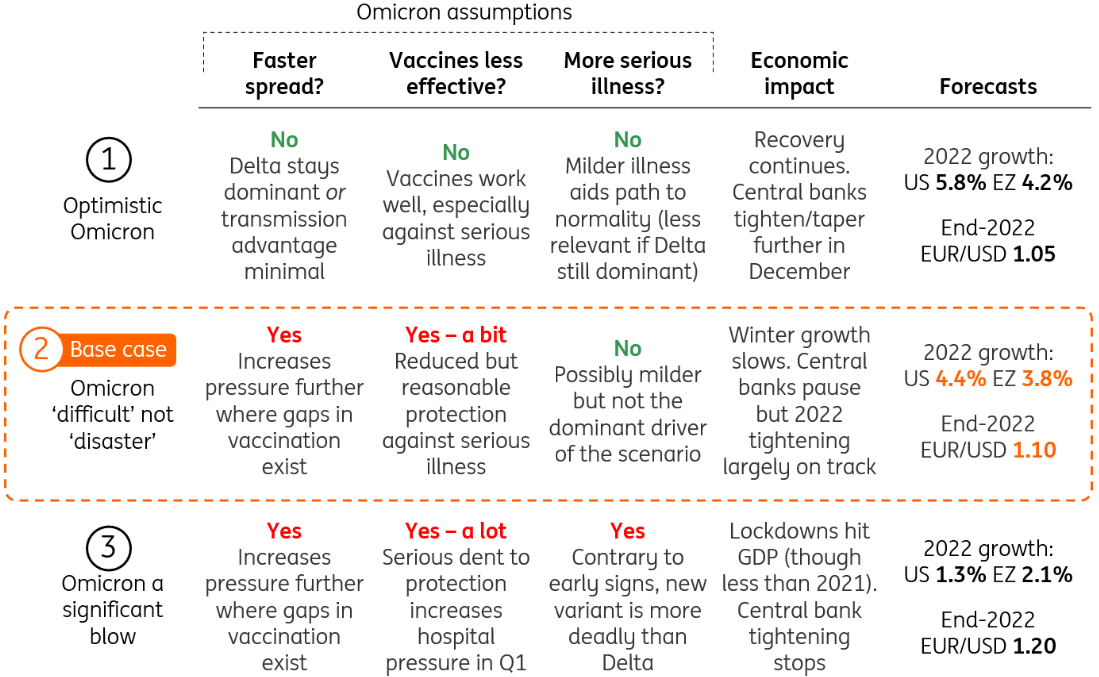

ING har udarbejdet tre scenarier for den virkning, som Omicron kan have på økonomien. I det gode scenarie vil økonomien ikke blive påvirket særlig meget, og USA vil have en væsentlig højere vækst end Europa. Hvis Omicron vil ramme hårdere, uden at blive en katastrofe, vil væksten blive reduceret med omkring et procentpoint i USA og Europa, dog mest i USA. Det skyldes, at vaccinationerne er mere udbredte i Europa end i USA, og desuden er Europa længere fremme med barske restriktioner. I det værste tilfælde, hvor det viser sig, at de nuværende vacciner ikke har nogen særlig god virkning mod Omicron, vil væksten falde dramatisk til mellem 1 og 2 pct. i USA og Europa, for så bliver lockdowns nødvendige igen – i hvert fald i begyndelsen af 2022.

Three Omicron scenarios for the global economy

Very little is known about the new Omicron variant, at the time of writing. Data is scarce, but we know what happens next depends heavily on two key questions. First, is the virus more transmissible, as some early reports have hinted? And second – perhaps more importantly for the economic outlook at least – how resistant is the new variant to vaccines and pre-existing immunity?

We’ve mapped out three scenarios based on the answers to those questions.

