Resume af teksten:

Bank of Japan’s upcoming interest rate decision is under scrutiny amid complex economic conditions. Japanese inflation rose in March, further complicating the outlook for the central bank. South Korea’s GDP shows strong growth driven by chip exports. China’s upcoming PMI data may indicate a contraction, with the manufacturing and non-manufacturing indices expected to dip just below 50. Taiwan is set to release its first-quarter GDP data, with expectations of continued robust growth fuelled by external demand. Australia’s inflation is projected to rise significantly due to increasing oil prices, potentially prompting early action from the Reserve Bank of Australia.

Fra ING:

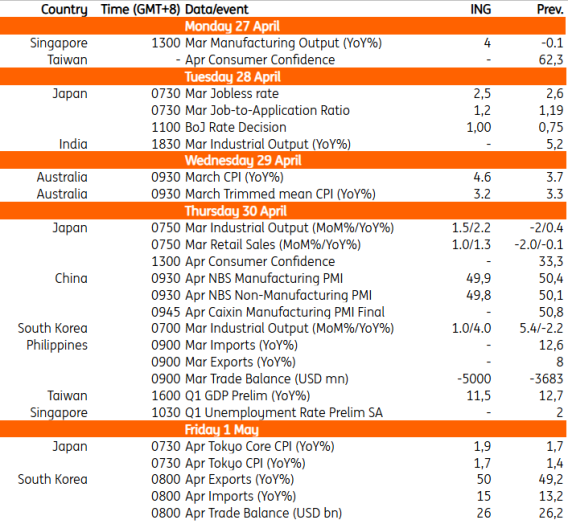

The Bank of Japan will announce a hotly-debated interest rate decision. Key data releases include China’s purchasing managers’ index, Australia’s inflation and Taiwan’s GDP

Asia Research highlights of the week

South Korean GDP surges, but K-shaped growth is challenge for central bank Japanese inflation quickened in March, complicating Bank of Japan outlook The Philippines kicks off hiking cycle, reasserting inflation control amid rising oil prices Bank Indonesia holds rates, prioritises rupiah stability Asia FX Talking: North-south divide

Japan: Inflation and labour market data complicate rate decision

Japanese data should indicate that inflationary pressures are intensifying, while the economy remains resilient. We expect labour market conditions to remain tight with the jobless rate edging down to 2.5%. Monthly activity data should rebound quite firmly, partially offsetting the previous month’s declines. We don’t think the energy shock has had a significant negative impact on production so far. Meanwhile, the Tokyo CPI is expected to rise faster in April, reflecting recent energy price hikes, a weak JPY, solid wage growth, and bi-annual price adjustments.

These developments complicate the Bank of Japan’s rate decision on Tuesday. Markets widely expect the BoJ to stay on hold amid uncertainty surrounding the Middle East situation. We continue to believe there’s a chance that the BoJ may hike on 28 April. Board members’ concerns about higher inflation expectations are likely to increase as real interest rates remain deeply negative. CPI inflation accelerated more than expected in March. It’s set to accelerate further in the coming months. The BoJ will release its quarterly outlook report on rate-decision day. The inflation outlook is likely to be revised upward from the current 1.9% to 2.4% for fiscal year 2026 and 2.0% to 2.2% for FY2027. Meanwhile, the GDP outlook is expected to be revised down modestly from the current 1.0% to 0.7% for FY2026. Even with the downward revision, GDP is expected to remain above potential, which should support BoJ rate hikes.

South Korea: Exports to show strength

Early April trade data shows robust chip exports are driving Korean export growth. With memory chip prices climbing and refineries passing higher input costs through to output, we expect April exports to increase 50% year over year.

China: PMI data could see a contraction

China releases its April PMI data. The official PMI rebounded to expansionary territory in March. In April, we could see the index dip back into contractionary territory, with the manufacturing PMI falling to 49.9 and the non-manufacturing PMI dipping to 49.8. We’re likely to see evidence of price pressures continuing to build in the PMI sub-indices.

Taiwan: We expect continued growth in Q1

Taiwan releases its first-quarter GDP data on Thursday. We expect Taiwan’s stellar growth to continue, with 11.5% YoY in the January-March period amid consistently outperforming data so far this year. Growth will be primarily driven by external demand again. There’s been a flurry of upward revisions over the last two years, as the economy continues to exceed expectations at nearly every turn. We revised our full-year GDP forecast up to 8.2% YoY from 6.7% YoY earlier this month. The first quarter release will go a long way to showing if this is an overshoot or still too conservative.

Australia: Inflation to reflect oil price surge

Australia’s CPI is expected to accelerate to 4.6% YoY, largely driven by the surge in oil prices. Inflation dynamics are likely to deteriorate further in the second quarter amid ongoing geopolitical tensions and no meaningful de‑escalation in the war. If the Reserve Bank of Australia intends to stay ahead of the curve, it’s likely to move in May rather than waiting until August.

Key events in Asia next week

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.