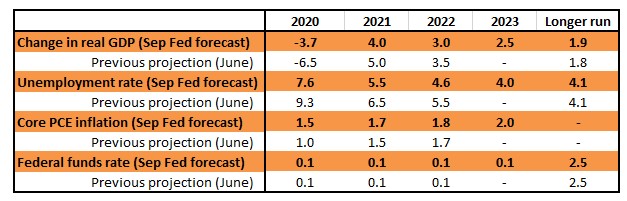

Den amerikanske centralbank, Fed, har i sin seneste rapport gjort det rimelig klart, at der ikke kommer nogen rentestigning før i 2024. Der er endda et par medlemmer af centralbanken som mener, at Fed bør udtrykke en større fleksibilitet, dvs. at være parat til en lav rente i endnu længere tid. Centralbanken vurderer, at der bliver en minusvækst på 3,7 pct. i fjerde kvartal – knap så dårligt som tidligere antaget, men samtidig har centralbanken nedjusteret sine prognoser en smule for 2021 og 2022 til henholdsvis 4 og 3 pct. I rapporten hedder det, at der er “betydelige risici på mellemlangt sigt.”

Uddrag fra ING:

US: Fed says wait until 2024

Cautious Fed still has dissent

The Federal reserve has left monetary policy unchanged today, which is unsurprising given the decent activity and employment backdrop and the recent rise in inflation. Nonetheless, the Fed remains wary, suggesting that the pandemic will “continue to weigh on economic activity, employment and inflation in the near-term, and pose considerable risks to the economic outlook over the medium term”.

The key part of the statement surrounds the updated guidance on policy in light of the publication of the Fed’s monetary policy strategy review which heralded “average” inflation targeting.

They have opted for “the Committee will aim to achieve inflation moderately above 2 percent for some time so that inflation averages 2 percent over time and longer-term inflation expectations remain well anchored at 2 percent.”

There wasn’t universal agreement on this though. Robert Kaplan wanted the statement to emphasise “greater policy rate flexibility beyond that point” – i.e. suggesting rates could stay low for even longer.

Neel Kashkari wanted to specify they wouldn’t change rates until “core inflation has reached 2% on a sustained basis” – again, slightly more dovish than what was agreed (“sustained” versus “some time”). Neither of these are hugely significant deviations from what was agreed and in any case the dot diagram of individual forecasts give us more specific views.

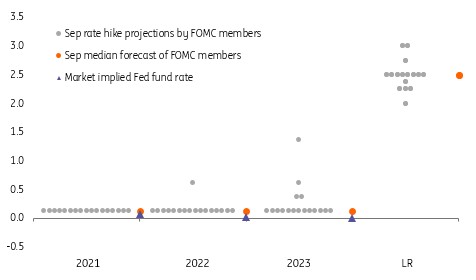

The Fed’s new “dot plot”

Fed consensus suggests nothing before 2024

They have the median Fed funds rate projected to remain in the current 0-0.25% range through the whole of 2023 with just one out of 17 members looking for a hike before the end of 2022 and just four expecting a move at some point in 2023. Interestingly, they kept their long-term projection unchanged at 2.5% with all member clustering between 2% and 3%.

As such the Fed is telling us they don’t think that rates will need to rise until 2024, which is understandable given the new policy strategy from the Fed – acknowledging inflation shortfalls can be just as bad as inflation overshoots – and their past track record on hitting the 2% target. This is an implicit acknowledgement that they ran policy too tight in recent years.

Since the beginning of 2010 the Fed’s favoured measure on inflation, the core personal consumer expenditure deflator, has been at or above 2% in just 13 months – so a hit rate of one in 10 – posting an average of 1.6% year on year over the past decade.

In terms of their broader forecasts they have revised up 4Q GDP YoY growth for 2020 to -3.7% from -6.5%, but because of the earlier and more vigorous rebound have cut 2021 to 4% from 5% and 2022 from 3.5% to 3%. The core inflation numbers have also been revised a little higher with the core PCE deflator expected to end 2023 at 2%.

New economic forecasts from the Fed