Three Omicron scenarios for the global economy

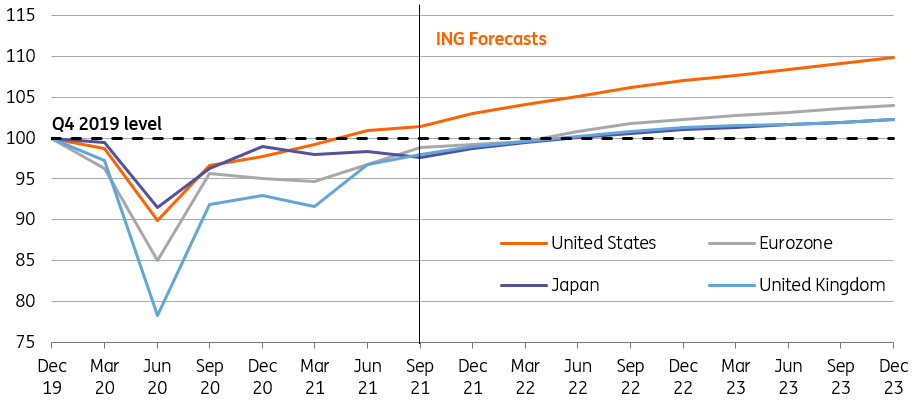

Scenario 1: Optimistic Omicron

Omicron proves to be a ‘storm in a teacup’. Either that’s because it can’t gain a foothold over Delta – something we saw with the Beta variant earlier in the year – or indeed because it lowers the threat level of Covid-19 by lowering the chances of severe disease.

This looks similar to our previous base case, and here central banks press on with their tightening plans. The Federal Reserve accelerates its taper in December and gears up for three rate hikes in 2022. Sporadic Delta lockdowns slow eurozone growth over Christmas and early into the new year, but the situation improves through the spring. The European Central Bank begins to taper amid growing wariness about inflation. The Bank of England kicks off its rate hike cycle this month.

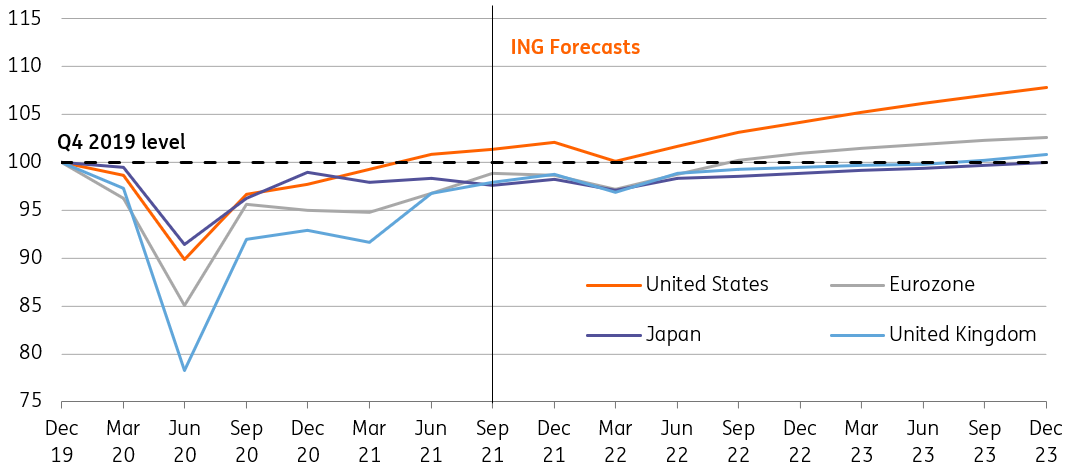

Scenario 1 – Level of real GDP (Q419 = 100)

Scenario 2: Omicron ‘difficult’ but not a ‘disaster’

This is loosely our base case. It assumes that early signs are correct that Omicron has a transmission advantage. That means a greater share of the population needs immunity to keep the virus under control. In practice, this threshold was already very high under Delta, but countries with lower vaccine take-up in vulnerable groups face a greater challenge.

Vaccine efficacy also takes a hit, though as we saw with the Delta variant, the current jabs still provide strong (if reduced) protection against severe disease, even if they’re much less likely to stop you from getting Covid altogether.

