Den amerikanske industri er i rigtig god form, skriver ING. Indekset for industriproduktionen, ISM, steg til 61,1 point i november. Både produktion og ordrer er over 60 point. Alt over 50 point er udtrykt for ekspansion. Beskæftigelsen steg til det højeste niveau siden april. Det betyder, at forbrugerne er parate til at betale konstant højere priser, og derfor er der udsigt til vedvarende høj inflation. ING forudser, at den økonomiske vækst i indeværende kvartal bliver på godt 6 pct. Alt går godt, og pengepolitikken vil blive strammet mere end hidtil forventet – hvis ellers Omicron tillader det…

US manufacturing and construction point to 6%+ GDP growth

Very healthy manufacturing ISM and construction data coming after last week’s robust consumer spending numbers suggests GDP will post a solid 6%+ increase in the current quarter. Inflation is likely to record a similar reading, meaning the case for swifter Fed policy tightening is strong. Omicron permitting…

Manufacturers have full order books and pricing power

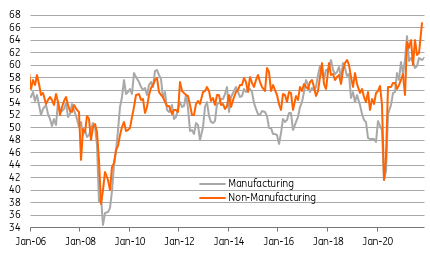

The November reading of the ISM manufacturing index increased to 61.1 from 60.8. A very healthy outcome, and with both production and new orders also above 60 – remember that anything above 50 is expansion – it reinforces the message that the sector is in great shape. Additionally, employment increased to the highest level since April, which bodes well for Friday’s employment report with a figure in excess of 500,000 jobs clearly on the cards.

ISM headline readings

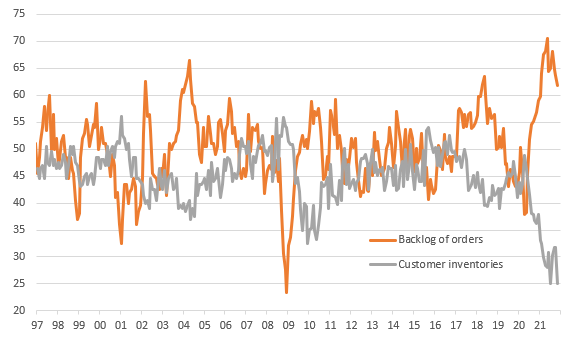

Meanwhile, the backlog of orders remains elevated at 61.9 and customer inventories are back at all time lows. This means that the narrative of full order books and desperate customers still holds, which in turn reinforces the message that companies have pricing power. Any cost increases they face can be passed on, which will help keep inflation higher for longer and fully justifies Fed Chair Jerome Powell’s decision to retire the “transitory” description of inflation.

Full order books and low inventory numbers show businesses can pass cost increases onto desperate customers

Construction looks set for a rebound

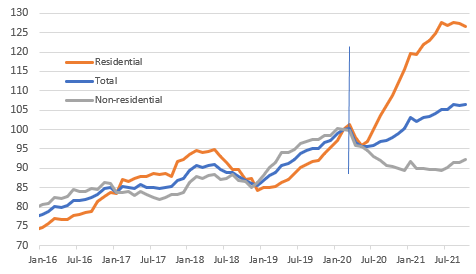

Separately, the October construction report didn’t post quite as strong an increase as hoped (0.2% versus the 0.4% consensus), but September was revised from a -0.5% reading to -0.1%. Residential spending fell 0.5% after a 0.3% drop in September while non-residential construction grew 0.9%.

Residential construction should soon return to positive growth given the recovery in home builder sentiment and builder permits. Non-residential construction should be under-pinned by the government’s infrastructure spending plans and the return of corporate capital expenditure.

Construction output levels (February 2020 = 100)

The case for Fed action continues to build

Today’s two reports suggest we should continue to expect GDP growth to come in around 6.5% for the current quarter. With inflation likely to average something similar, the case for an early QE taper conclusion and rate hikes coming from summer 2022 onwards looks strong. Omicron permitting…