Resume af teksten:

Central bankers face a challenging task next week amid uncertainty in the Middle East and unclear data. Markets are anticipating rate hikes, but the case for such action is not clear. Central banks, including the Fed, ECB, and Bank of England, are expected to hold rates this month. Data such as inflation and GDP growth is not providing clear guidance, and inflation is mainly driven by motor fuel prices. Markets are pricing in potential rate hikes for the eurozone and UK by year-end, but immediate changes are unlikely. The situation requires central bankers to keep their options open, balancing the threat of hikes with market conditions.

Fra ING:

Central bankers face an unenviable task next week. Nobody knows where the crisis in the Middle East is going next. Nor is the data telling them how to act. Markets are bracing for rate hikes, yet the case for action is far from clear-cut. James Smith weighs up the dilemma as the team builds us up to next week’s Fed, ECB and Bank of England meetings

Trying to find the right balance is tough for central bankers such as Christine Lagarde

A day in the life of a central banker

Imagine for a moment you’re a central bank boss here in Europe. Not a great role play right now, if I’m honest, given, well… *gestures at everything going on in the world right now*

You have the unenviable task not only of setting policy next week, but also of coming up with a coherent message about what you might do in June.

Let’s start with the bad news: having kept all your options open in March and intimated you’d have a better grip of the situation by April, the truth is quite the opposite.

The better news is that nobody else has a clue where the crisis is headed, either. Another week of contradictory headlines and stalemate in the Strait of Hormuz has made the situation, if anything, harder to forecast. Polymarket, to the extent that it is a reliable gauge of anything, is pricing a 28% chance of a permanent peace deal by the end of May, down from 74% a week ago.

Better still, markets aren’t expecting a rate hike this month, anyway. Not from the Fed, ECB or Bank of England. An “on hold” decision looks like a no-brainer.

Time is on your side, but perhaps not for long. Markets are pricing upwards of two rate hikes for the eurozone and UK by year-end. A June rate rise is near-enough fully priced.

Your central challenge is that the data isn’t proving to be much of a guide right now. Inflation is up, but so far only because of motor fuel. We’ll get new numbers out of Europe over the coming days, but they’re unlikely to tell us much about the knock-on impact on core or food inflation. That’s going to take time; it’s not clear you’ll be much the wiser by June, even.

Surveys aren’t proving to be much more help either. Consumer inflation expectations are up (especially in the UK). But confidence is down. And while surveys of corporates – including this week’s purchasing manager’s indices – are unsurprisingly showing higher input costs, there’s only limited evidence that this is translating into a rise in output prices.

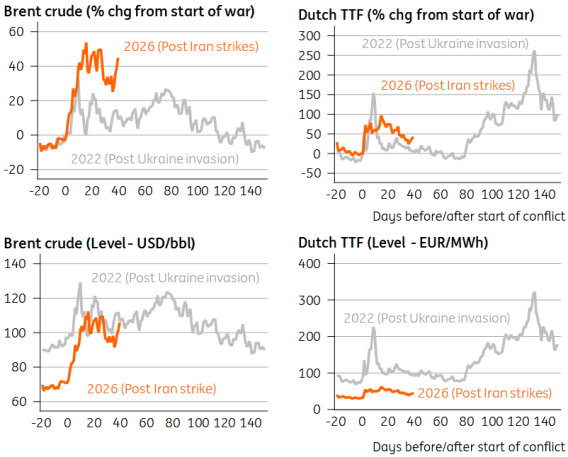

The one thing you can at least point to is natural gas prices. The problem in 2022 was that it became both an oil and an electricity crisis, the latter being a particular issue for core inflation. So far, this has proven to be only the former. Natural gas prices are much more contained than post the Ukraine invasion, in level terms if not in percentage changes. That’s a powerful argument in favour of keeping rates on hold for now.

How the energy crisis compares to 2022

Source: Macrobond, ING

So here’s your conundrum: Ideally you don’t want to hike interest rates at all. It’s fairly established wisdom now that the economic backdrop to this crisis is very different to the 2022 energy shock. And the more rate hikes markets price in, the tighter financial conditions become, and the more economic growth is going to take a hit.

Equally, having some limited tightening priced in is not entirely unhelpful, even if you can’t say that bit out loud. Rate hike expectations are keeping market measures of inflation expectations in check. The eurozone five-year inflation swap, priced five years forward – a gauge of longer-term inflation expectations – sits at 2.14%. That’s barely higher than it was before the war began.

