ECB-chefen Lagarde må bruge alle sine diplomatiske evner på rådsmødet i dag for at afbalancere duerne og høgene i rådet, mener ING. Høgene, der vil standse den meget lempelige pengepolitik, har skærpet tonen den seneste tid i takt med den stigende inflation. ING venter, at Christine Lagarde vil sige, at en høj inflation måske bliver af mere vedvarende karakter, men at hun vil indtage en neutral holdning og holde optioner åbne for pengepolitikken. ING venter, at den holdning betyder, at euroens kurs over for dollaren stort set forbliver uændret i den nærmeste tid.

EUR and ECB Crib Sheet: Lagarde’s diplomacy may leave euro unsupported

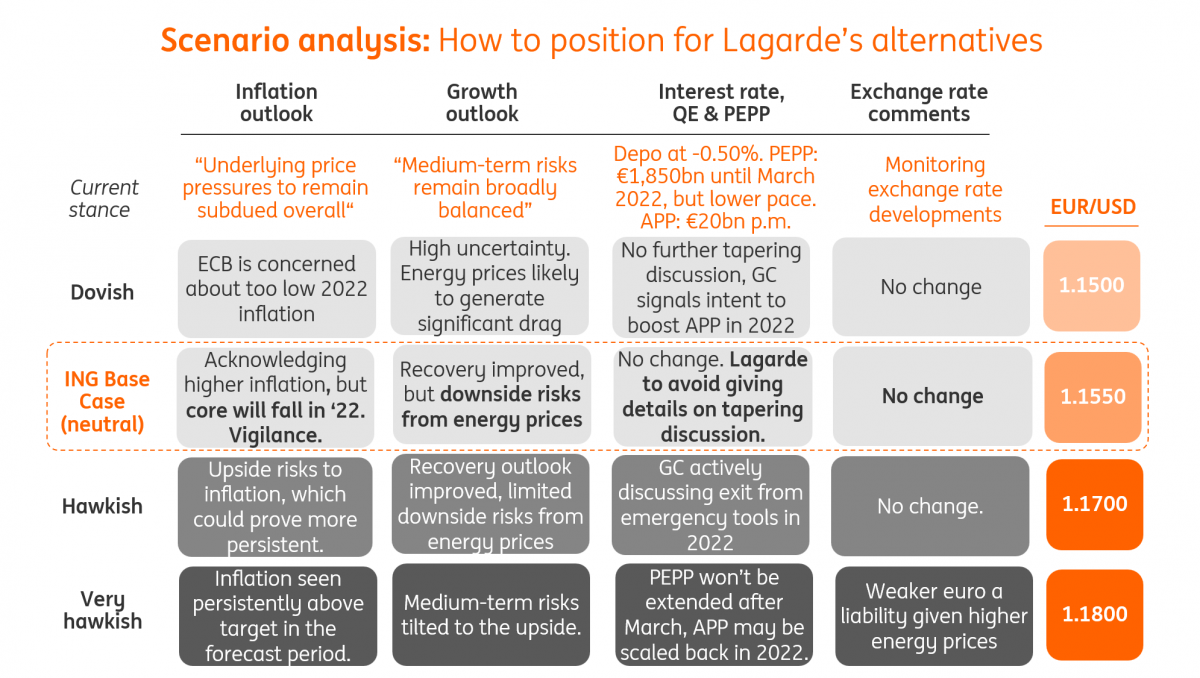

We think ECB President Lagarde will use all her diplomatic skills to moderate the diverging views of hawks and doves within the Governing Council on Thursday, and a neutral message may ultimately defy some of the market’s hawkish expectations. The balance of risks for EUR/USD (which is overvalued in the short term) appears slightly tilted to the downside.

Hawkish expectations rose significantly

The European Central Bank’s September meeting marked a small victory for the hawks, as the Governing Council decided to reduce the pace of asset purchases under the Pandemic Emergency Purchase Programme (PEPP), while keeping all other measures unchanged. Since then, a sharp rise in global energy prices has added upside risk to the inflation outlook, and a number of central banks, like the neighbouring Bank of England, have made quite a decisive hawkish shift in their language as a result.

