Resume af teksten:

Næste onsdag forventes det bredt, at Federal Reserve vil holde rentepolitikken uændret. Økonomien vokser stadig, men står over for stigende udfordringer, herunder højere omkostninger til transportbrændstof, der presser inflationen op. Jerome Powells periode som Fed Chair afsluttes den 15. maj. Markedet forventer generelt rentenedsættelser senere på året, med et mindre rentefald på 10 basispoint prissat inden årets udgang. FOMC’s seneste beslutningsreferater antyder begrænset sandsynlighed for politiske ændringer. Inflation forstærkes af højere brændstofpriser, men forventes ikke at være så bredt anlagt som forsyningskædeproblemer fra pandemien. Beskæftigelsesvæksten er næsten stagneret, og amerikansk økonomisk vækst trues af geopolitiske spændinger. Fx-markedet overvåger signaler fra FOMC, da udsagn om inflation kan påvirke dollaren.

Fra ING:

Next Wednesday, the Federal Reserve is widely expected to leave monetary policy unchanged in an environment where the economy continues to grow, albeit with intensifying headwinds, and transportation fuel costs are pushing inflation higher

Fed Chair Jerome Powell’s term is set to end on 15 May

Rate cuts remain more likely than hikes

Absolutely nothing is priced in terms of Fed funds futures contracts for the 29 April Federal Reserve policy decision, but the market still leans in the direction of eventual rate cuts with around 10bp of easing priced by the end of the year. The Fed itself continues to have one 25bp rate cut within its March economic projections for 2026, while the consensus amongst economists remains a little more aggressive, predicting two 25bp cuts in the latter part of the year. We also continue to forecast two rate cuts this year, one in September and one in December.

The main interest will be Jerome Powell’s press conference which, in theory, will be his last given his term as Chair ends on 15 May. As such, there will be questions over how he sees his legacy and his relationship with President Trump and whether he will choose to stay on at the Fed given his term as a Governor doesn’t end until January 2028. However, it may not actually be his last as Fed Chair. Until Republican Thom Tillis is satisfied that the Department of Justice’s “vindictive prosecution” of Jerome Powell, tied to the renovation of the Fed’s headquarters, has been brought to an end, the confirmation of Kevin Warsh as his successor will remain blocked at the Senate Banking Committee stage. Powell has already said he will stay on as chair “pro tempore”, which would only intensify tensions between the Fed and the President.

In terms of the outlook for monetary policy, we are unlikely to get anything particularly revelatory. The minutes from the last decision suggested that the “vast majority” of the FOMC membership saw employment risks as skewed to the downside, while progress on inflation was likely to be slower because of the economic headwinds being generated by developments in the Middle East. This is likely to remain the way the committee assesses the situation with little prospect of any immediate change in policy signalled.

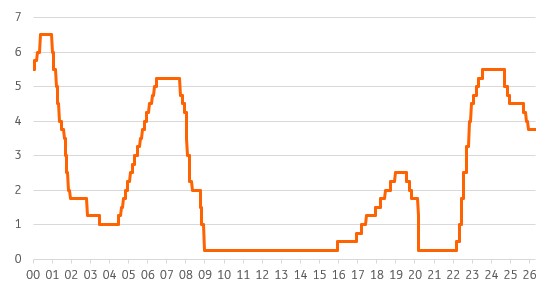

Fed funds ceiling (%)

Source: Macrobond

Inflation likely to be transitory with the jobs markets still stalled

In terms of inflation, it has been five years since either headline or core consumer price inflation were at or below the 2% target, and higher fuel and airline fares mean CPI looks set to break back above 4% imminently. The Federal Reserve can’t do anything to ease the current energy supply shock though. Instead, its focus is to ensure that inflation expectations remain contained and, for now, that seems to be the case. Hence the mildly hawkish rhetoric coming from officials.

Importantly, the current supply shock, focused on fuel prices, is not as broad as the pandemic-related supply chain stresses in 2020/21, and we don’t have the same sort of demand impetus that would risk a broader, more persistent inflation story.

