two years later while tariffs on non-agricultural products rose to 4.1% from 4.0%.

This is far lower than countries like Guatemala, where average US tariffs imposed on agricultural products amounted to 8.4% in 2018, but at the same time, it is much more than Iceland, for example, where average US tariffs on agricultural products amounted to just 2% in 2018. Unfortunately, there is hardly any reliable data available for 2019.

Trade in Energy and Nord Stream 2

In addtion to tariffs on goods, the Trump administration also made keen use of sanctions to impose its economic will. The last 150km of Nord Stream 2, the gas pipeline from Russia to Germany, is a case in point.

In recent years, the US has become the EU’s main supplier of liquefied natural gas (LNG). The share of gas imported from the US was 16% in 2019, up from 6% and 4% in 2018 and 2017, respectively.

The EU needs to import 70% of its total LNG demand. In order to diversify its energy imports and ensure the security of supply, the EU looked to increase gas imports from Russia, a move which sparked a geopolitical row.

After the Trump administration threatened to impose sanctions on companies financing the project, the Nord Stream 2 project was halted last year. On the US side, this was justified by the Countering America´s Adverseries through Sanctions Act (CAATSA), effective since 2017.

At the same time, the Trump administration has been retreating from the world stage while attempting to dismantle the rules-based global order.

Trump has terminated the US relationship with the World Health Organization, arguing that it was responsible for the spread and development of Covid-19. And he has blocked the nomination of judges in the World Trade Organization’s arbitration court. In short, global tensions have risen, trust has been lost and the EU has been caught in the crossfire.

What Europe should expect from the next US president?

Will things change if Trump is re-elected in November? His campaign slogans ‘Keep America Great‘ and ‘Promises Made, Promises Kept‘ point to a second term in office without any deviation from the current path of policy.

Even though Europe probably wouldn’t be the main focus of Trump’s second term in office, the threat of tariffs and sanctions on European goods and manufacturers would stay with Europe for another four years.

Europe would also have to become more independent and probably also more opportunistic in the geopolitical race between the US and China.

If Republicans were to lose their majority in Congress, Trump could become even more active in the area of trade, as foreign policy would remain one of the few exclusive presidential responsibilities.

In theory, a second Trump administration could try to work together with the EU to address joint concerns over China but comments from the current administration over the last few years suggest this is not a preferred tactic.

A win by Joe Biden, on the other hand, could portend a more conciliatory approach though a complete U-turn on all of the Trump-era policies seems unlikely. Here are some of the ways in which we think a Biden administration could impact Europe:

- On trade, don’t expect a significant shift. Traditionally, the Democrats have been less supportive of free trade than Republicans. The race on tech should continue, putting further strain on global trade and particularly, relations with China.

- However, a Biden administration is likely to invest more in the transatlantic relationship, in a bid to make Europe an ally. Biden seems unlikely to use tariffs as a policy instrument. Even if trade relations improve under Biden, US pressure on Europe to increase defence spending will remain. In this regard, it is interesting that the WTO very recently ruled in favour of the EU in the Boeing-Airbus dispute, although the EU has announced that it will wait until after the US election before imposing any measures.

- Related to trade is Brexit. Here, the outcome of the US elections could have an impact on the current cumbersome negotiations between the UK and the EU. If Trump retains the presidency, he might try to get a UK trade deal agreed, to the detriment of Europe. Conversely, Biden’s Irish roots make things more challenging for the UK and could therefore push the UK to sign up to the EU’s demands.

- On regulation and taxation, a Biden administration could bring the US closer to Europe when it comes to financial regulation. And it might go back to the negotiating table with other OECD countries to amend taxation rules for digital companies. If, under a common agreement on digital regulation, the EU abandons the national digital services tax for US companies, the US would drop the Section 301 investigations.

- Although Joe Biden thinks that Nord Stream 2 is “a bad deal for Europe”, it is possible that he won’t be as strict as Trump on this issue as he seeks to rebuild relationships with Europe, and Germany in particular. However, he might want something in return. If Europe’s reliance on Russian gas increases, the US may demand broader access to gas markets in Europe at the expense of Russia.

- There could also be positive spillovers for Europe from what may look like US domestic issues: a big infrastructure programme, more investment to tackle climate change and 5G. Under a Biden administration, European global players are more likely to benefit from these domestic US investments than under a second term for Trump.

- Planned tax increases by the Biden administration are unlikely to have a major impact on FDI from Europe to the US, which has always been high. Even with higher taxes, we do not see a contraction of European company earnings. Taxes could be higher but not as high as they were before Trump took office while conditions for foreign trade should improve.

Europe may not have a say in the coming presidential election but it does have a stake in the outcome. A re-election for Trump suggests a continuation of the status quo while a change in the Oval Office could usher in a new period of US-EU relations. Under either scenario, however, Trump’s legacy will likely live on, with “America First” still at the heart of future foreign policy.