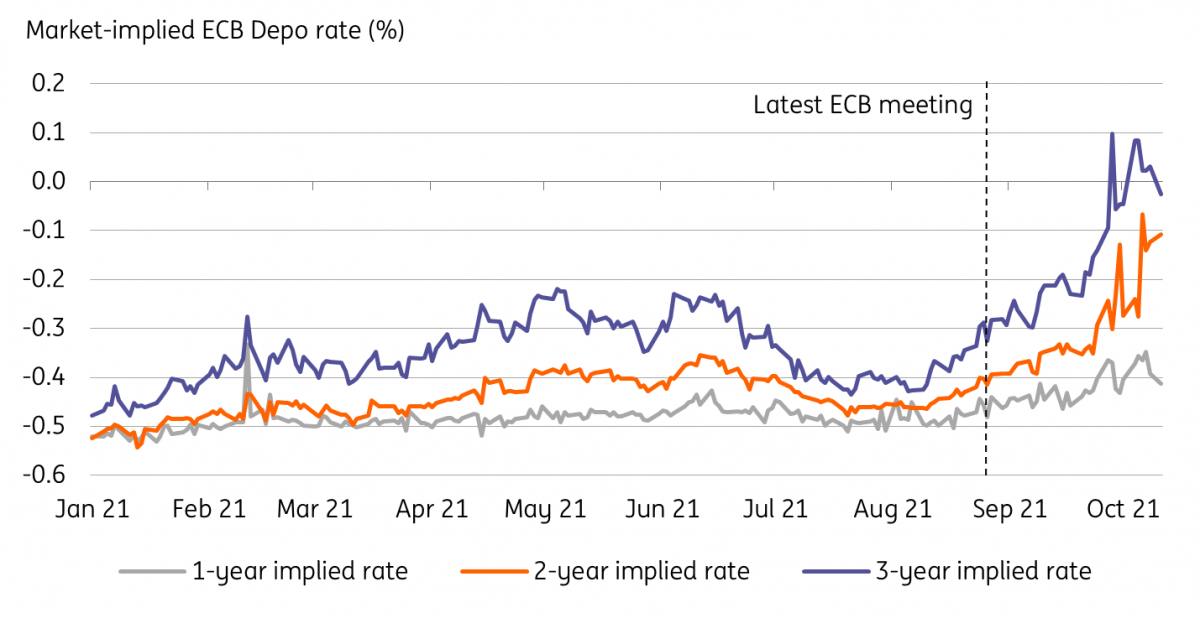

The market reaction to higher energy prices has been channelled through a widespread hawkish re-repricing in rate expectations, which has also involved the ECB, as shown in the chart below. Markets are now pricing in a 10bp hike in the deposit rate in late 2022.

A neutral tone may lead to a (contained) EUR/USD correction

These hawkish expectations may face a first reality check at the October ECB meeting on Thursday. As discussed in our ECB Preview note, this week’s discussion in Frankfurt will likely centre around whether the recent upside pressure to prices will still prove more, or less transitory and crucially whether it will soon be necessary to further scale back the bank’s emergency policy tools. At the same time, recent comments by ECB chief economist Philip Lane suggest that the ECB is not really satisfied with current market expectations about the first rate hike.

Our view is that the policy statement and the following press conference by President Christine Lagarde will be quite neutral, possibly with a further more explicit acknowledgement that higher inflation could be more persistent in 2022. We think Lagarde will carefully try to avoid giving any hint that the current debate between the hawks and doves in the Governing Council is leaning in any clear direction, ultimately leaving many options open when it comes to the timing and pace of the unwinding of monetary stimulus. What we could see is the ECB bringing back Jean-Claude Trichet’s preferred phrase of ‘vigilance’ against inflation.

The clear intent to avoid giving details on tapering may disappoint the hawkish expectations currently priced into the short end of the EUR curve. From an FX perspective, we could see some euro weakness on Thursday as some of those hawkish bets are partly scaled back. Our short-term fair value model shows (chart above) that EUR/USD is currently trading in expensive territory (around 2.5% overvalued), with the short-term rate differential showing the highest beta of all factors considered in the model.

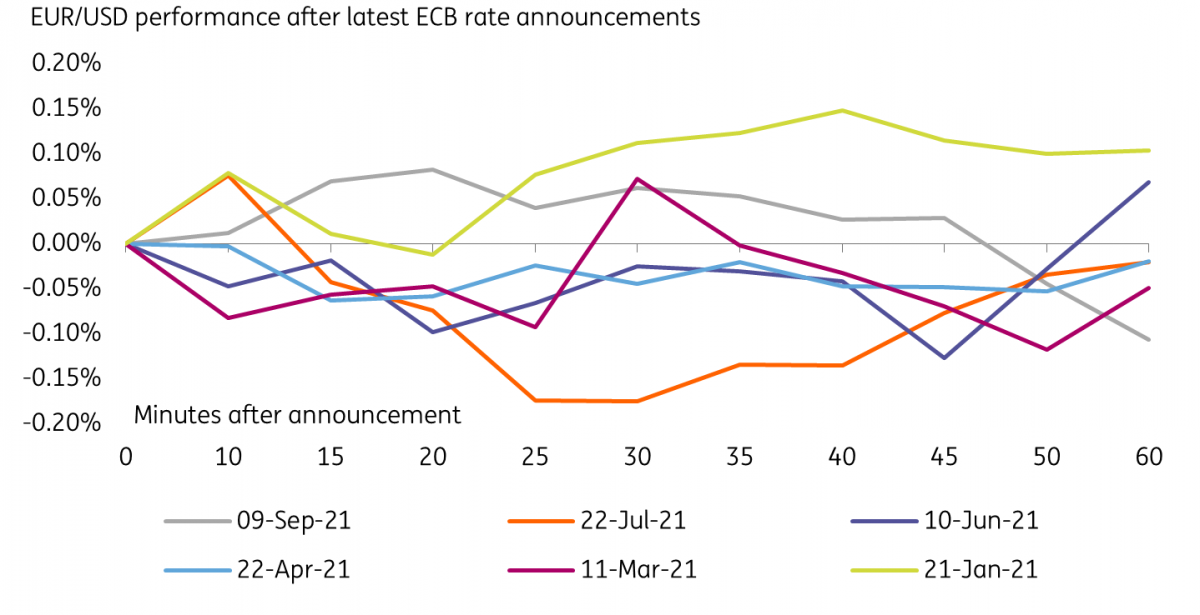

At the same time, a quick look at the recent EUR reaction to the latest ECB meetings suggests that the common currency has not been very reactive to rate announcements of late (chart below). Accordingly, we expect to see only a contained downward correction in EUR/USD on Thursday. The options market is currently pricing in around 35 pips of event-day volatility (measured as the break-even on a Thursday EUR/USD straddle).

We expect, instead, to see EUR/USD converge to its lower short-term fair value model more gradually in the coming weeks. We currently see room for the pair to test the sub-1.15 region in November, although seasonality trends in December may see it bounce back towards 1.1700 at the end of the year.