Ruslands stop for gas til Polen og Bulgarien kan blive udvidet, og i så fald øges de økonomiske risici betragteligt, skriver ING. Så bliver aktiemarkederne mere risikofyldte, og renterne på statsobligationer vil stige. Inflationen vil få et pres opad, og det bliver ikke bare energipriserne, der stiger. Det vil samtidig øge risikoen for recession. De gyldne tider er definitivt slut, men analysen fra ING viser også, at det er ekstremt svært at komme med konkrete prognoser for konsekvenserne, fordi så mange forskellige faktorer er i spil på én gang.

Rates Spark: bye bye, goldilocks

The times of solid risk sentiment in the face of tightening central banks are over. The end of the goldilocks market makes sense and asset classes have to chose between the inflationary or recessionary scenarios. The curve can price both for a time, by flattening, but we think bonds will eventually benefit from safe-haven demand across the board

Inflation or recession, a familiar dilemma

What makes an energy crisis inflationary rather than deflationary? This is the question investors have to grapple with as the latest escalation of tensions between Russia and EU countries over payment and delivery of gas sent energy prices, gas in particular, on another spike. Back in late February/early March, the rate market’s knee-jerk reaction was to rally, to then quickly sell off as the inflationary implications dawned on investors. This was despite very real concerns about the accompanied hit to consumption and confidence, not to mention the risk of further escalation.

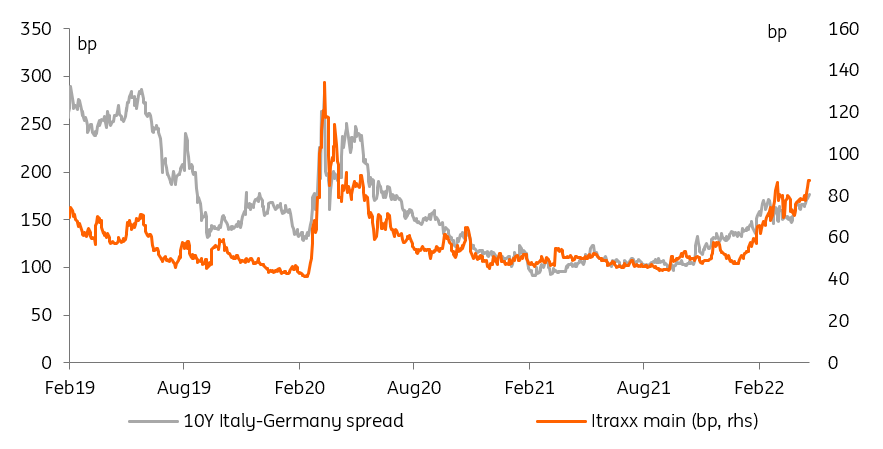

Stress is spreading to many corners of financial markets

The Fed (or ECB) put doesn’t apply when inflation is running at 7% or 8%

Fast forward to today, growth concerns have spread to China where the threat of more lockdowns is compounding already fragile economic sentiment elsewhere. The market’s blissful ignorance seems like a distant memory. Less than a week ago, it seemed nothing could stand on the market’s path towards higher rates – with obvious near-term targets at 3% and 1%, respectively, for 10Y Treasuries and Bunds. It is no coincidence that the penny dropped as central bank rhetoric goes into hawkish overdrive. Clearly, monetary policy cannot be blamed for the collapse in confidence but there is a distinct feeling that the Fed (or ECB) put doesn’t apply when inflation is running at 7% or 8%.

Bad news is bad news, even for inflation

For now, tightening expectations have held up at the front-end of yield curves. This tends to suggest that the inflationary impact, in the near term at least, of geopolitical tensions isn’t forgotten. Iron-clad hike expectations would mean that the long-end is more likely to reflect any growth concerns more freely, and so that the curve faces the risk of more bull-flattening. This makes sense in the near term but we doubt the market’s capacity to price both recession risk and aggressive rate hikes for long. Something has to give.

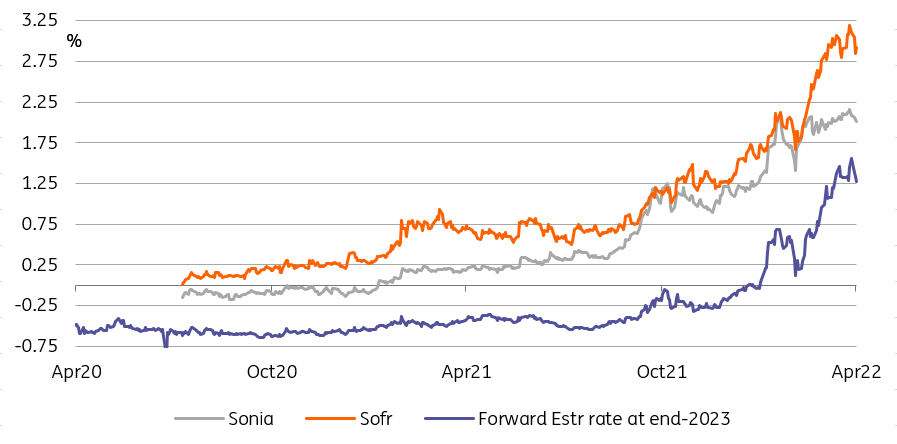

Rate hike expectations are holding up, for now

An even more hawkish ECB could prove unnerving for risk assets

Today’s German and Spanish CPIs are a good test of the market’s conviction. Renewed upward pressure on energy prices means that the relief of cooling CPI will prove short-lived. We’d also argue that the focus will increasingly be on core measures to assess the broadening of price pressures, something more likely to worry the ECB than a mere energy inflation spike. Counter-intuitively, a reading consistent with an even more hawkish ECB could prove unnerving for risk assets, and push more money into the safety of government bonds.