For the world economy, experience from the Delta wave last summer offers some clues. Omicron doesn’t help Europe at a time of spiking cases and offers more justification for more aggressive action in the run-up to Christmas.

But high vaccine rates and the arrival of boosters mean the continent (including the UK) comes off more lightly than other parts of the world. Consumer ‘virus confidence’ (eg appetite for socialising) need not take a permanent hit assuming vaccines still offer some reasonable protection.

The effect might be slightly more noticeable in the US, even if the bar for lockdowns is much higher. Lower vaccine rates (notably among vulnerable groups) could mean that confidence slips and activity levels take a hit, as we saw with Delta. Meanwhile, in Asia, Omicron stalls the move away from zero-Covid, especially in China. The recovery of supply chains is further delayed.

Central banks are likely to ‘wait and see’ in December, not least because it may be weeks before we know what we’re dealing with. But inflation remains front and centre, so we should still expect some tightening of monetary policy next year.

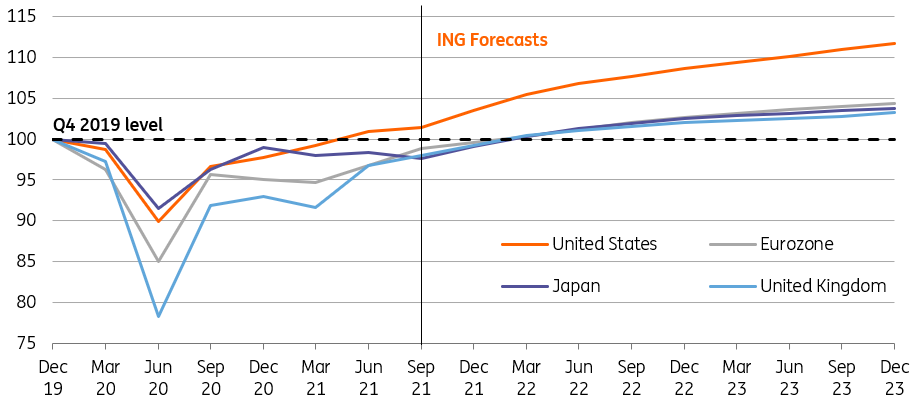

Scenario 2 – Level of real GDP (Q419 = 100)

Scenario 3 – Omicron deals significant blow to the recovery

This is the scenario markets were first worried about when the Omicron news first broke. Vaccines are significantly worse at stopping severe disease, making Europe and the US especially vulnerable to a fresh increase in hospitalisations, versus our other scenarios. We’re also assuming Omicron ends up being more deadly too.

Countries that have relied most heavily on vaccines so far tighten restrictions. Europe returns to lockdowns in the first quarter, as do parts of the US.

That said, the economic hit is unlikely to be quite as bad as last winter. Most scientists agree that the current vaccines will still do something, even if considerably less than against Delta. And we know with reasonable certainty that a new vaccine can be made, albeit not rolled out much before the summer in large numbers. New anti-viral treatments will help too.

Protests in Europe also hint at some ‘virus fatigue’, making it politically challenging for governments to maintain strict restrictions for as long as last year. The second wave in early 2021 also showed that businesses are more geared up for tighter restrictions than when Covid first arrived. This is probably even more true now.

In short, we expect a dip in first-quarter GDP in the major developed economies, albeit not as deep as in early-2021. But the subsequent recovery could be gradual. A vaccine-resistant Omicron acts as a wake-up call that without more widespread vaccine manufacturing capability, future variants could deliver similar blows in subsequent winters.

Firms begin to factor this into their business decisions, limiting their appetite to invest. Consumers look to keep savings levels higher, in anticipation of future turbulence. Overall growth momentum proves more lacklustre through 2022, compared to the rapid rebounds we saw in Q2/3 2021.

Scenario 3 – Level of real GDP (Q419 = 100)