Vi står foran et paradigmeskifte med højere renter stort set over hele verden, vurderer ING. Selv det forsigtige Japan tager fat på rentestigninger. Det er især for obligationer i periferien, også i Europa, at der vil ske rentestigninger – med voksende rentespænd over for de tyske renter. Spændet er i dag på 2 pct. mellem italienske og tyske 10-årige renter. ECB bliver nødt til at fokusere netop på denne udvikling, mener ING, først og fremmest gennem afviklingen af PEPP-programmet.

Rates Spark: The paradigm shift of higher rates

Geopolitical tensions should not mask the fact that rates are in an uptrend. This is a global trend if there ever was one. Even the Bank of Japan’s (BoJ) apparent dovishness adds to upward pressure on foreign yields. Peripheral bonds are in the eye of the storm, and we think the ECB should look beyond PEPP reinvestments to contain spreads

Bonds remain caught in the ebb and flow of geopolitical tensions. Assuming the recent flare-up was the last such iteration, then yields will be free to resume their rise. If not, they are looking at a temporary retracement of their recent sell-off, but not a change of market dynamics. Our base case remains that inflation pressure and central banks’ urgency in tightening policy will continue to push rates higher.

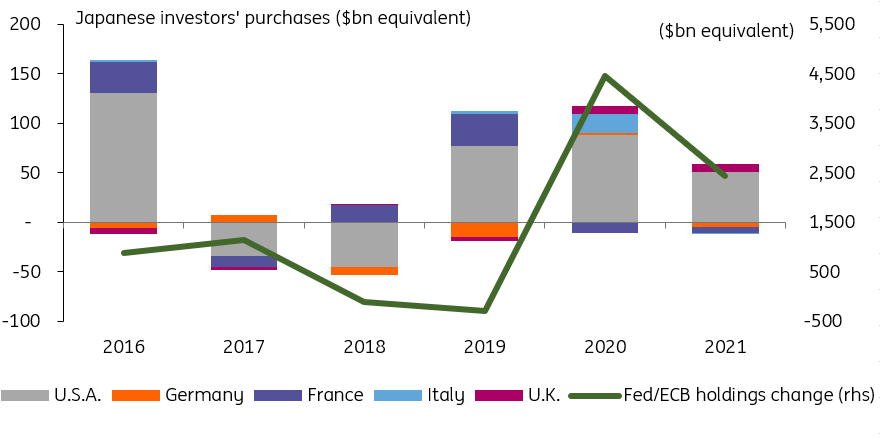

Keeping an eye on the BoJ and Japanese flow

This is a global dynamic if there ever was one, with DM bonds markets affected across the board. Even the staid Japanese Government Bond (JGB) market has shown signs of life lately with the 10Y point testing the upper limit of the BoJ’s tolerance band at 0.25%. Among the large developed market (DM) central banks, the BoJ will likely be the last one to tighten policy.

Tightening policy at the ECB and Fed tends to scare Japanese investors away

This shouldn’t prevent its policy from effecting rate markets abroad, however. The BoJ has long since stopped growing its bond portfolio, and we expect a rising degree of caution from Japanese investors when it comes to put their money to work abroad when foreign central banks are stepping back from easing. This is a tendency that we witnessed in the previous tightening cycle, and that we may be witnessing now. The difference of course is that the European Central Bank, and eventually the BoJ, will be following in the Fed’s footsteps this time around.

Peripheral debt in the eye of the storm

Ever since the beginning of this cycle, we’ve identified euro peripheral bond markets as a key vulnerability. Price action in recent weeks has shown that they were exposed not only to the ECB’s change of tone, but also to a repricing higher in US yields. This makes sense.

Large DM central banks have played an instrumental role in supressing rates volatility globally, and the compensation offered to investors for holding riskier debt. As they unwind these measures, it is rational for investors to reassess how much yield they require for holding debt in the face of higher future volatility.

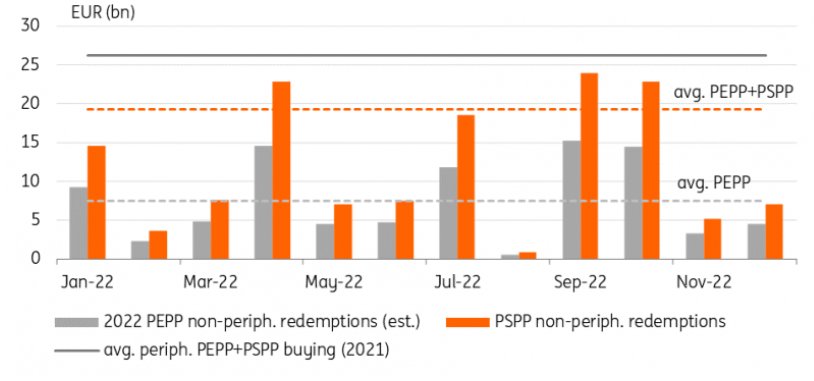

We doubt PEPP reinvestment flexibility will be enough to stop spread widening

The ECB acknowledged this risk but seems relaxed about the spread widening so far. Our best guess for a level that could raise their level of urgency is 200bp in the Italy-Germany 10Y spread. So far its strategy to contain spreads seem to be to rely on the flexibility of its PEPP reinvestments.

We argue that this will be insufficient to prevent further widening. Bringing public sector purchase programme (PSPP) reinvestments to bear would be a more credible strategy in our view, but the ECB has shown reluctance to diverge from the target country allocation key of this program.

Clarifications on that subject will be needed soon. Overnight, Banque de France governor Villeroy made a plea for ending net asset purchases in 3Q 2022 but said that an end to QE didn’t mean hiking rates immediately afterwards as the ECB remains data dependent. His fellow ECB governing council member Schnabel stressed the risks of waiting before normalising rates as “inflation will likely stabilise around our 2% target over the medium term”.