ING ser tydelige tegn på, at inflationsforventningerne er blevet tæmmet, og det har lagt en dæmper på renteudviklingen. Den 10-årige amerikanske renter ligger på ca. 1,75 pct. Markedet er påvirket af den geopolitiske spænding omkring Ukraine, men det afgørende er, at der er blevet lagt bånd på inflationen, og det skyldes de barske udtalelser fra Forbundsbanken den seneste tid. Banken mødes i morgen og torsdag.

Rates Spark: Real rates hold up

Geopolitical tensions are causing yield curves to bull-flatten, and doubts about the Fed put are pushing more investors into the relative safety of bonds. This looks a temporary move but one that could continue into the FOMC. The risk of verbal intervention against overly low long-end rates is rising.

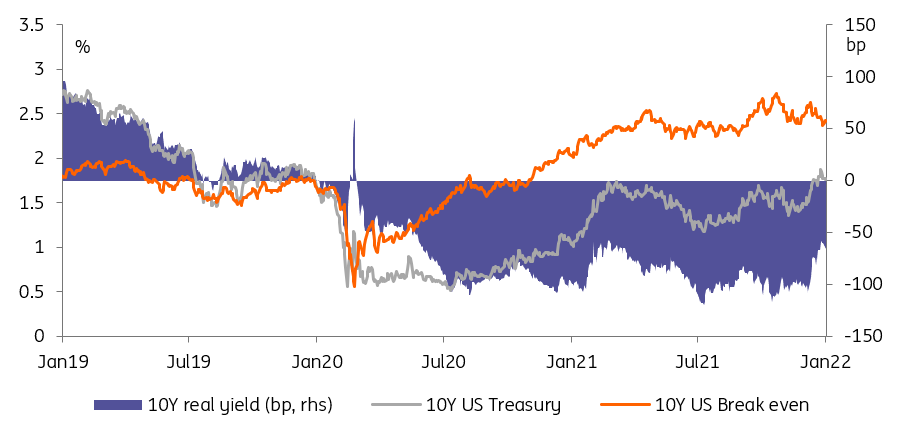

Market rates are well below their highs, but real rates are still well up

The 10yr yield is clearly well off the highs seen earlier in the week, having slipped to the 1.75% area. Drivers here have been: 1. Pause after a previous impressive upmove, 2. Risk-off, partly driven by higher rates, and 3. Ukraine tensions (in part). Reasonable foreign demand at recent auctions has also helped, and there has been no panic selling.

A key wrinkle to be aware of is that the move lower in yields appears to be mainly due to falls in inflation expectations. The 10yr inflation expectation is now at 2.35%, 30-40bp down from the 2.65%-2.75% area seen in Nov/Dec 2021. Tough tightening talk from the Fed is at the root of this. That said, the2.40% level we’re at right now is in fact not that elevated any more. It discounts inflation of a little over 2% plus a 30bp premium, practically back to neutral.

Higher US real rates continue to be a worry

Real rates have hardly fallen at all. The 10yr real rate is up 50bp since the beginning of the year, and in the past week or so where nominal rates have moved well off prior highs, real rates are holding on to highs. They remain deeply negative, with the 10yr at -65bp, but still holding up quite well.

So what does this all mean? First, inflation expectations are being tamed. The Fed has in fact done nothing so far apart from talking, but has managed to get some decent verbal tightening in. Second, the journey for real rates is still up, despite the fall in nominal rates.

Inflation expectations are being tamed

Inflation expectations in the 10yr are likely to hit a roadblock between here and 2.25%, which should limit the pull lower coming from this. But there is no such roadblock for real rates, with the 10yr still 60bp away from zero. Ahead, if real rates continue on their journey towards a non-negative state, this should begin to dominate, ultimately pushing nominal rates back up.

Opportunity for the Fed to shape the conversation on Wednesday

The downdraft in global stock markets, on the back of geopolitical tensions and Fed tightening worries, remains the main driver of government bonds this week. None of these are valid long-term drivers for a rates forecast, but we think they will continue to push yields down in the near-term.