Real household disposable incomes are already flatlining, so we see higher fuel prices as being demand destructive via reduced spending power. This is set to weigh on core inflation, and we also need to remember the importance of shelter costs within the US inflation basket (35.5% weighting for headline and 44% for core), which we expect to moderate further. Moreover, if Middle East tensions ease and oil prices drop back to below where they are today, there is a high probability of sub-2% year-on-year inflation being achieved in 2027.

In terms of jobs, there are only 260,000 more people in work today than 12 months ago, implying that the jobs market has effectively stalled during a period when the US growth story was robust. Our concern is that with the Middle East tensions showing little sign of coming to an imminent conclusion, an overlay of heightened geopolitical, economic and market angst is not going to incentivise business to suddenly start hiring now. In fact, with cost pressures rising and consumer spending power being squeezed, corporate profitability will face more challenges and runs the risk that employers will look to cost containment measures. This threatens weaker payrolls numbers in the coming months.

The Federal Reserve has to optimise monetary policy for two very different goals – inflation and jobs. It still views the current stance of monetary policy as being modestly restrictive. With a new, more dovish Fed Chair taking office and key elections this year, which will keep up the political pressure for action, we look for September and December Fed cuts.

The balance sheet and prognosis for Treasuries

Since the T-bills buying programme (re)commenced in mid-December, holdings of bills have risen to over USD$425bn (from USD$195bn). That has expanded the Fed’s overall “securities” holdings (including bills) by some USD$185bn. The Fed did this to help boost bank reserves, which had fallen to below USD$3tn, coinciding with repo tightness, and in consequence saw the effective funds rate rise right up to just 1bp short of the rate paid on reserves. Since then, repo pressure has eased, and this week, the New York Fed announced a reduction in monthly T-bills buying from USD$40bn to USD$25bn. This is a purely operational move, completely within its authority and as agreed at a prior FOMC meeting. Still, Chair Powell could get some questions on this, or indeed he could comment on it up front. It certainly suggests a degree of comfort on the part of the Fed over liquidity conditions.

There is also a link here with the incoming chair, Kevin Warsh. He has an ambition to reduce the Fed’s holdings of bonds, and in particular, Mortgage Backed Securities. Currently, the Fed holds just under USD$2tn of these, and continues to roll them off as they mature. It’s a slow process though, running at some USD$10-15bn per month. Chair Powell could get quizzed on this, too. Any acceleration in roll-off, e.g. outright selling, would place upward pressure on longer-term Treasury yields, as any selling would likely occur in longer tenors. There is no stated plan here. It’s all supposition at this stage. But it’s very market relevant. The odds are that Chair Powell swats away questions on this, as his FOMC has a steady-as-she goes policy, and he won’t comment on what Kevin Warsh might do. But still, worth asking the question(s). Beyond that, the bulk of the Treasury-relevant issues will centre on inflation expectations as seen through the Powell prism.

Potentially some upside risks for the dollar

Even though the Fed story is far less of a driver for the dollar than events in the Middle East, the FX market will still take note of the FOMC statement and Chair Powell’s press conference. Part of the market’s enduring demand for risk assets this year has rested on the expectation that the Fed will help out with rate cuts (and a weaker dollar).

Depending on how tough Chair Powell sounds on monitoring the inflation threat, and of course, depending on where energy prices are at the time, we see some potential upside risks to the dollar from this FOMC. Should Chair Powell echo any of the recent comments by Christopher Waller that the longer energy prices stay high, the greater chance of unchanged policy, then some bearish flattening of the yield curve could give the dollar a lift across the board.

If that is the case, EUR/USD could be heading down towards the 1.15 area consistent with the ‘Prolonged Disruption’ scenario presented in our recent update . Depending on how hawkish the Bank of Japan has been at its meeting the day before the FOMC, USD/JPY could be embarking on a sustained push above 160. One week realised USD/JPY volatility has recently dipped to 5%, which is exceptionally low for this pair. Given the unstable global backdrop, April’s two-yen range in USD/JPY looks too narrow and at this stage, the upside looks the path of least resistance.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.