Resume af teksten:

Taiwan oplevede en betydelig stigning i eksport og import i marts med henholdsvis 61,8% og 38,3% år-til-år. Eksportvæksten var drevet af maskiner og elektrisk udstyr, hvor især Information, Kommunikation og Audio-Video produkter steg med 134,5%. Taiwan’s handelsoverskud i første kvartal af 2026 steg med 124,2% år-til-år til 53 milliarder USD. Importpriserne steg også, men handelsbalancen blev forbedret på trods af stigende oliepriser. Taiwan’s økonomiske vækstprognose er opgraderet til 11,5% år-til-år for 1. kvartal og 8,2% for året, grundet stærke nettoeksportpræstationer. Der er dog bekymringer over energiforsyningssikkerheden på grund af regionale ustabiliteter.

Fra ING:

Exports surged 61.8% year-on-year in March, while imports surged 38.3%, both far eclipsing market expectations once again. Taiwan’s trade surplus has more than doubled in the first quarter of this year, suggesting another double-digit quarter of GDP growth. We are upgrading our growth forecasts as a result

People walk past shipping containers at the port of Kaohsiung City, Taiwan

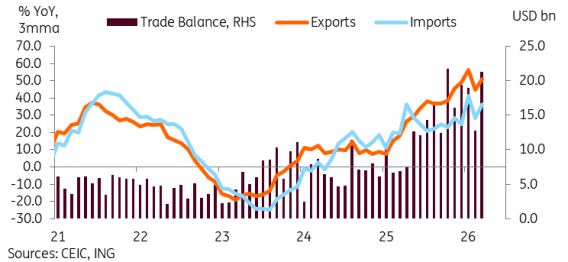

Taiwan’s trade surplus

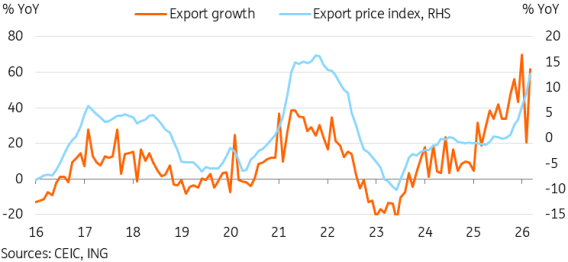

Taiwan’s tech exports continue to defy expectations

Taiwan’s March export growth surged to 61.8% YoY, tripling the growth rate from the Lunar New Year-impacted February growth of “just” 20.6% YoY. Once again, exports have significantly surpassed market forecasts.

Unsurprisingly, most of the strength remains tied to Taiwan’s primary export engine, the broader Machinery and Electrical Equipment category, which grew by 81.9% YoY and accounted for 85.8% of total exports in March. Within this category, Information, Communication and Audio-Video Products exports surged 134.5% YoY, electronic parts rose 44.0%, and semiconductor exports rose 45.7% in March from a year ago.

The continued outperformance has led to Taiwan’s trade and economy becoming increasingly concentrated and dependent on this segment; the subcategory represented 84.0% of total exports in 1Q26, up from 80.4% in 2025 and 73.2% in 2024.

A major reason for the outperformance is tied to a notable pickup in export prices. Taiwan’s USD-adjusted export price index surged 12.7% YoY in March, the highest level since 2022. Combined with strong demand on a volume level, this is a major factor causing outperformance, as we’ve also observed across other economies in the region.

Outside of this category, export growth generally looked pretty soft, with most other subcategories showing either single-digit or negative YoY growth.

Export price surge has contributed to headline export growth outperforming

Imports also surge but trade balance continues to beat

Imports also well eclipsed forecasts, surging to 38.3% YoY, up from 6.8% YoY in February. We also saw some of the same price factors play out on the import side, as import prices rose 8.5% YoY in March.

Interestingly, the data suggests that this wasn’t attributed to energy prices quite yet, with the price of oil imports rising to 72.2 USD per barrel, which rose to -8.5% YoY from -19.1% YoY but still remained negative. More pain is likely ahead on this front once import prices catch up with oil spot prices. Taiwan imported USD 21.6bn of petroleum products in 2025, where a price surge will likely cut into Taiwan’s trade surplus somewhat in the coming months.

Despite the upside surprise in import growth, the boom in exports far outweighed the faster imports when we look at the trade balance. Taiwan’s trade balance rose to a five-month high of USD 21.3bn, while its 1Q26 trade surplus rose to USD 53.0bn, which was up 124.2% YoY. This outperformance will likely translate to another quarter of double-digit GDP growth when Taiwan reports its 1Q26 GDP growth at the end of April.

Taiwan’s 1Q26 trade surplus has more than doubled year-on-year

Continued trade outperformance prompts a risky growth upgrade

We’ve written in previous reports that as the tech boom goes, so goes Taiwan’s economy. This logic still looks solid, even as the world faces greater uncertainties from higher energy prices.

It’s certainly a risky time to consider a forecast upgrade, given Taiwan’s over 95% energy import dependence and volatile headlines out of the Middle East that can change things at a moment’s notice. While we think that Taiwan’s economic growth will be able to absorb higher energy prices as long as the global tech boom and AI-related investments continue, energy shortages potentially impacting production would be a whole different story. As such, our outlook is contingent on some sort of resolution being reached in Iran in the coming weeks or months, or at least limited supply disruption leading to higher prices but not actual shortages.

However, it’s impossible to ignore the trade surplus once again, more than doubling in the first quarter of 2026, especially when considering the last time this happened in 4Q25, net exports added a whopping 11.9ppt to GDP growth. Market forecasts continue to undershoot actual growth even after waves of upgrades. We’re taking another shot here, upgrading our 1Q26 GDP forecast to 11.5% YoY from 10.2%, and our full-year GDP forecast to 8.2% YoY from 6.7%.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.