Barring a surprise de-escalation, the next flashpoint for markets will be Wednesday’s Fed meeting. The central bank has a track record of stepping back from the brink when under pressure from risk assets, the famous “Fed put”.

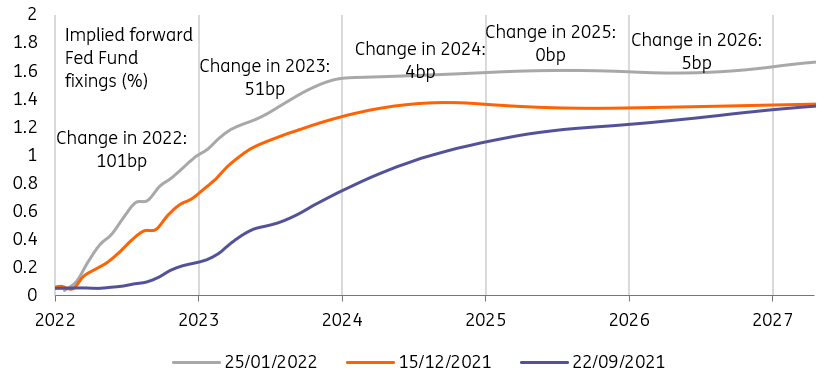

The US curve has barely tempered its Fed hike expectations for this year

It is debatable how much the Fed put applies here

It is debatable how much the Fed put applies here. The situation in Eastern Europe is far from the Fed’s main area of concern, and it is unclear whether stubbornly high inflation would allow it to operate another U-turn, 2018-style. Interestingly, markets do not seem overly confident that the Fed will ride to the rescue, at least judging from the USD swap curve still pricing four 25bp hikes this year.

This is the fear gripping financial markets currently, and investors will only get the beginning of an answer tomorrow. Between now and then, we struggle to see what could give markets reasons for optimism.

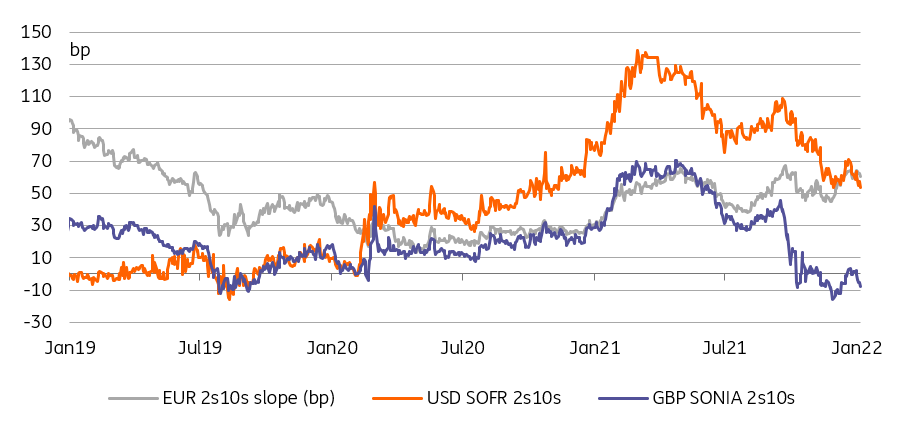

The US curve-flattening may run counter to the Fed’s tightening objective

The anatomy of the risk-off move is interesting too. Yield curves have generally bull-flattened as one might expect in a bout of risk-off. Naturally, this flattening goes against our macro view, but also against the Fed’s perceived aim to prevent a flattening of the yield curve as it tightens policy. It is well understood that this curve-flattening may be temporary but it may still prompt a verbal response from the Fed.

Today’s events and market view

Barring a surprise breakthrough in talks with Russia, we expect investors to continue to shun risk assets, and to prefer safe havens instead. This has the potential to extend the government bond rally that started in the middle of last week. This is no change to our bearish macro view on bonds, but it looks like there are too many headwinds on the way to higher yields for the time being.

Supply is relatively light this week, although France has mandated banks for the launch of a new 30Y inflation-linked bond. Aside from this deal, the Netherlands will auction 30Y debt. The US Treasury will also sell 2Y notes.