ING tror ikke, at der vil komme en rentestigning på den amerikanske centralbanks møde i denne uge, men derimod mener ING, at centralbanken omgående bør reducere sine obligationsopkøb, QE, for derved at få et snarligt fald i inflationen, der har forværret omkostningerne for erhvervslivet og forbrugerne. Opkøbene har ført til en ekstrem høj obligationsbeholdning på 9 trillioner dollar, og ING venter, at den bliver reduceret med omkring en tredjedel.

What to expect at the January Fed meeting

Building to a March hike

On the face of it, the 26 January 2022 Federal Open Market Committee (FOMC) meeting should be a non-event.

Speaking at his Senate confirmation hearing on 11 January, Federal Reserve Chairman Jerome Powell set out a clear timetable for events: “As we move through this year … if things develop as expected, we’ll be normalising policy, meaning we’re going to end our asset purchases in March, meaning we’ll be raising rates over the course of the year… At some point perhaps later this year we will start to allow the balance sheet to run off, and that’s just the road to normalising policy.”

With the economy regaining all of its lost output, inflation running at its highest rate since 1982 and the unemployment rate dropping below 4%, there is plenty to justify “policy normalisation”. Financial markets are now fully pricing a March rate hike with a further three moves expected during the course of 2022.

An even earlier end to QE?

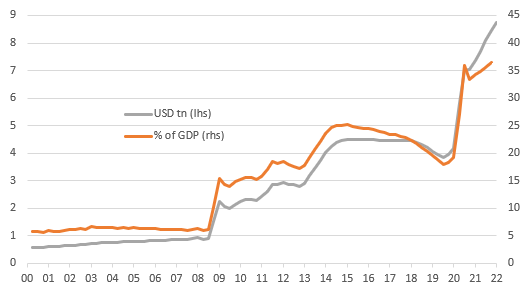

Given this backdrop there is the obvious question, why is the Fed saying it will keep buying Treasuries and agency mortgage-backed securities (MBS) through to mid-March? After all, Powell acknowledged at the same hearing that “we’re mindful the balance sheet is $9tr. It’s far above where it needs to be”.

Price pressures continue to broaden and deepen with the latest increase in energy prices heightening the prospect of an extended run of above-target inflation. At the same time, the competition for labour is resulting in record job quits and it means that companies are not only having to pay more to recruit new workers, but also pay more to retain the ones they currently have.

Consequently, employment costs rose sharply in the third quarter of 2021 and next Friday’s (28 January) 4Q Employment Cost Index could show a similarly steep rise, increasing the prospect that inflation pressures remain elevated for longer than the Fed had envisaged.

We therefore see no reason for the Fed to continue purchasing assets and expect them to announce an immediate conclusion to their QE asset purchase program. This earlier corrective action on the balance sheet would also help reduce talk of a potential 50bp March rate hike, while opening up the possibility of an earlier start to a shrinking of the balance sheet.

The Federal Reserve’s balance sheet in US dollars and measured as a proportion of US GDP

50bp calls look implausible

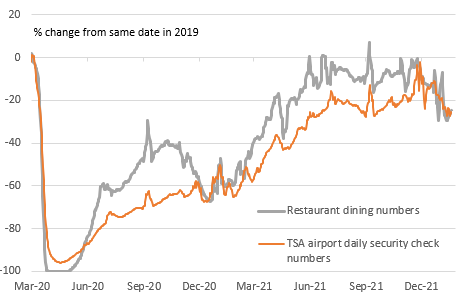

Talk of a possible 50bp move seems far-fetched to us. High-frequency data suggests the break-through of the Omicron variant has heightened Covid wariness and people movement is significantly down on early December levels. Restaurant dining and air passenger figures are 30% lower than what would ordinarily be expected at this time of year. Worker absences due to Covid quarantining also appear to be impacting economic activity with the potential for a decline in January non-farm payrolls signalled by some surveys, while we expect 1Q GDP to come in close to just 1% annualised.

The Fed would be highly unlikely to move by 50bp in this situation, but a 25bp could be justified on the basis that Omicron intensifies production bottlenecks and inflation pressures. With Covid case numbers also now falling in the US we are hopeful that we will see a rebound in consumer and business activity in February and March, particularly the rising wage narrative and the strong platform that a $30tr increase in household wealth through the pandemic provides.

Covid caution is hurting consumer demand for services

Balance sheet to do the heavy lifting

As we recently wrote in our outlook for the Fed’s balance sheet, further interest rate increases are coming – most likely at a pace of one per quarter. Some analysts are more forceful, proposing five or maybe even six, but we think earlier, more aggressive action on balance sheet reduction can do a lot of the heavy lifting in terms of “normalising” policy.

Given the balance sheet has more than doubled in size during the pandemic, there is a strong case for the Fed shrinking the balance sheet by at least double the initial rate seen in 2015-17 of $6bn Treasuries and $4bn agency MBS per month.

We would suggest that within six months of the March rate hike we would see the Fed allowing $10bn and $6bn per month initially being allowed to roll off before swiftly going up to $50bn and $40bn per month. Officials note that the current weighted average maturity of the Fed’s holdings are shorter than five years ago, so this structural change means the balance sheet can certainly shrink more quickly than it did last time.

In terms of how far they could go, Christopher Waller, member of the Federal Reserve Board of Governors, suggested in December that he would like to see the balance sheet brought down to around 20% of GDP from the current 36%. Assuming average nominal GDP growth of 5% over the next three years, this would imply a balance sheet of roughly $5.4tr, which would mean the Fed offloading $3.4tr of assets.

This can certainly contribute to the yield curve remaining steeper with the long end moving higher relative to if the Fed focused on raising the Fed funds target rate. It would also mean that the terminal rate for Fed funds may be closer to 2% rather than the 2.5% the Fed is currently projecting.