The thing is, though, at some point, investors might start to think you’re all bark and no bite. The longer you don’t hike rates, the more likely it is that those inflation expectations start creeping up. Having been accused of being too slow to react four years ago, the last thing you want is to go down in the history books for making the same mistake twice. Fed Governor Christopher Waller’s speech last week entitled “one transitory shock after another” spoke to that anxiety.

And after all, what’s one or two rate hikes going to do, anyway? Then you remember that the ECB tried doing exactly this in both 2008 and 2011, only to be forced into awkward U-turns within months.

There are no good options right now – other than to keep everything on the table. The situation is delicate, one that requires you to keep the threat of hikes alive, without opening the floodgates for markets to price in yet more tightening. And if you’re lucky, you might not end up having to deliver much, if anything, at all.

Is anyone even listening right now, though? Just look at poor old Andrew Bailey at the Bank of England. He told investors in no uncertain terms at the start of the month that he didn’t think it needed to hike rates. And markets completely ignored him. Our Rates Strategy team have been arguing that interest rate expectations are being influenced by oil prices and not much else right now.

As my colleague Francesco put it in his scenarios for next week’s ECB meeting , you – the central bank – would have to come out with a real surprise to trigger an enduring market move. And that’s a brave call to make at a time of such extreme geopolitical uncertainty.

Alright, that’s quite enough time in a central banker costume for one day… Jump back into the real world and read on for exactly what our team are expecting from the major central banks next week.

James Smith

THINK Ahead in developed markets

United States (James Knightley)

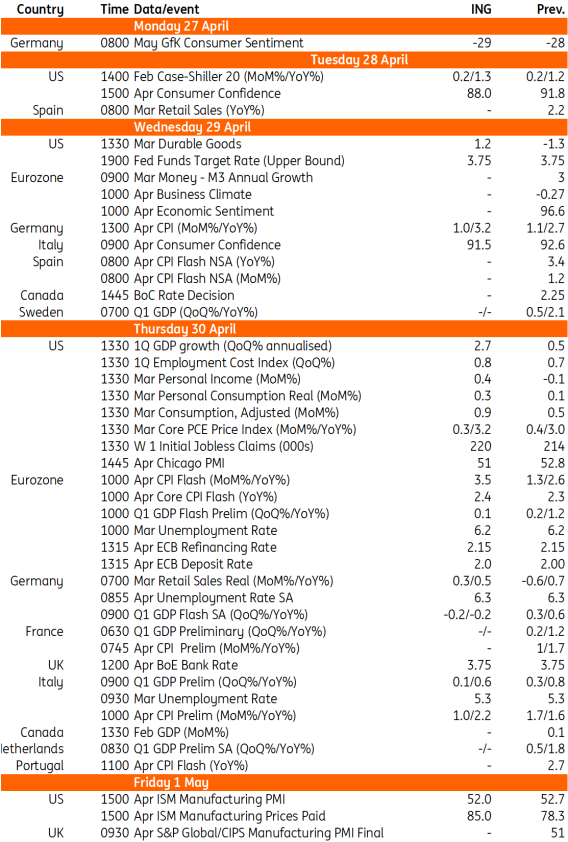

Rate Decision (Wed): The Federal Reserve will leave monetary policy unchanged next week in what is scheduled to be Jerome Powell’s last meeting as Fed Chair. The minutes to the last decision suggested that the “vast majority” of the FOMC membership saw employment risks as skewed to the downside, while progress on inflation was likely to be slower due to economic headwinds from developments in the Middle East. This is likely to remain the way the committee assesses the situation, with little prospect of any immediate change in policy signalled.

GDP (Wed): In terms of the data, 1Q GDP growth will be the highlight after the disappointing 0.5% annualised expansion in the fourth quarter of 2025. That was held back by the government shutdown that lasted throughout October, and we should see a corresponding rebound in government spending at the start of this year. Tech-related investment is expected to continue growing very strongly, net trade shouldn’t be too much of a headwind while residential investment will continue to be a drag. Unfortunately, the consumer spending story is likely to be more subdued with bad weather at the start of the year holding back activity. We expect GDP growth of 2.7% annualised.

