ING analyserer den økonomikke genrejsning i Europa i forhold til, at der ikke sker en pind med renten. ING tror, at renten stort set vil være uændret hele året, omend 10-årige Bunds vil stige fra 0,1 pct. til 0,2 pct. ING vurderer, at ECB fortsat vil nægte at ændre sit opkøbsprogram. Derfor kan markedet glemme alt om stigende europæiske renter, og inflationen bliver ikke normaliseret.

Rates Spark: An unstoppable force meets an unmovable object

EUR rates, the unmovable object

The performance in EUR rates so far this week has been rock-solid, and this allows markets to look to the few days separating us from the 10 June ECB meeting with relative calm. Positioning is difficult to assess given the market volatility and drop in yields since their mid-May peak.

Our hunch is that longs/receivers have dominated price action in the past two weeks and are thus more liable to take risk off the table before the meeting.

We tend to still favour higher interest rates

Against this theory, one might disagree that interest rate and bond markets have largely shrugged off better economic data and heavy supply this week.

The logical conclusion would be that today’s duration-heavy French auction and PMI services, would fail to make a dent in the strength in EUR rates. This is entirely possible but since this short-term conclusion clashes with our higher-conviction medium-term view, we tend to still favour higher interest rates.

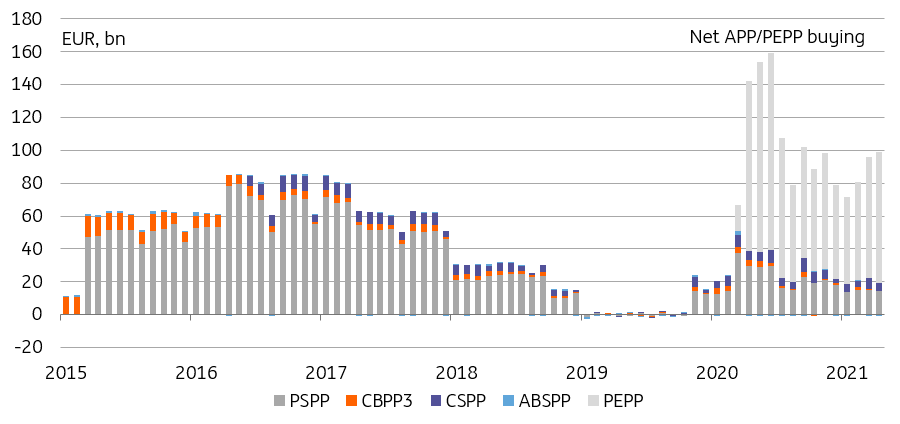

ECB bond purchases smother rate volatility, a boon for financial markets, and the economy

The European recovery, the unstoppable force

To be sure, the proximity of the ECB meeting, and an apparent refusal to contemplate tapering, has helped EUR rates regain their poise of late. We think this hides an unstable equilibrium: one where ECB purchases smother rates volatility but where end investors balk at buying bonds that clearly yield less than what the recovery warrants, see for example the decrease in demand at German auctions.

The way out of this conundrum is simple in our view: more and more bond demand will be diverted towards higher yielding alternatives as they offer at least a spread buffer against future rate rises.

ECB purchases smother rates volatility but end investors balk at buying bonds

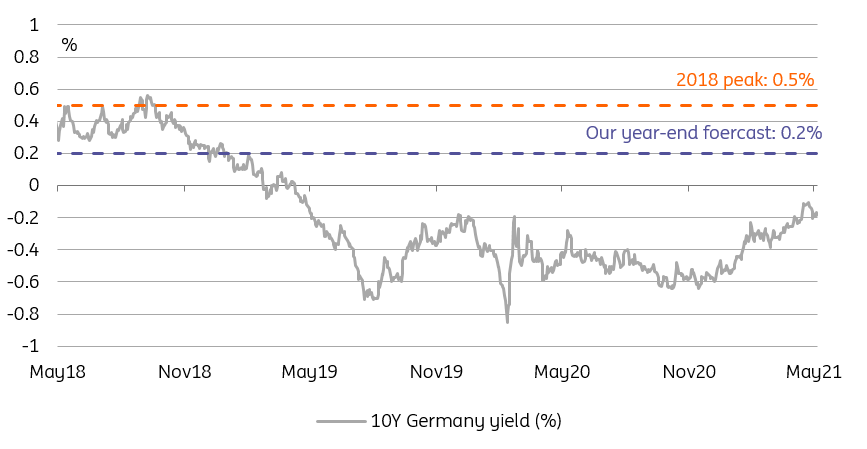

One should also note that, with a longer-term view in mind, the upcoming EUR rate rises will be fairly limited, and thus present no great threat to fixed income investors. Consider our year-end forecast for 10Y Bund yields at 0.2%. It implies that rates are about halfway through their adjustment this year.

This is quite a significant rise but would still take them well below their 2018 peak of 0.5% which they reached the last time spot inflation rose above 2%.

Core rates will continue to rise this year, but remain well below their 2018 peak

This is the kind of rise that the fixed income market, and the broader economy, should be able to live with if strong sentiment translates into equally strong growth. The more distant idea of a full normalisation of rates and of ECB policy is not something the market should spend a lot of time thinking about.

If our view pans out, inflation returning durably to target is a remote possibility, and so is the end of net QE purchases by virtue of the ECB’s forward guidance, let alone rate hikes.