Other numbers to watch include the 1Q employment cost index, which is the broadest measure of labour costs. Slowing wage growth is the main factor which should ease Federal Reserve concerns about second-round price effects due to higher motor fuel costs. Nonetheless, their favoured measure of inflation – the core PCE deflator is likely to temporarily pick up to 3.2% from 3%, confirming little prospect of any imminent Fed policy rate change.

Eurozone (Bert Colijn)

Rate decision (Thu): It is a big week ahead for the eurozone with the ECB rate decision and a lot of relevant data releases all packed into the Thursday. GDP for 1Q, inflation for April and unemployment for March will all come out just hours before the ECB announces its decision on rates. We expect them to remain on hold. That’s been hinted at by several Governing Council members lately, who have stressed the lack of new information and the absence of urgency to act. In that sense, April will mainly serve as a reality check for rate expectations, with markets currently pricing around 50bp of tightening by year end. Read our full preview

Inflation (Thu): The headline rate is set to increase further on the back of high energy prices, with eyes mainly on any preliminary impact on core inflation. We don’t expect much movement as of yet, but that doesn’t mean that the second round effect will not emerge, of course.

1Q GDP (Thu) : This will mainly show how the eurozone performed before the energy crisis, as only the month of March saw rising energy prices. Initial data have been sluggish, so after relatively strong GDP growth in 2025 despite all the uncertainty, 1Q could come in more modest.

United Kingdom (James Smith)

Rate decision (Thu): We expect an 8-1 decision from the Bank of England to keep rates on hold. Governor Bailey said at the start of April that markets were getting ahead of themselves on rate hikes. But with uncertainty still elevated and the committee likely to become more visibly divided once again, we doubt the Bank will want to double down on this push back against market pricing next week. Read our full preview

Canada (James Knightley)

Rate Decision (Wed): The Bank of Canada looks set to leave the policy rate unchanged at 2.25%. They have lowered it from 5% in 2024 and, with core inflation broadly in line with the target and the unemployment rate seemingly stabilised, another on-hold decision looks certain. Markets are pricing one 25bp rate hike by the end of the year, but we are in the camp that looks for the BoC to leave its monetary policy stance unchanged throughout 2026.

THINK Ahead in EMEA

Poland (Adam Antoniak)

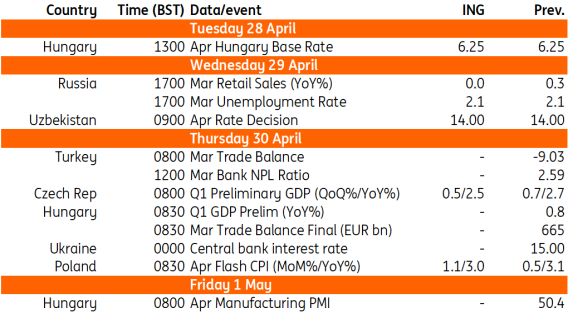

Flash CPI (Thu): The government’s fiscal package includes cuts in excise duty on petroleum and diesel, lower VAT (down to 8% from 23%), and a daily cap price set by the minister of energy, halting further increases in fuel prices vs March. Still, annual growth in fuel prices is projected to be higher than in the previous month due to a low reference base. Elsewhere, inflationary pressure is well contained. Hence, we expect only a small uptick in headline inflation to 3.1% YoY, if any, from 3.0% YoY in March. Core inflation excluding food and energy prices most likely remained at 2.7%YoY this month.

Czech Republic (David Havrlant)

GDP (Thu): The Czech economy likely entered the year in a mode of continued expansion in both annual and quarterly terms, yet at a somewhat slower pace than at the end of the previous year. The 1Q26 economic activity was affected by the onset of the turmoil in the Middle East, which sent energy prices on a steep upward path and propelled uncertainty. Still, the main negative impact will likely be tangible in the GDP readings that will follow.

Uzbekistan (Dmitry Dolgin)

Rate Decision (Wed): We expect the central bank (CBRU) to keep the policy rate unchanged at 14.00% at the upcoming meeting on 29 April, in line with the previous decision and guidance , as the domestic CPI and FX trends remained largely stable, the growth trend remained strong, while the external inflationary risks increased for the region. High real rate of c.7%, based on CPI over the past 12 months, remains one of the support factors for Uzbekistan’s competitiveness on the global capital markets.

Key events in developed markets next week

Source: Refinitiv, ING

Key events in EMEA next week

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.